Garage Liability Insurance Indiana: What Your Shop Should Include

Running a garage in Indiana means managing real risks every single day. From customer vehicles on your lot to employee injuries and equipment damage, the liability exposures add up fast.

At Briggs Agency, Inc., we’ve helped shop owners across the state understand what garage liability insurance Indiana actually covers and where most policies fall short. This guide walks you through the coverage types you need, the gaps to watch for, and how to build protection that fits your operation.

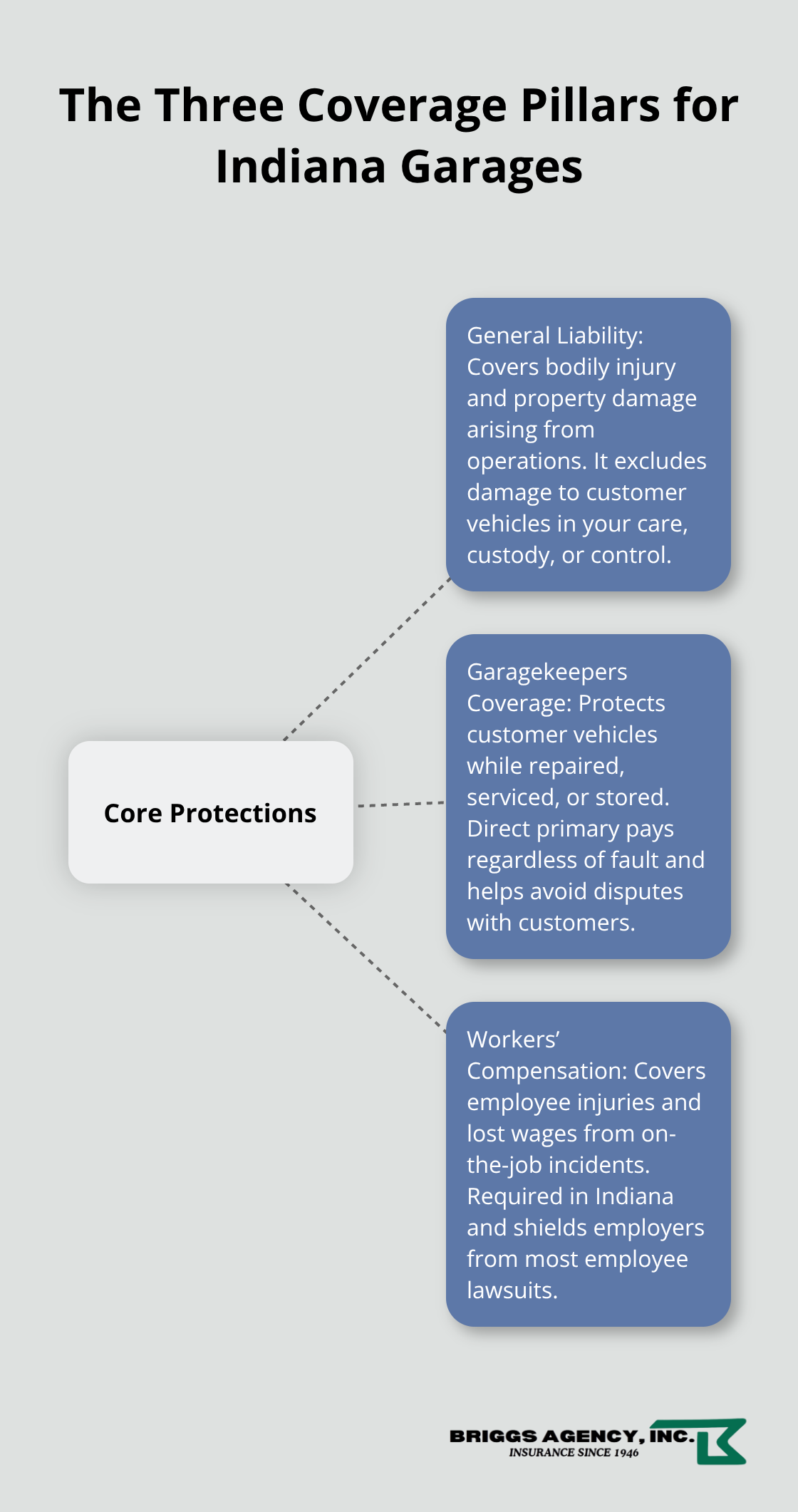

The Three Coverage Pillars Your Indiana Shop Needs

Why General Liability Alone Isn’t Enough

General liability covers bodily injury and property damage claims that arise from your shop’s operations-a customer slips on your floor, or your equipment damages their property while it’s in your care. However, general liability explicitly excludes damage to customer vehicles under its care, custody, or control provision, which leaves your biggest exposure unprotected. Indiana Code Title 27 defines garage liability as coverage for shops that sell, lease, repair, service, deliver, test, road test, park, or store motor vehicles. The standard ISO Garage Coverage Form CA 00 05 bridges this gap by combining general liability with auto exposure in one policy, so you don’t juggle separate policies with overlapping exclusions-the garage liability form handles the vehicle-related risks that traditional general liability won’t touch.

