Auto Repair Shop Insurance: Protecting Your Garage and Crew

Running an auto repair shop means managing countless moving parts-literally and figuratively. One wrong move, one accident in the bay, or one equipment failure can drain your finances fast.

At Briggs Agency, Inc., we’ve seen repair shops face unexpected costs that could have been prevented with proper auto repair shop insurance. The right coverage protects your business, your team, and your customers when things go wrong.

What Your Shop’s Insurance Actually Protects

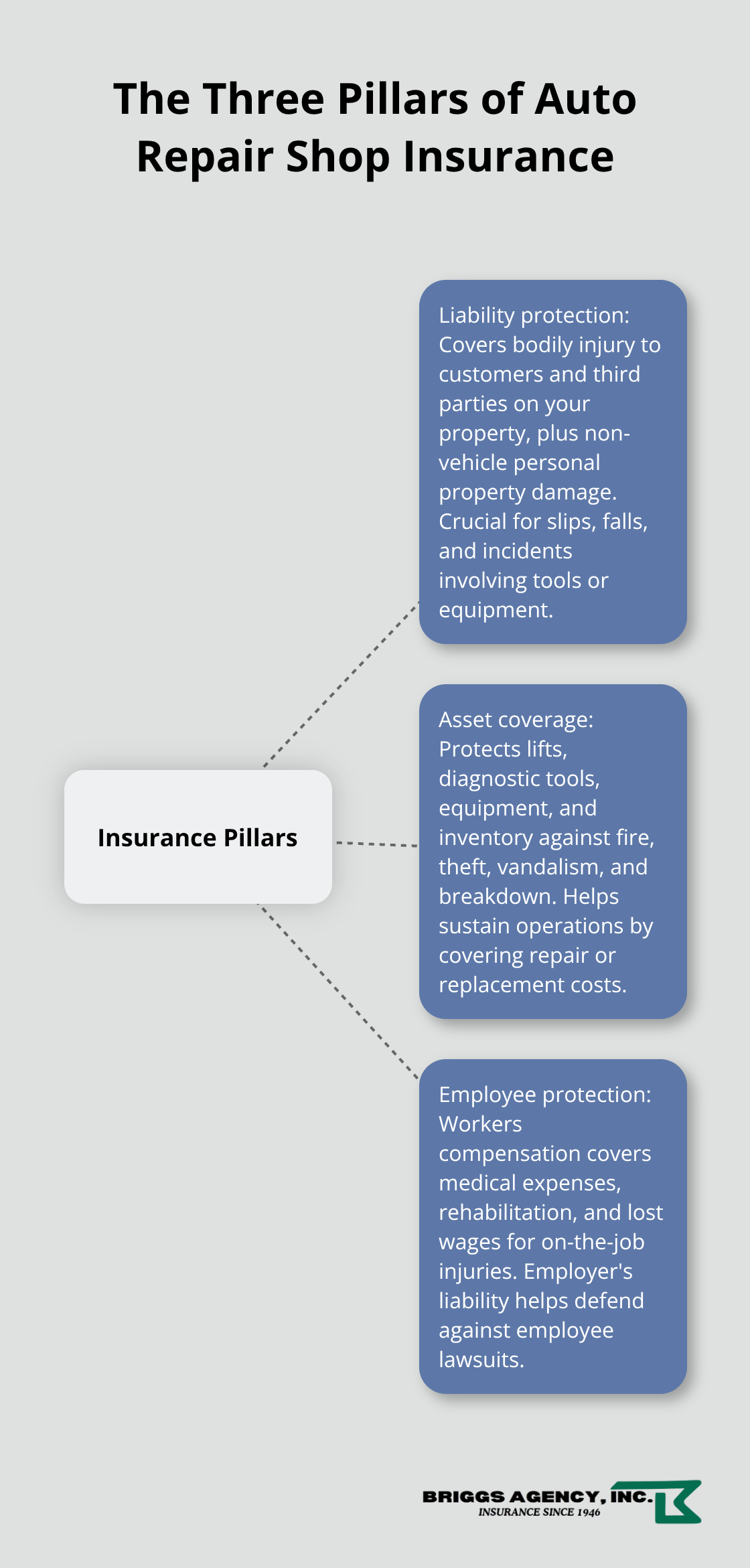

Auto repair shop insurance isn’t one-size-fits-all, and that’s the point. Your coverage needs to match the specific hazards your operation faces daily. The biggest mistake shop owners make is assuming standard business insurance covers vehicle-related damage or injuries on their property. It doesn’t. General liability policies explicitly exclude vehicles in your care, which is why specialized garage coverage exists. When a customer’s car gets damaged during service, or a technician gets hurt on the job, you need protection designed for these exact scenarios. The three pillars of proper auto repair shop insurance are liability protection, asset coverage, and employee protection-understanding what each actually covers separates shops that survive incidents from those that don’t.

