Running a trucking operation in Indiana means managing real liability risks every day. Indiana truck liability insurance isn’t optional-it’s a legal requirement that protects your business, your drivers, and everyone sharing the road.

We at Briggs Agency, Inc. help carriers understand exactly what coverage they need and why it matters. This guide walks you through the protections available, state requirements, and the risks your policy should address.

What Truck Liability Insurance Covers in Indiana

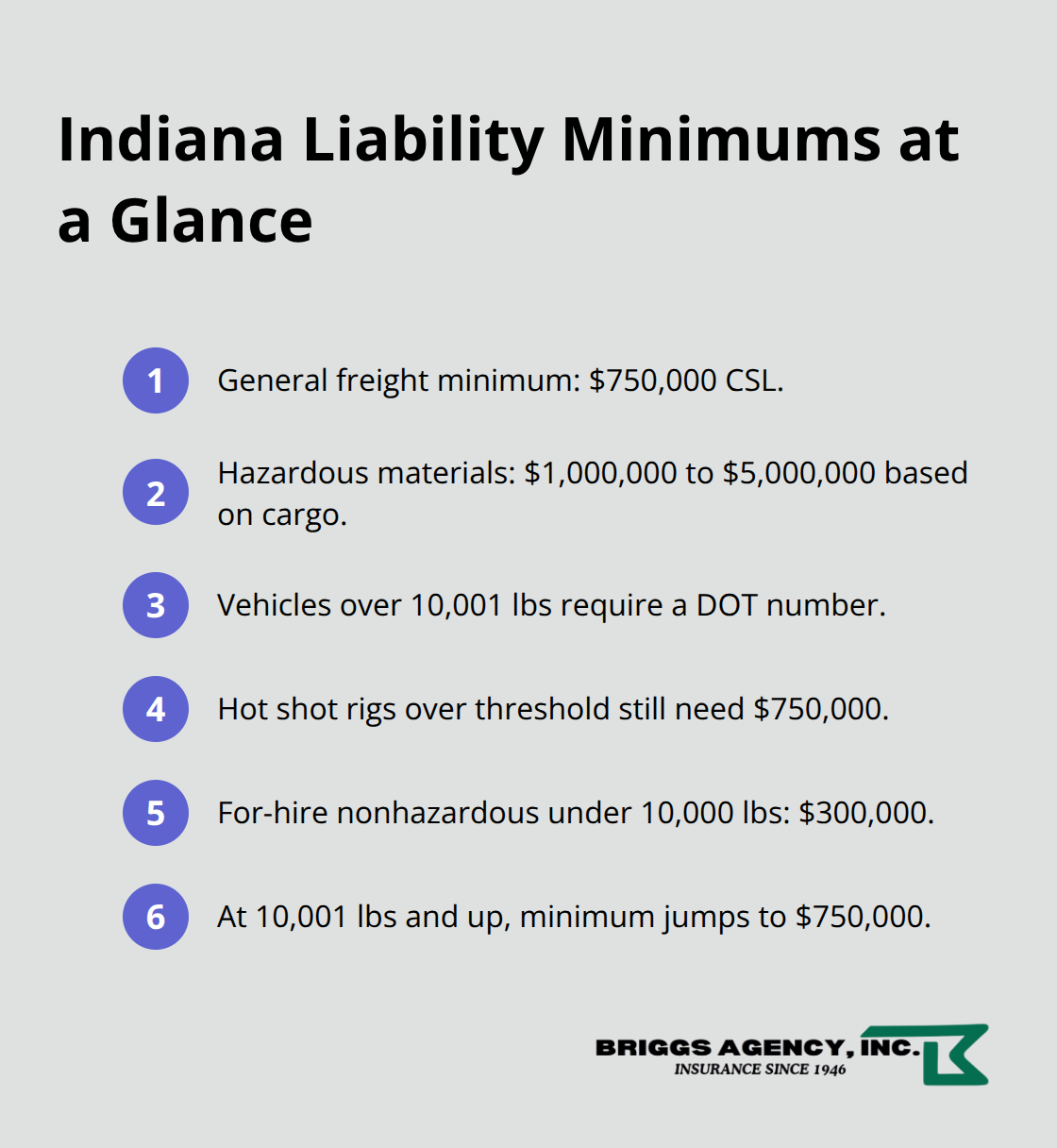

Truck liability insurance protects you when your operation causes bodily injury or property damage to someone else. This coverage pays for medical bills, lost wages, pain and suffering, vehicle repairs, and property replacement when you’re found legally responsible for an accident. Indiana’s minimum requirement is $750,000 in combined single limit coverage for general freight operations. If you haul hazardous materials, that jumps to $1,000,000 to $5,000,000 depending on the cargo type. Most freight brokers, however, demand $1,000,000 in coverage regardless of what the law requires-they’ve learned from experience that the minimum often isn’t enough when a serious crash happens. A fully loaded semi-truck weighs up to 80,000 pounds and creates vastly different damage than a passenger car at 4,000 pounds, which is why brokers push for higher limits and why you should listen to them.