Garage Keepers Coverage Closes the Protection Gap

Garage keepers coverage addresses the exact gap that general liability creates by covering vehicles in your care, custody, or control while they’re being repaired, serviced, or stored at your business. When a customer leaves their vehicle with you for service, storage, or a test drive, that vehicle becomes your responsibility, and damage from negligence, theft, vandalism, or weather requires protection. Three forms exist-legal liability, direct primary, and direct excess-and they offer different approaches. Legal liability pays only if you’re found negligent, while direct primary pays regardless of fault and resolves claims faster without disputes. Most Indiana shops benefit from direct primary because it simplifies customer relationships and claim resolution; if a test-drive accident damages the vehicle, direct primary covers it without finger-pointing.

Workers Compensation Protects Your Team and Your Business

Workers compensation is the third pillar and protects your employees from injuries on the job, covering medical expenses and lost wages. Indiana requires this coverage if you have employees, and it also shields you from employee lawsuits. Workplace injuries in garages occur regularly-slip-and-fall incidents, tool-related injuries, and strain injuries from repetitive tasks happen more often than many shop owners realize. Workers comp keeps both your employees and your business finances secure when accidents happen.

These three pillars work together to address the specific exposures your shop faces, and understanding how each one fills a different gap helps you build a protection strategy that actually matches your operation. The next section examines where most Indiana shops discover gaps in their coverage-and how to spot them before they become costly problems.

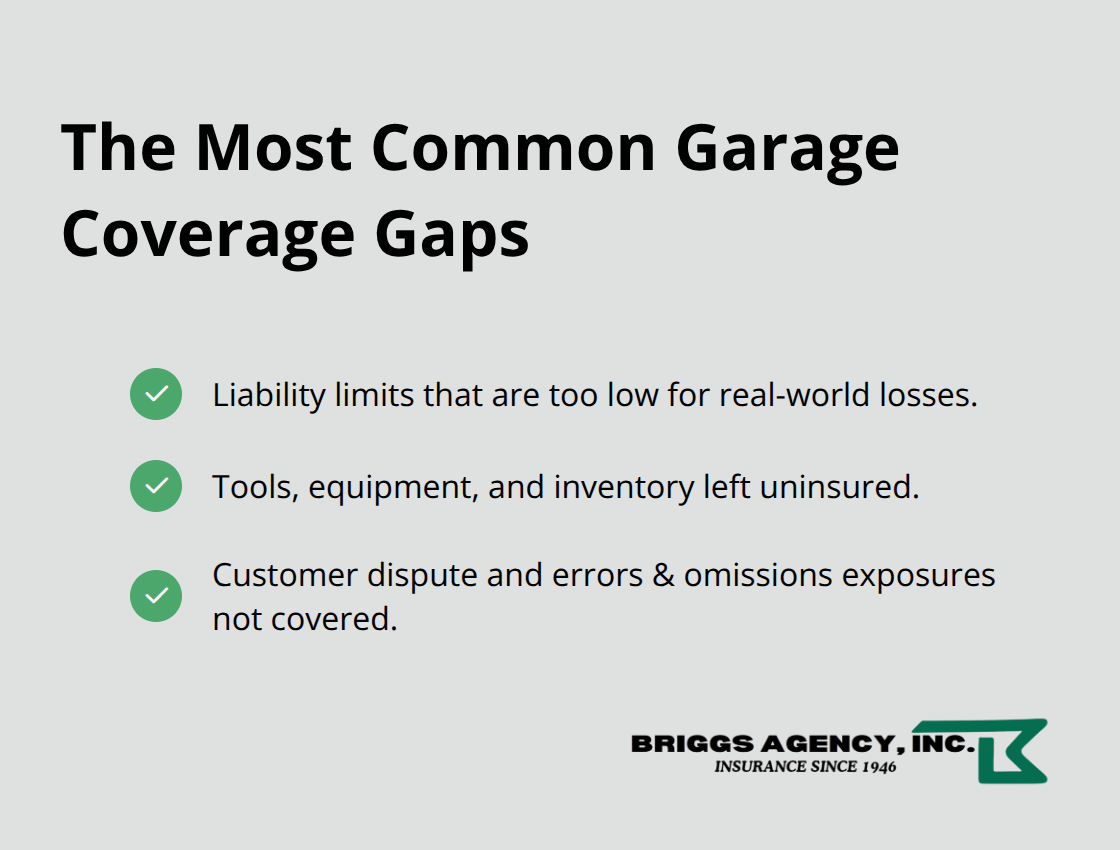

Common Gaps in Garage Coverage

Liability Limits That Don’t Match Your Actual Risk

Most Indiana shop owners carry minimum liability limits of $100,000 per occurrence, which sounds reasonable until a serious accident happens. A single major incident-a test-drive collision that injures multiple people, or a fire that destroys customer vehicles on your lot-can easily exceed $100,000 in liability costs. Indiana shops handling high-value vehicles or performing complex repairs need inadequate liability limits of at least $300,000 per occurrence and $1,000,000 aggregate to match the actual risk. Without adequate limits, you face personal liability for costs above your policy cap, which can wipe out your business savings and future earnings.