Protecting Against Customer Injury and Vehicle Damage Claims

Garage liability insurance covers bodily injuries to customers or third parties on your property, plus damage to their personal property that isn’t their vehicle. If a customer slips on an oily floor and breaks their arm, or tools fall and damage someone’s phone, this coverage handles it. More critically, garage keepers insurance protects vehicles under your custody during service, storage, or test drives. Fire, theft, vandalism, and negligent handling cause the most expensive vehicle damage claims at repair shops. You can choose direct primary coverage, which pays losses regardless of fault and speeds claim resolution, or direct excess coverage, which acts as secondary protection after the customer’s insurance pays. Direct primary costs more but eliminates disputes about who’s responsible and keeps customers satisfied. One major incident-a vehicle fire in your bay, a stolen customer car, or damage during a test drive-can cost tens of thousands and destroy your reputation without this protection.

Protecting Your Tools, Equipment, and Business Assets

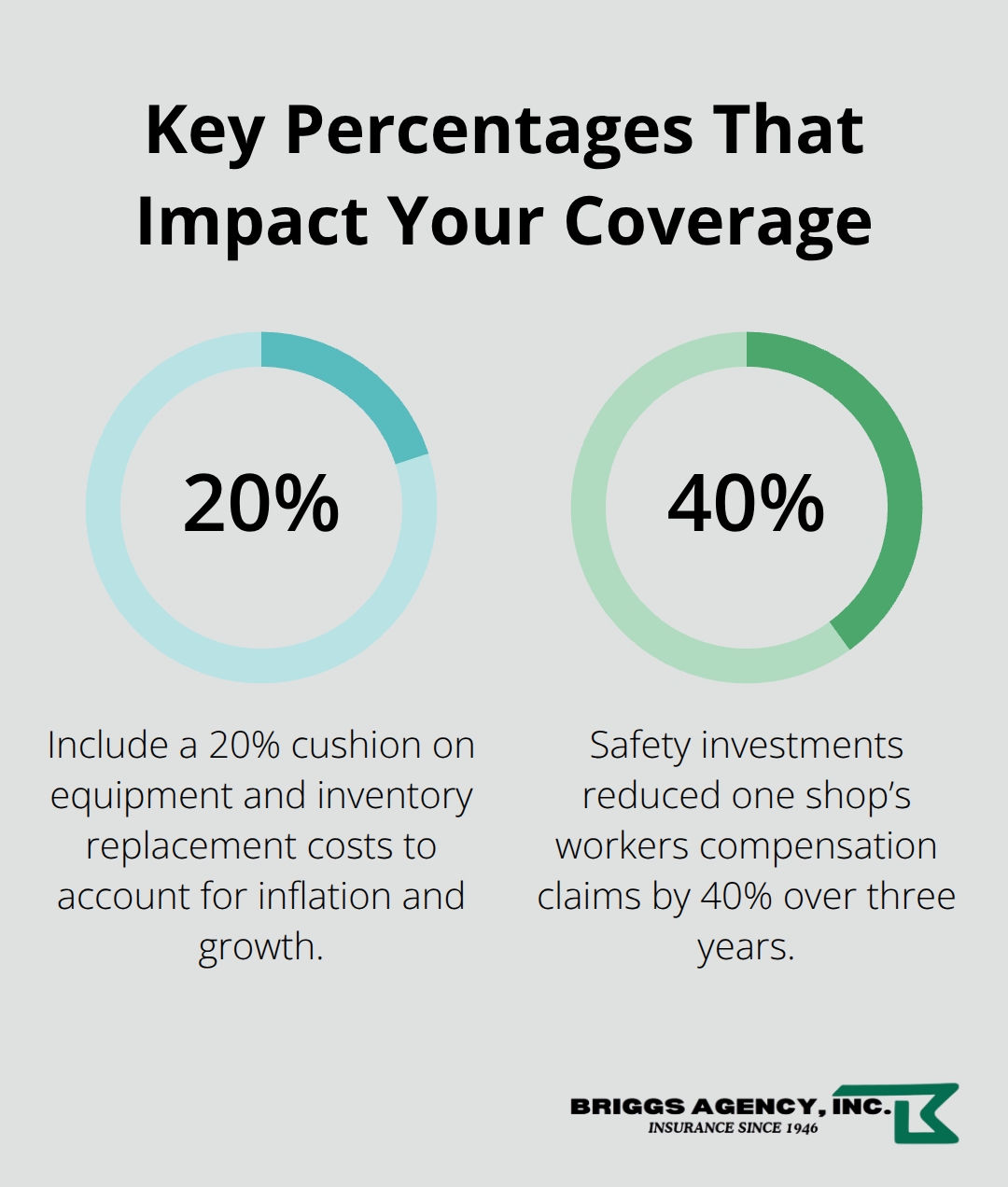

Your shop’s equipment, diagnostic tools, lifts, and inventory represent your ability to operate. Commercial property insurance and inland marine coverage protect these assets from fire, theft, vandalism, and equipment failure. A shop fire or break-in doesn’t just damage what’s stolen; it stops you from earning revenue while repairs happen. Many shop owners underestimate inventory value and choose limits that leave them exposed. Calculate the replacement cost of every lift, tool set, diagnostic machine, and parts inventory, then add 20 percent for inflation and growth. If you store customer vehicles on-site regularly, property coverage should extend to protecting against loss of income during recovery, so you maintain cash flow when you can’t serve customers.

Employee Safety and Workers Compensation Requirements

Workers compensation insurance is legally required in nearly every state for shops with employees. The policy covers medical expenses, rehabilitation, and lost wages when employees get injured on the job, plus employer’s liability protection shields you from employee lawsuits. Some states like New York require coverage even for part-time staff, while Alabama requires it once you hit five employees. OSHA compliance-proper ventilation for welding fumes, chemical hazard management, lift safety training, and lockout procedures-directly reduces claims and can lower your premiums over time. Shops that invest in employee safety training and proper personal protective equipment file fewer claims and attract better technicians, which means your next step involves assessing the specific risks your operation faces.

Why Standard Business Insurance Falls Short

Standard business insurance policies were designed for offices and retail stores, not shops where technicians work on vehicles worth thousands of dollars. General liability explicitly excludes vehicle-related damage, which means a customer’s car damaged during service, a vehicle fire in your bay, or a stolen vehicle while parked on your property receives zero coverage under a typical business policy. Auto repair shops face hazards that don’t exist in most other industries: flammable liquids stored on-site, heavy equipment that can malfunction, customer vehicles of significant value under your control, and specialized work environments.

