Commercial Truck Liability: Navigating Risk on the Road

One accident involving your commercial truck can expose your business to significant financial and legal liability. At Briggs Agency, Inc., we’ve seen how quickly a single incident can threaten a trucking operation’s future.

Commercial truck liability coverage protects you when your vehicles cause injury or damage to others on the road. This guide walks you through what your policy actually covers, the risks you face, and concrete steps to reduce your premiums.

What Commercial Truck Liability Coverage Actually Covers

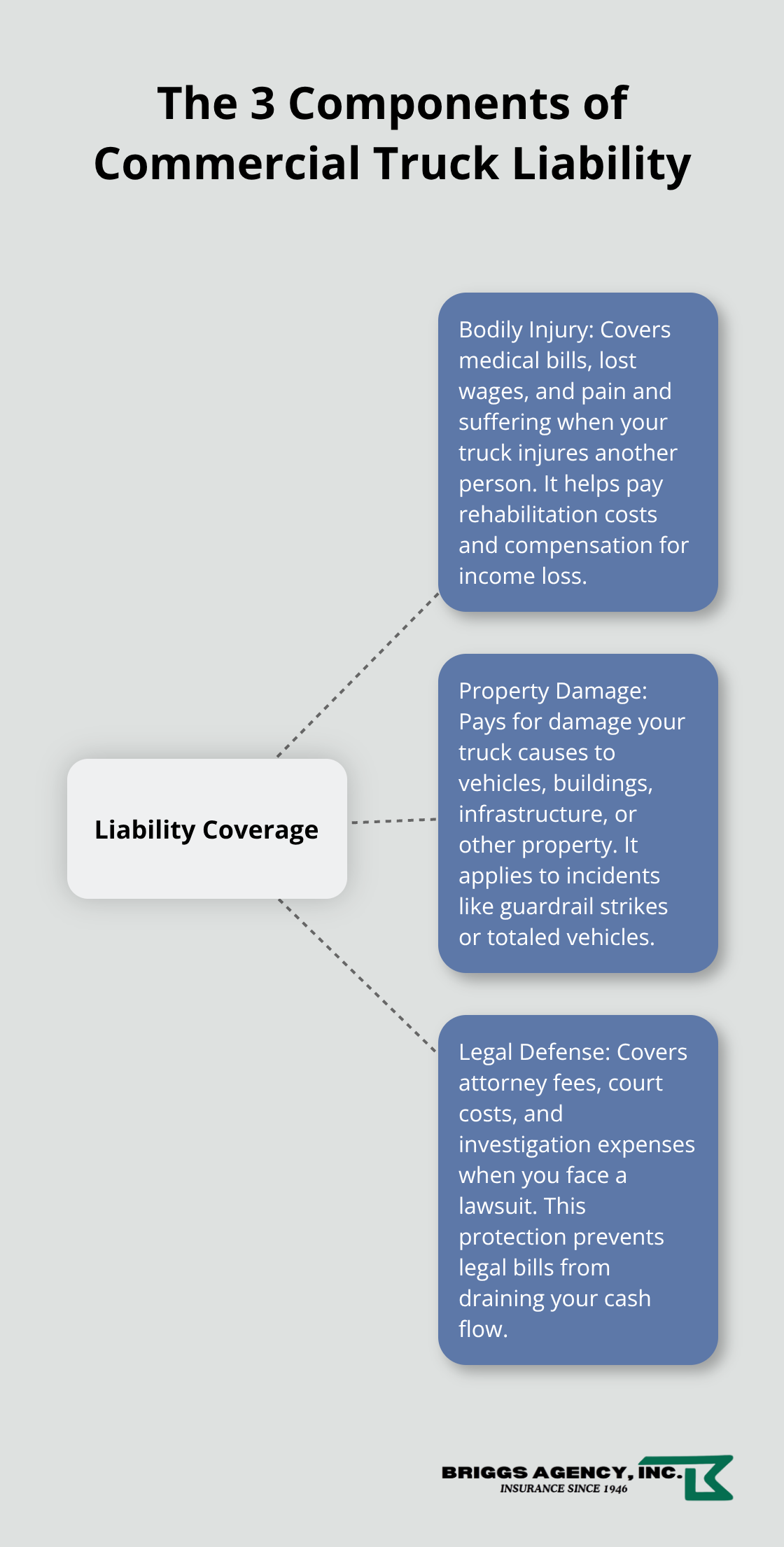

The Three Core Components of Your Policy

Commercial truck liability coverage protects your business through three distinct components when your truck causes harm to someone else on the road. Bodily injury liability covers medical expenses, lost wages, and pain and suffering when your truck injures another person. If your driver causes a collision that puts another driver in the hospital, their medical bills, rehabilitation costs, and compensation for lost income all fall under this coverage. Property damage liability pays for damage to vehicles, buildings, infrastructure, or other property your truck causes. A side-swipe collision that damages a guardrail, a rear-end crash that totals another vehicle, or cargo that falls and damages someone’s storefront all qualify for this protection.