Tools, Equipment, and Inventory Remain Unprotected

Shop owners often assume their garage liability policy covers tools, equipment, and inventory damage. It doesn’t. Your policy protects against liability claims, not your own property losses. A theft of diagnostic equipment worth $15,000 or a fire that destroys your lifts and tools leaves you unprotected unless you add inland marine or business property coverage to your package. These gaps mean you absorb the full cost of replacing critical equipment that keeps your operation running.

Customer Disputes and Legal Claims Fall Outside Standard Coverage

Many shops overlook the exposure created by customer disputes and legal claims that fall outside traditional liability. When a customer claims your repair caused an engine failure or disputes your work quality, they may sue for the cost of repairs elsewhere or vehicle value loss. Your garage liability policy covers bodily injury and property damage, not breach of warranty or contract disputes. Products-completed operations coverage and errors and omissions insurance protect you against these claims and the legal costs that accompany them.

The Real Cost of Coverage Gaps

These three gaps-inadequate limits, unprotected property, and uninsured contract disputes-represent the most common exposures that catch shop owners off guard.

Each one stems from a different assumption about what garage liability covers, and each one can create substantial financial exposure. Identifying your specific gaps requires an honest inventory of what you own, what you store, and what services you perform.

The next section walks you through how to assess your shop’s unique risks and select coverage that actually closes these gaps instead of leaving your business exposed.