Fire and Theft Create the Biggest Financial Exposure

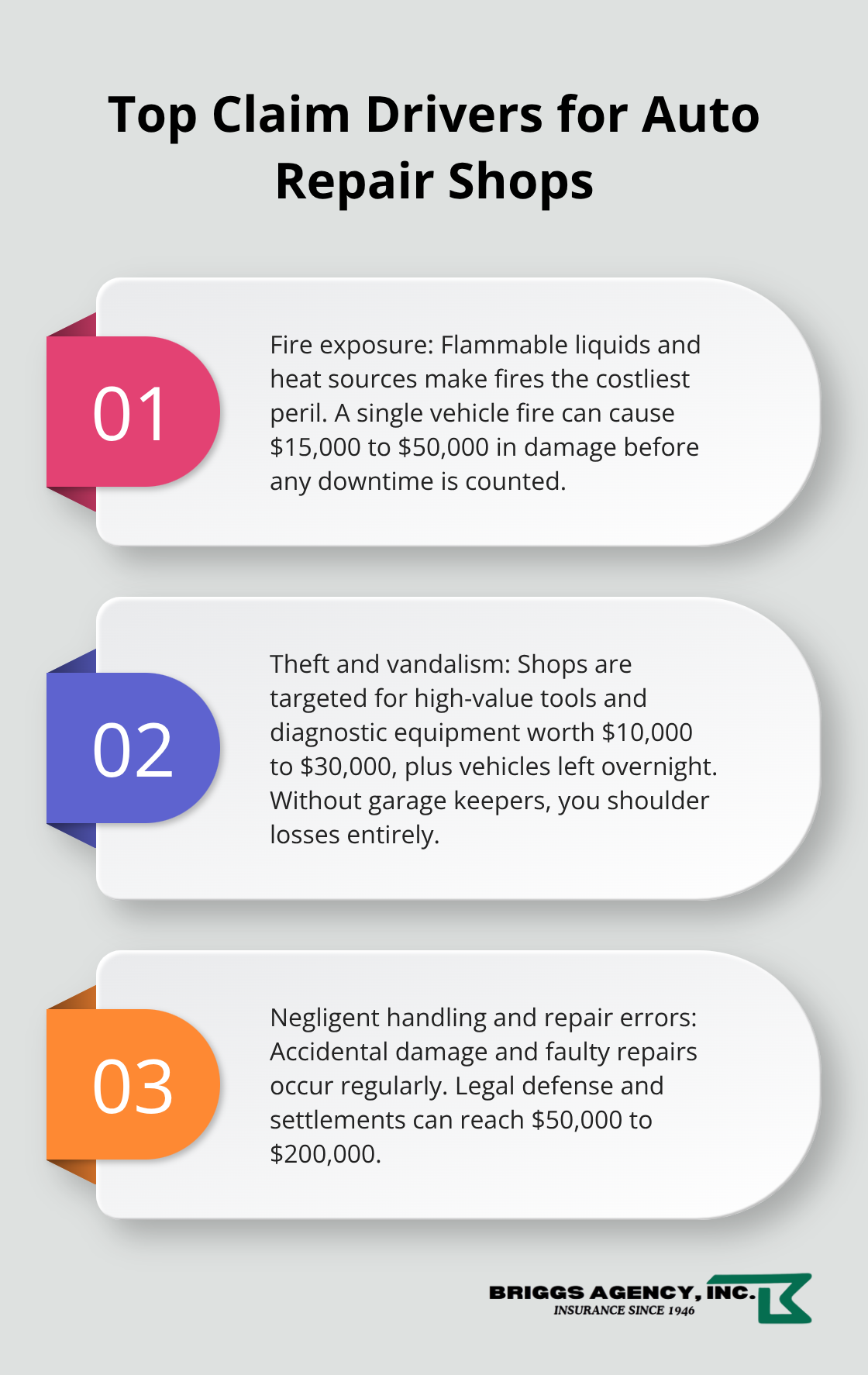

Fire remains the costliest peril for repair shops. Flammable liquids like gasoline and brake fluid combined with heat sources from welding and grinding operations create significant fire hazards. One vehicle fire during service or in your storage area costs $15,000 to $50,000 in vehicle damage alone, plus potential liability for the customer’s rental car and diminished value.

Theft and vandalism rank second. Criminals target repair shops specifically because they contain high-value diagnostic equipment and tool sets worth $10,000 to $30,000, plus customer vehicles left overnight. Without garage keepers insurance, you absorb the entire loss even though the vehicle wasn’t yours.

Negligent Handling and Repair Errors Generate Frequent Claims

Negligent handling during repairs creates frequent claims across the industry. A technician accidentally damages a customer’s paint during service, or a lift failure causes collision damage-these scenarios happen regularly and cost shops thousands in settlements and reputation damage. Garage liability insurance with products-completed operations coverage protects against claims from defective parts or faulty repairs, covering legal defense costs and settlements that can reach $50,000 to $200,000 depending on severity.

State Laws and OSHA Requirements Drive Coverage Needs

State laws recognize these unique risks, which is why specialized garage liability and garage keepers coverage exist. Most states require workers compensation for any shop with employees, with New York mandating it even for part-time staff and Alabama requiring it once you reach five employees. OSHA standards for auto shops cover hazard communication for chemicals, lockout procedures for equipment maintenance, proper ventilation for welding fumes, and fall protection from lifts and elevated work areas. Shops that document OSHA compliance and implement formal safety training programs see measurable premium reductions because insurers recognize reduced claims risk.

The Real Cost of Being Underinsured

Medical costs for a serious workplace injury average $40,000 to $100,000 depending on severity. A lawsuit over defective repairs or negligent handling can reach $50,000 to $200,000 in settlements and legal fees. Specialized coverage costs between $1,500 and $4,000 annually depending on shop size and operations-a fraction of what one major incident costs. A single uninsured claim can force a small repair shop to close. One shop that invested in proper ventilation systems, chemical tracking procedures, and employee safety training reduced workers compensation claims by 40 percent over three years, lowering annual premiums significantly. The financial impact extends beyond premium savings to business continuity and reputation protection.