Who Your Policy Actually Protects

Your liability policy covers third parties-the other driver, their passengers, property owners whose buildings or vehicles you hit. It does not cover your own truck, your own drivers’ medical bills, or your cargo. In Indiana, 5,897 crashes involving large trucks occurred in a recent year, resulting in 1,862 injuries and 135 deaths according to data cited by the Indiana University Public Policy Institute. The vast majority of those fatalities were occupants of passenger vehicles, not truck drivers. Your liability coverage pays when you’re responsible for those injuries or deaths. Rear-end collisions represent the most common tractor-trailer crash type in Indiana, driven by the longer stopping distances of heavy vehicles. If your driver follows too closely and hits someone, your liability policy covers their damages. This is why maintaining proper following distances and enforcing hours-of-service compliance directly reduce your insurance exposure and your premiums over time.

Optional Protections That Fill Critical Gaps

Uninsured and underinsured motorist coverage protects your drivers and company when an at-fault driver has little or no insurance. While Indiana doesn’t mandate this coverage for commercial trucks, it’s highly recommended because many drivers on Indiana roads carry minimal or no coverage. Medical payments coverage pays medical and funeral expenses for you and your passengers without waiting for fault determination. These optional protections fill gaps that basic liability leaves open and address real exposure on Indiana’s highways (particularly I-65, I-70, and I-90, where truck traffic concentrates). The right combination of coverages matches your actual risk exposure rather than just meeting minimum legal requirements.

How Liability Limits Connect to Real-World Crashes

A serious crash involving a fully loaded semi can generate damages far exceeding $750,000 when multiple vehicles and injuries occur. Brokers understand this reality and require higher limits to protect themselves and their shipper clients. When you carry only the state minimum and a major accident happens, your policy maxes out quickly, leaving you personally liable for the remainder. This gap between what the law requires and what brokers demand reflects the actual cost of serious truck crashes in Indiana.

Moving Forward with the Right Coverage

Your liability policy forms the foundation of your insurance program, but it’s only one piece. Understanding what it covers-and what it doesn’t-helps you identify the additional protections your operation needs. The next section examines Indiana’s specific regulatory requirements and how different vehicle types and cargo classifications affect your coverage obligations.

Indiana Truck Liability Requirements and Regulations

Indiana’s truck liability framework operates on a tiered system that changes dramatically based on vehicle weight and cargo type. For general freight, the state minimum is $750,000 in combined single limit coverage, according to the Indiana Department of Revenue Commercial Motor Vehicle Guide. Cross into hazardous materials territory and that floor jumps to $1,000,000 to $5,000,000 depending on what you’re hauling. The weight threshold matters too: a commercial vehicle over 10,001 pounds GVW requires a DOT number and falls under these minimums.

Operate a hot shot trucking setup with a trailer that tips the scale above that threshold and you’re subject to the same $750,000 requirement. For-hire carriers hauling nonhazardous property under 10,000 pounds can operate with $300,000, but add just one more pound and that minimum jumps to $750,000. This isn’t theoretical-it’s the difference between legal operation and a shutdown.