How to Choose the Right Garage Liability Policy

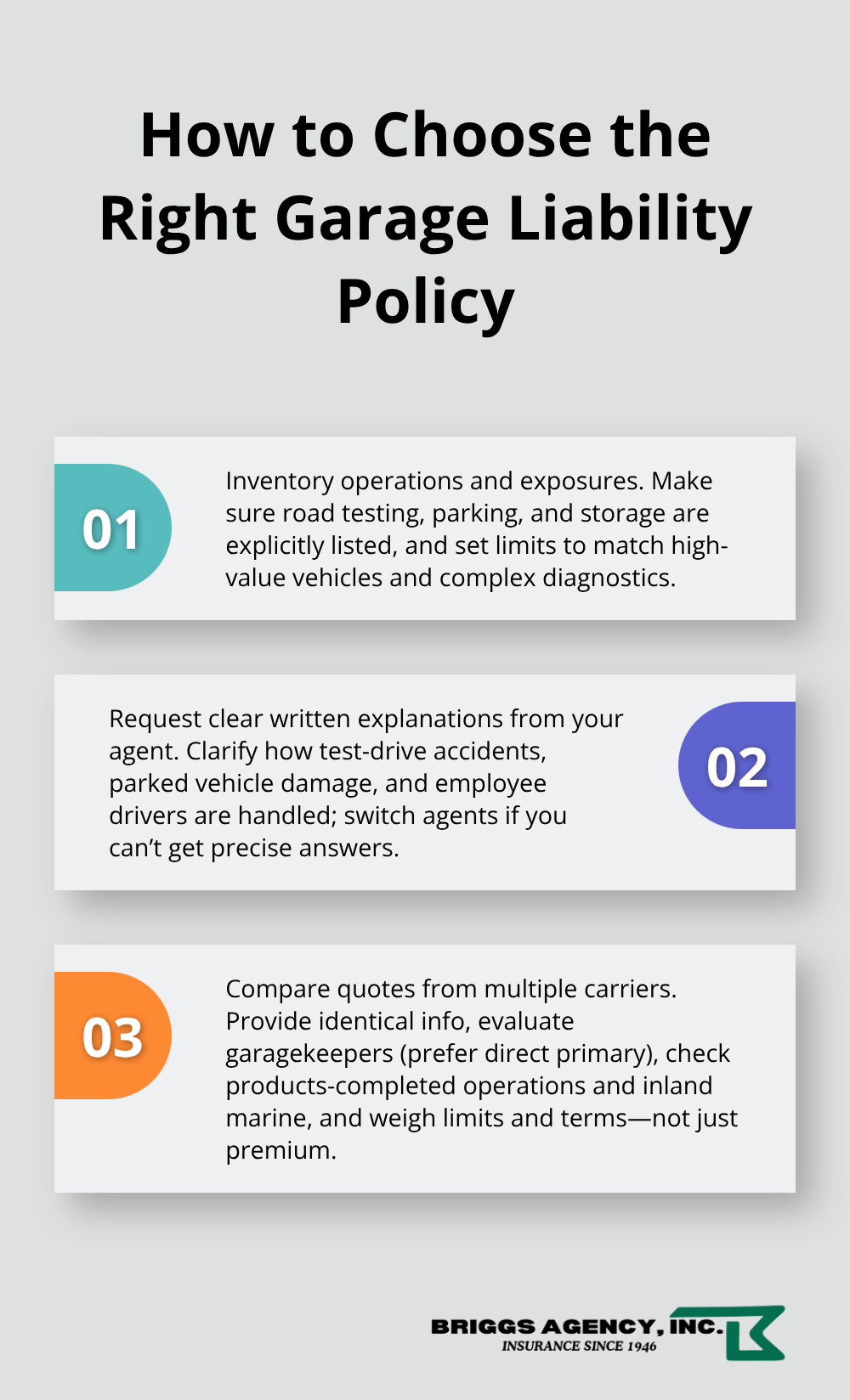

Inventory Your Shop’s Operations and Exposures

Start by listing exactly what you do, what you own, and what vehicles pass through your facility. If you perform road tests or customer test drives, road testing must appear explicitly in your policy-this is non-negotiable. If you store vehicles long-term, parking and storage must be listed as covered activities. If you handle high-value vehicles or complex diagnostics, your liability limits need to reflect that exposure, not minimum state requirements. Most Indiana shop owners carry $100,000 per occurrence limits, but a single multi-vehicle accident or fire generates $300,000 to $500,000 in liability costs within minutes. The ISO Garage Coverage Form CA 00 05 that most carriers use defines garage operations broadly to cover all activities necessary or incidental to running your garage, but carriers interpret this language differently. Request a detailed coverage summary from your agent that explicitly lists your shop’s activities-repair, service, storage, test drives, delivery-and confirms each one receives coverage. Vague language like “and related activities” creates risk; demand specificity instead.

Request Clear Written Explanations of Coverage

Your agent must provide a clear written explanation of what counts as covered garage operations at your specific shop. Ask your agent to explain how the policy handles test-drive accidents, what happens if a customer vehicle is damaged while parked on your lot, and whether employees who drive customer vehicles receive coverage. If an agent cannot articulate these details in writing, find a different agent. Your insurance should match your operation precisely, and that requires someone who listens to your business, not someone selling a standard package.

Compare Quotes from Multiple Carriers

Contact three to five carriers and provide identical information about your shop’s operations, vehicle volume, and services to receive apples-to-apples quotes. When reviewing quotes, compare not just premium but coverage components: Does the policy include garagekeepers coverage, which covers vehicles in your care, custody, or control while being repaired, serviced, or stored at your business? Direct primary costs more but eliminates claim disputes and protects customer relationships. Does the policy include products-completed operations coverage to protect against defective repair claims? Are tools and equipment protected under inland marine coverage, or do you need to add that separately? What are the actual liability limits per occurrence and aggregate? A carrier quoting $1,200 annually with $100,000 limits is not cheaper than one quoting $1,600 with $300,000 limits if the lower-limit policy leaves you exposed.

Work with a Local Agent Who Understands Your Shop

A good local agent asks detailed questions about your specific services, inquires about claims history, and explains gaps in standard coverage before you purchase. Your agent should take time to understand your shop’s operations and the vehicles you handle. If an agent cannot explain why you need garagekeepers coverage or what products-completed operations covers, that agent cannot protect your business effectively. At Briggs Agency, Inc., we represent multiple top-rated carriers and compare options to show you the real trade-offs between cost and protection. We work with shop owners to build policies that match their operations precisely, not generic packages that leave gaps.

Final Thoughts

Your Indiana garage faces exposures that standard business insurance simply doesn’t address. General liability excludes vehicle damage, workers compensation covers only employee injuries, and property coverage protects your building but not the vehicles in your care. Garage liability insurance Indiana combines auto exposure with general liability in one policy, eliminating the gaps that catch shop owners off guard.

Protection only works when your policy matches your actual operation. If you perform road tests, that activity must appear explicitly in your coverage. If you store vehicles long-term, parking and storage must receive listing as covered activities. If you handle high-value vehicles, your liability limits must reflect that exposure rather than minimum state requirements, and an agent who understands your shop’s specific services can show you why direct primary garagekeepers coverage costs more but eliminates claim disputes and protects customer relationships.

We at Briggs Agency, Inc. represent multiple top-rated carriers and work with shop owners across Indiana to tailor policies that match your operation. Contact us to review your current coverage, identify gaps, and build protection that actually fits your business.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.