Legal Defense: A Hidden but Essential Layer

Legal defense costs represent the third critical component-your insurer covers attorney fees, court expenses, and investigation costs when you face a lawsuit. This matters because legal defense costs in truck accident cases can quickly add up. Without this coverage, you would shoulder these costs out of pocket while your case proceeds, straining your cash flow and operations.

Federal Minimums vs. Real-World Requirements

Federal regulations require a minimum of $750,000 in liability coverage for most interstate trucking operations, according to the FMCSA. However, that minimum serves only as a baseline. Many shippers and brokers demand higher limits before they’ll contract with you, and your actual liability exposure depends on the cargo value you haul, the routes you operate, your driver’s experience, and your vehicle condition. If your coverage falls short and you’re found liable for damages exceeding your policy limits, your personal assets and business face direct risk.

Why Annual Reviews Matter

Your liability needs shift as your operation grows or changes. An experienced agent who understands trucking operations-not just general commercial insurance-can identify gaps in your coverage and recommend adjustments that align with your actual exposure. The difference between adequate protection and underinsurance often comes down to a conversation with someone who knows your business inside and out.

Understanding what your policy covers is only half the battle. The risks you actually face on the road determine whether your coverage is sufficient.

Common Risks Trucking Companies Face on the Road

Multi-Vehicle Collisions and Chain-Reaction Liability

Multi-vehicle collisions represent one of the most expensive liability exposures you face, and they happen more often than most trucking companies anticipate. When your truck triggers a chain-reaction crash on a highway, you become potentially liable for injuries and damages across multiple vehicles-medical bills for several drivers and passengers, vehicle repairs or total losses, and lost income for everyone affected. A single rear-end collision involving your truck and three other vehicles can easily generate $500,000 to $2 million in liability claims depending on injury severity and vehicle damage.

The FMCSA data shows that most truck crashes result from human error, but investigations frequently reveal that regulatory violations like hours-of-service fatigue contributed to the incident. These violations strengthen claims against your company and expose deeper liability. Driver negligence citations compound your exposure because they create a documented pattern that plaintiffs use to argue your company failed in hiring, training, or supervision. If your driver receives multiple speeding tickets or violations within a short period, insurance companies view your operation as higher risk, and that directly impacts your premiums at renewal.

Cargo Liability: A Threat Many Operators Underestimate

Cargo liability presents a different but equally serious threat that many trucking operators underestimate. When cargo shifts during transit, falls from your truck, or damages a shipper’s facility during loading or unloading, you face liability for those losses even if your driver followed standard procedures. Overweight loads and improperly secured cargo increase both your crash risk and your liability exposure-a load that falls onto another vehicle or pedestrian creates catastrophic injury claims that far exceed the cargo’s actual value.

Shippers and brokers now commonly demand that you carry cargo coverage as a contract requirement, and without it, you lose business opportunities. The value of loads you haul likely changes as your customer base evolves, which means your cargo coverage limits need regular attention. If you haul high-value goods like electronics or pharmaceuticals, your standard cargo coverage may be insufficient, and specialized endorsements become necessary to protect your business from underinsurance.

How Driver Violations Escalate Your Risk Profile

Your driver’s record directly shapes how insurers assess your operation’s risk level. Citations for speeding, hours-of-service violations, or unsafe lane changes signal to underwriters that your company may lack adequate supervision or training protocols. Each violation adds weight to your risk profile and can trigger premium increases at renewal, even if no accident occurred. Insurance companies track these patterns because they predict future claims-a driver with multiple violations statistically poses higher risk than one with a clean record.

Understanding these specific risks helps you identify where your coverage gaps exist and what steps reduce your exposure most effectively.