Federal and State Minimum Coverage Limits

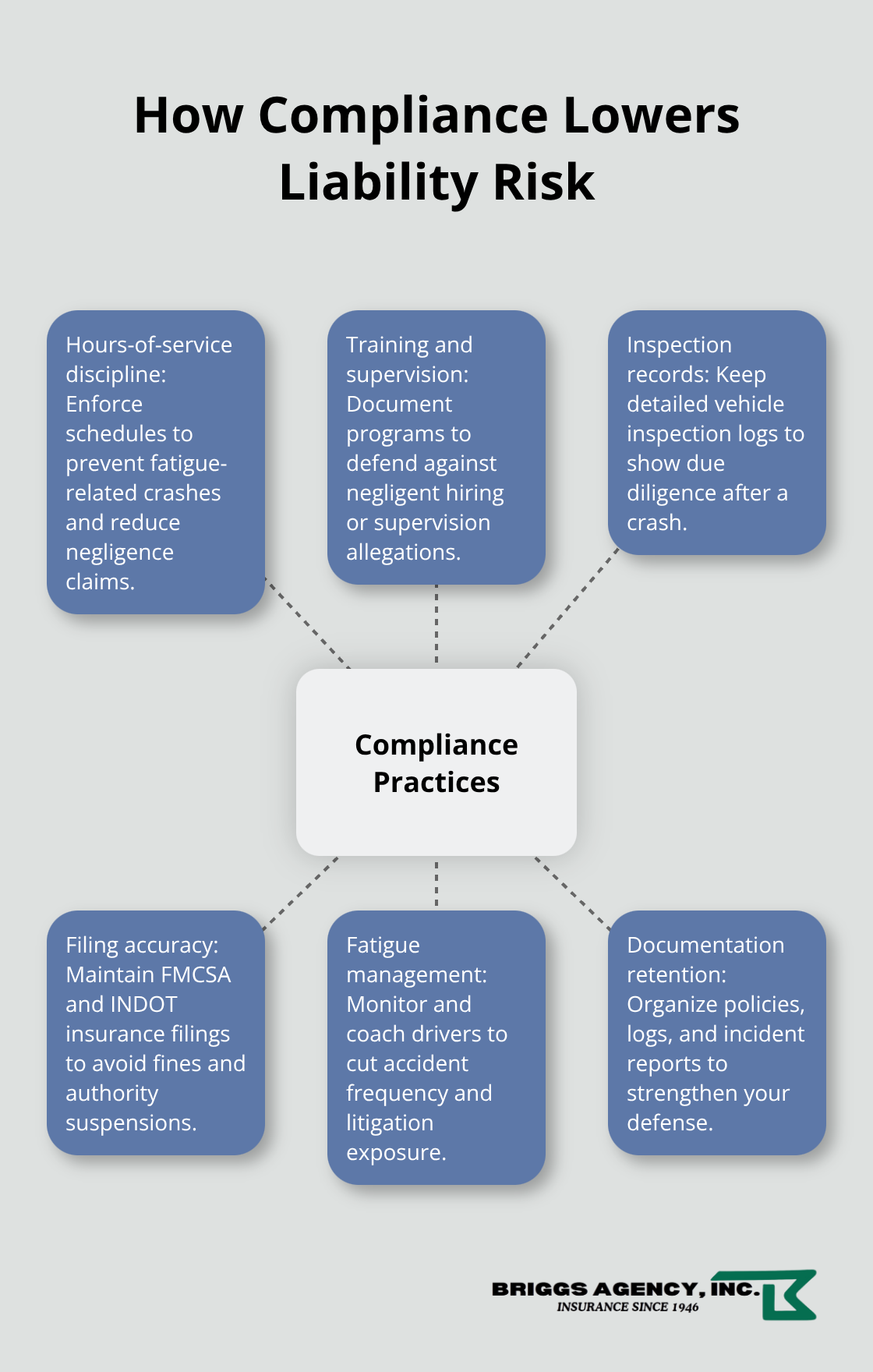

You’ll file Form BMC-91 or BMC-91X with FMCSA to prove your coverage, and noncompliance brings fines, suspension of operating authority, or revocation of your carrier license according to FMCSA enforcement standards. The Indiana Motor Carrier Application (Form IOA-1) comes next, followed by Unified Carrier Registration fees that depend on fleet size. A two-truck operation pays $37 per truck annually; three to five trucks cost $111 each. These aren’t optional paperwork exercises-they’re the legal backbone of operating in Indiana.

Federal FMCSA requirements layer on top of state minimums and actually drive the real-world floor for most carriers. Interstate operations require MC authority, which means your insurer files BMC-91X with FMCSA and attaches the MCS-90 endorsement guaranteeing coverage. You send Form E proof of insurance to INDOT, and FMCSA approves your MC authority.

Why Brokers Demand More Than the Law Requires

Here’s the practical reality: brokers and shippers regularly demand $1,000,000 in coverage regardless of state minimums because they’ve handled claims where $750,000 wasn’t remotely enough. Indiana ranks seventh nationally in the share of truck accident fatalities, with 5,897 large-truck crashes annually resulting in significant injury and fatality risk. A serious multi-vehicle crash on I-70 or I-65 can generate damages well beyond minimum limits. If your coverage maxes out and you’re liable for the remainder, your personal assets and future earnings become targets.