Understanding what standard policies exclude is only half the battle. The real question becomes how to assess which specialized coverages your specific operation actually needs.

Choosing the Right Mix of Coverage

Assess Your Shop’s Specific Operations and Assets

Start by listing every revenue-generating activity your shop performs and every asset on-site. If you perform oil changes and tire rotations, you need different coverage than a shop that handles engine rebuilds and stores vehicles overnight. If you conduct test drives, that activity creates liability exposure that static repair work doesn’t. Document whether you store customer vehicles on your lot, how many at any given time, and their average value. Count every diagnostic machine, lift, tool set, and piece of equipment-replacement costs add up fast, and underestimating inventory leaves you exposed when loss happens.

For workers compensation, calculate your total annual payroll and note how many employees work in each role since classification rates vary by job type. A technician performing welding pays a different rate than an office administrator. Next, identify your shop’s specific hazards. Chemical storage matters only if you keep quantities on-site; a shop that orders small batches monthly has lower exposure than one maintaining bulk supplies of solvents and brake fluid.

Evaluate Your Unique Risk Profile

Lift operations present risk if you work on vehicles daily but not if you handle only diagnostic work. Fire hazard depends on your equipment mix-shops with welding bays face greater risk than those focused on computerized diagnostics. Write down your state’s workers compensation requirements and whether you operate in a monopolistic fund state like Ohio or Washington, which affects how you purchase employer’s liability coverage. Get your shop’s loss history if you’ve had prior coverage; insurers review this when underwriting, and transparency about past claims prevents surprises later.

Compare Quotes from Multiple Carriers

Once you understand your operation, obtain quotes from at least three carriers rather than accepting the first offer. Request quotes that specify coverage limits for garage liability, garage keepers, workers compensation, commercial property, and commercial auto separately so you can compare what each carrier includes. Ask each insurer for their experience with repair shops specifically-carriers that specialize in auto service understand your risks better than generalists. Coverage can start within 24 hours of application for shops using online platforms, but this speed shouldn’t override the value of multiple quotes.

Compare the actual dollar limits, deductibles, and exclusions rather than just the premium price. A $500 deductible saves money monthly but costs more when a claim happens, while a $2,500 deductible makes sense if your cash flow can absorb it. When comparing garage keepers options, determine whether direct primary or direct excess coverage fits your customer relationships-direct primary costs more but eliminates fault disputes and keeps customers happier during claims, which matters for repeat business.

Leverage Loss Control Credits and Accurate Information

Ask about loss control credits for shops implementing formal safety programs; OSHA-compliant ventilation systems, documented chemical tracking, and employee safety training can reduce your workers compensation premium by 10 to 15 percent annually once you demonstrate consistent compliance. Request quotes that reflect your actual payroll and operations, not generic estimates, since premium accuracy depends on accurate information about what you do. At Briggs Agency, Inc., we represent multiple top-rated carriers, which means you receive genuine comparison quotes rather than quotes from a single insurer with limited flexibility.

Final Thoughts

Auto repair shop insurance protects your business from the financial devastation that one major incident can cause. The right coverage combination addresses your specific operation, not some generic template, and garage liability, garage keepers, workers compensation, and property insurance work together to cover customer injuries, vehicle damage, employee protection, and your shop’s assets. Without this specialized protection, a single fire, theft, or negligent handling claim forces you to close your doors permanently.

Document your shop’s operations, assets, and payroll, then request quotes from multiple carriers that specialize in auto repair. Compare the actual coverage limits and exclusions rather than just the premium price, and ask about loss control credits for safety programs since OSHA compliance and documented employee training reduce claims and lower your costs over time. Accuracy matters when applying for quotes, so provide real numbers about what you do and what you own rather than estimates.

We at Briggs Agency, Inc. have served Crown Point and surrounding communities since 1946, helping repair shops and other businesses find the right protection at competitive rates. As an independent agency representing multiple top-rated carriers, we compare genuine options tailored to your operation rather than pushing a single insurer’s products, and our experienced local agents understand the specific risks repair shops face because we work with them regularly. Contact Briggs Agency, Inc. today to discuss your shop’s coverage needs and get quotes that reflect your actual business.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.