How to Lower Your Commercial Truck Liability Costs

Driver Training and Safety Programs Reduce Your Premiums

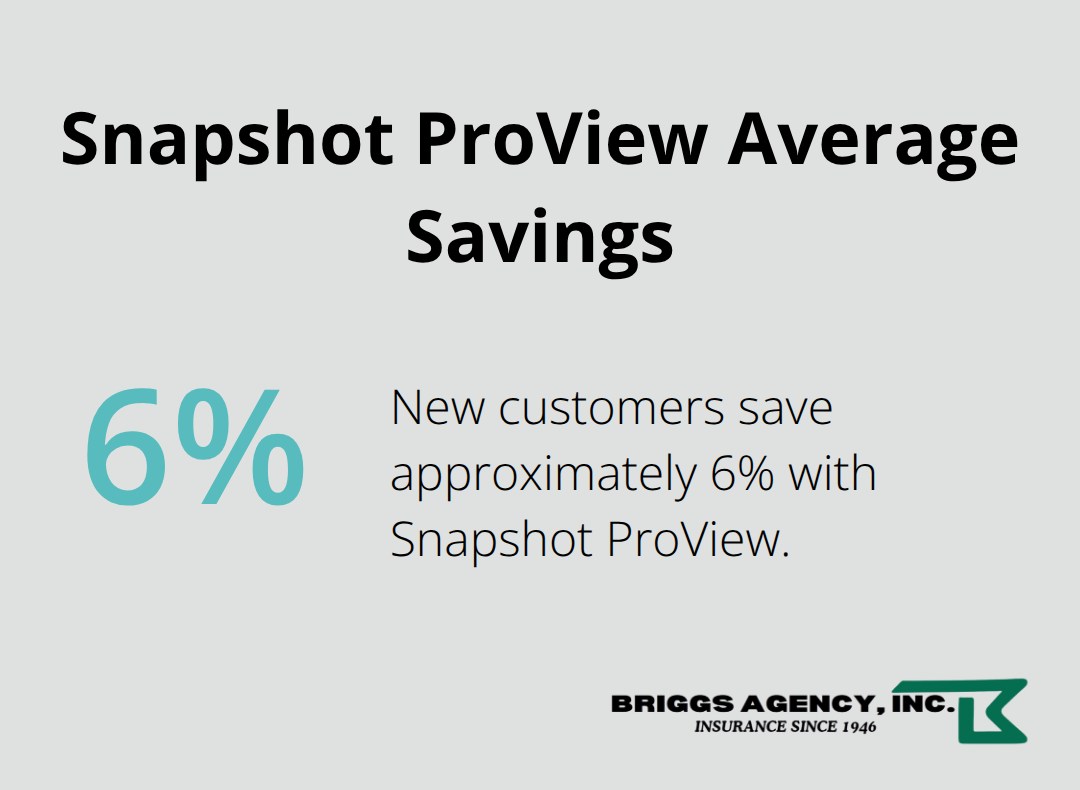

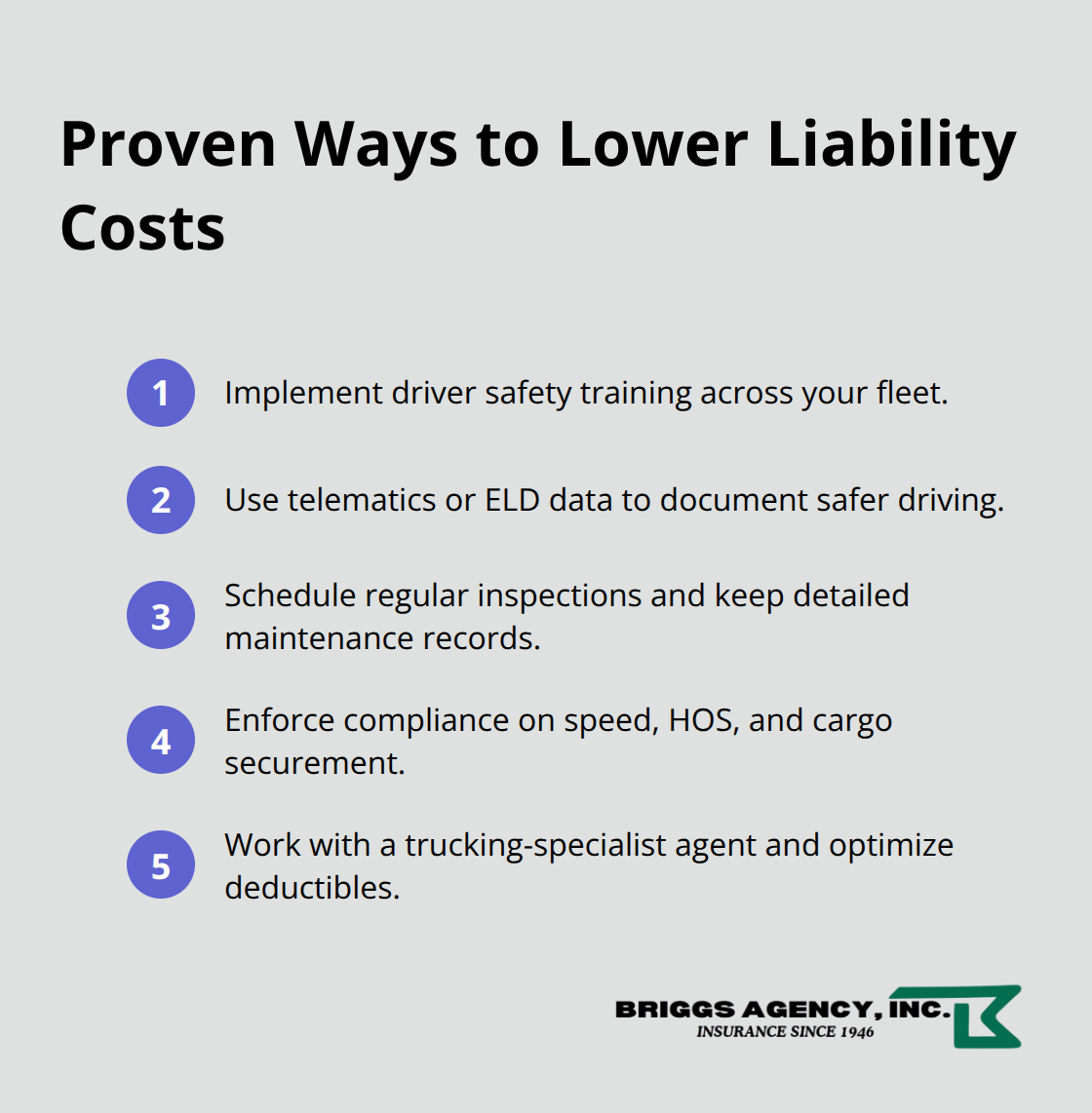

Driver training and safety programs lower your premiums because insurers measure risk through concrete metrics: accident frequency, violation citations, and claims history. When your drivers complete formal safety training, your company demonstrates to underwriters that you take prevention seriously, and that translates to measurable rate reductions. Progressive’s Smart Haul program shows this principle in action-new customers who share driving data via electronic logging devices save an average of $1,261 annually by proving safer operational practices. Even without telematics, Snapshot ProView saves approximately 6% for new customers and includes free fleet management tools for operations with three or more vehicles.

These aren’t marginal discounts; they represent real money that compounds year after year.

Your drivers need hands-on instruction on speed management, following distance, load securing, and hours-of-service compliance because citations for violations directly increase your risk profile with insurers. A single driver with multiple speeding tickets or hours-of-service violations signals to underwriters that your supervision practices may be weak, and that justifies premium increases across your entire fleet.

Vehicle Maintenance and Inspection Programs Prove Your Responsibility

Vehicle maintenance and inspection programs operate the same way-insurers reward documented proof that your trucks are mechanically sound and regularly serviced. A truck with faulty brakes, worn tires, or poor maintenance history increases your liability exposure substantially because mechanical failure contributes to accidents that might otherwise be preventable. Scheduling regular inspections, maintaining detailed maintenance records, and addressing safety issues immediately before they escalate shows insurers you manage your fleet responsibly.

The FMCSA requires these inspections anyway, so compliance becomes your foundation. Carriers reducing their insurance costs most aggressively treat maintenance as an investment that pays for itself through lower premiums and fewer downtime incidents.

Work with an Agent Who Understands Trucking Operations