Understanding Your Compliance Obligations

Your compliance obligations extend beyond simply purchasing a policy. You must maintain current filings with FMCSA, keep your Form E proof current with INDOT, and renew your UCR registration annually. Carriers operating intrastate in Indiana still need a Federal DOT number, and the paperwork requirements don’t disappear just because you stay within state lines. Different vehicle types and cargo classifications trigger different thresholds, so misclassifying your operation can leave you underinsured and exposed to enforcement action. The tiered system exists because regulators recognize that a 5,000-pound cargo van presents different risk than an 80,000-pound fully loaded semi, yet both fall under commercial vehicle rules once they cross the 10,001-pound threshold.

Your next step involves identifying which specific coverages your operation actually needs beyond liability-because liability forms only the foundation of a complete truck insurance program.

Real Crash Costs and What Your Liability Insurance Actually Covers

Indiana’s truck crash data reveals the true cost of accidents that your liability policy must handle. Indiana truck crash data shows that large-truck and bus crashes highlight safety trends and identify factors associated with crashes. The most dangerous corridors run through I-65, I-70, I-90, I-69, and US-30, where concentrated freight traffic means higher collision frequency. Rear-end collisions dominate Indiana’s truck crash statistics because drivers underestimate stopping distances for 80,000-pound vehicles.

How Liability Coverage Responds to Real Accidents

When your driver follows too closely and causes a rear-end collision, your liability policy pays for the other vehicle’s repairs, occupant medical bills, lost wages, and pain-and-suffering damages. A single serious crash involving multiple vehicles can easily generate $1.5 million to $3 million in damages-which is exactly why brokers refuse to accept the state minimum of $750,000. One Indiana carrier with only state-minimum coverage faced a two-vehicle collision where the other driver’s medical treatment alone exceeded $900,000, leaving the carrier personally responsible for the overage. Your liability insurance protects your company from that financial devastation, but only if your limits match the actual risk.

Hazmat Routes and Compounded Exposure

Hazmat routes carry even steeper exposure because cargo damage, environmental cleanup, and third-party claims multiply damages exponentially. Regulatory violations compound your liability exposure in ways many carriers overlook. FMCSA enforcement data shows that missing or improper insurance filings trigger fines up to $10,000 per violation, suspension of operating authority, or complete license revocation according to FMCSA standards.

How Compliance Failures Increase Your Liability

Noncompliance with hours-of-service rules increases accident risk and gives plaintiffs ammunition to prove negligence. A driver working excessive hours who causes a crash gives the injured party grounds to sue not just for the accident itself but for your company’s negligent hiring, training, or supervision practices. These vicarious liability claims reach far beyond what a standard liability policy covers if you haven’t maintained proper compliance documentation.

Carriers who enforce fatigue management, maintain detailed vehicle inspection records, and document driver training reduce both accident frequency and litigation exposure. Your liability insurance becomes much more effective when your operation demonstrates due diligence in risk management.

Cargo Insurance Fills a Separate Gap

Motor truck cargo insurance operates separately from liability coverage and addresses an entirely different exposure. Cargo damage or loss during transit falls outside your liability policy’s scope-it protects third parties, not your shipper’s goods. A load of electronics worth $150,000 damaged in a rollover on I-70 creates immediate financial liability to your customer. Most freight brokers require motor truck cargo coverage with limits matching typical shipment values, usually $100,000 to $250,000. Carriers hauling temperature-sensitive products like pharmaceuticals or perishables face even steeper cargo risk because spoilage claims can exceed the physical shipment value. Your cargo policy reimburses the shipper and protects you from losing contracts when accidents happen. Without it, a single cargo loss can wipe out months of profit margins.

The Foundation Your Operation Needs

Liability insurance covers third-party damages, cargo insurance covers shipper losses, and together they form the minimum foundation for operating safely in Indiana’s freight market. Carriers who skimp on either coverage find themselves personally liable when accidents inevitably occur.

Final Thoughts

A complete Indiana truck liability insurance program protects your operation through layered coverages that address different risks. Liability forms the foundation, cargo insurance protects shipper relationships when accidents damage goods in transit, and physical damage coverage repairs your truck after a collision or comprehensive loss. Brokers demand $1,000,000 in coverage because real crashes generate damages that exceed the $750,000 state minimum, and adding the right protections prevents personal liability when accidents happen.

We at Briggs Agency, Inc. understand the specific risks you face on Indiana’s high-traffic freight corridors and help you build coverage that matches your actual exposure. Contact Briggs Agency, Inc. with details about your fleet size, routes, and cargo types so our local agents can compare options across multiple carriers and find competitive pricing tailored to your operation. Our experienced team walks you through compliance requirements, explains what each coverage protects, and helps you avoid gaps that leave you personally liable when accidents occur.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.