An experienced insurance agent who specializes in trucking operations matters more than most operators realize because they understand which rate factors actually move your premiums and which ones don’t. An agent focused on general commercial insurance may quote you standard rates without recognizing that your specific operation qualifies for safety discounts or specialized coverage arrangements that reduce your overall cost. At Briggs Agency, Inc., our agents understand trucking operations because we’ve served this industry since 1946, and we compare multiple carriers to identify where your operation gets the best combination of coverage and pricing.

An agent who knows your business can also recommend deductible strategies-increasing your deductible from $1,000 to $2,500 or $5,000 lowers your premium significantly, and that makes sense if your operation can absorb that out-of-pocket exposure without straining cash flow. The conversation with your agent should focus on your actual risk profile, not generic coverage recommendations. Reviewing your current premiums, deductibles, and coverage limits helps identify which adjustments deliver the most value for your specific operation.

Final Thoughts

Commercial truck liability coverage protects your business when accidents happen, and one collision can expose you to hundreds of thousands of dollars in medical bills, vehicle damage, legal fees, and lost income claims. Without adequate protection, your personal assets and business operations face direct risk. The federal minimum of $750,000 provides only baseline protection; your actual exposure depends on the cargo you haul, your routes, and your driver’s experience.

The steps to reduce your liability costs work because they address what insurers actually measure: accident frequency, violation citations, and claims history. Driver training programs that produce measurable safety improvements, regular vehicle maintenance that prevents mechanical failures, and documented inspection records all signal to underwriters that your operation manages risk responsibly. These investments pay for themselves through premium reductions that compound year after year.

Review your current coverage limits against your actual liability exposure, assess whether your drivers need additional safety training, and schedule a conversation with an agent who understands trucking operations. We at Briggs Agency, Inc. have served trucking operations since 1946, and we compare multiple carriers to identify where your operation gets the best combination of coverage and competitive pricing.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.