Garage Owners Policy Indiana: Simplifying Your Small-Business Protections

Running an auto repair shop in Indiana means managing risks that standard commercial policies simply don’t cover. A garage owners policy Indiana is built specifically for your business, protecting everything from customer vehicles on your lot to your team during test drives.

At Briggs Agency, Inc., we’ve helped countless shop owners discover the gaps in their coverage and fill them before problems arise. This guide walks you through what you actually need to protect your business.

What Garage Owners Really Need to Know About Coverage

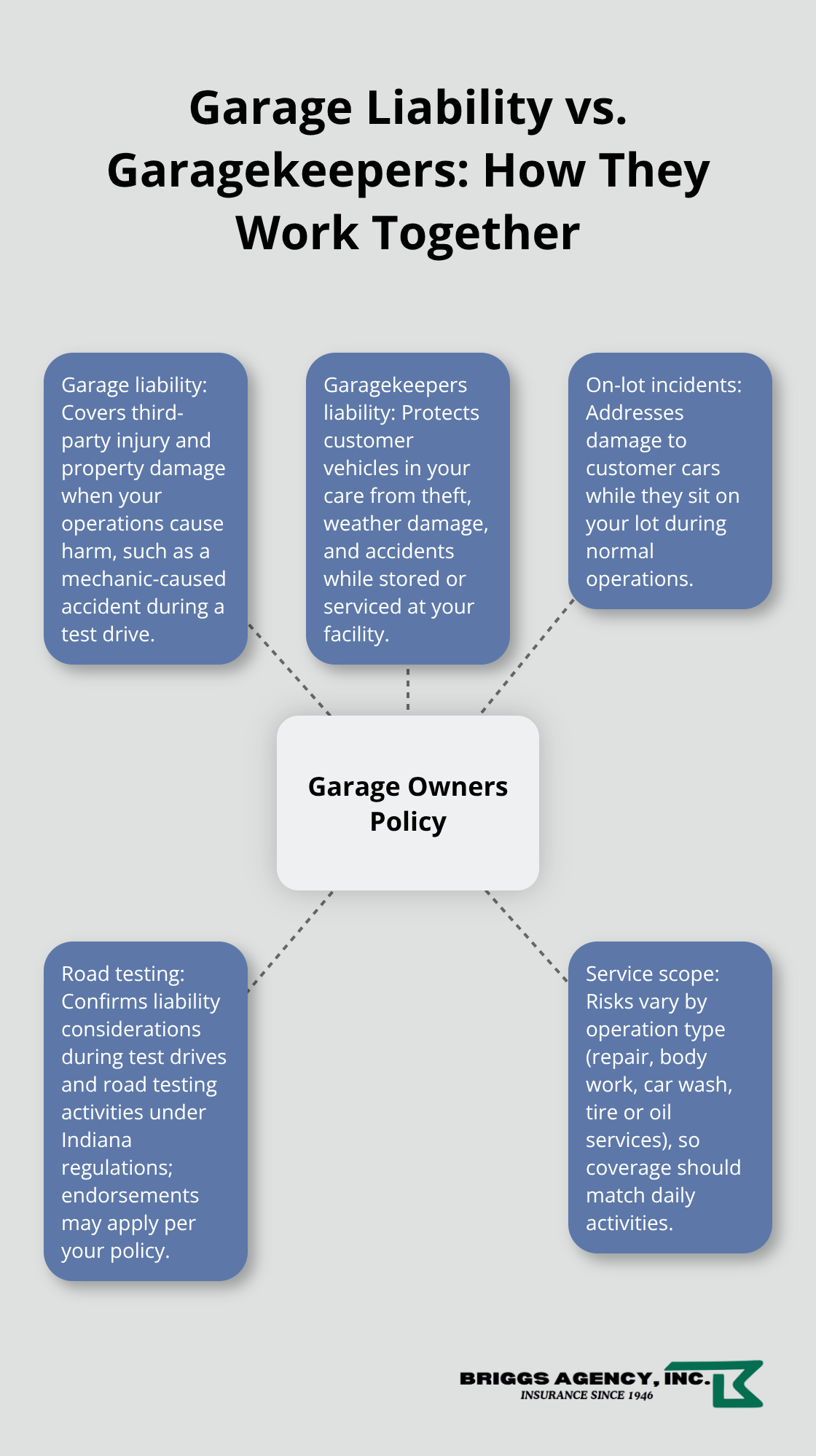

How Garage Liability and Garagekeepers Coverage Work Together

A garage owners policy in Indiana covers the specific risks that come with running an auto repair shop, body shop, car wash, tire shop, or oil change station. According to Indiana Code Title 27, § 27-8-9-6, garage liability policies protect businesses engaged in selling, leasing, repairing, servicing, delivering, testing, road testing, parking, or storing motor vehicles. This means your policy covers liability when a mechanic test-drives a customer’s vehicle and causes an accident, damage to customer cars while they sit on your lot, and injuries that occur during shop operations. Garagekeepers liability, a separate but complementary coverage, protects customer vehicles in your care from theft, weather damage, or accidents that happen while the car is stored or serviced at your facility.

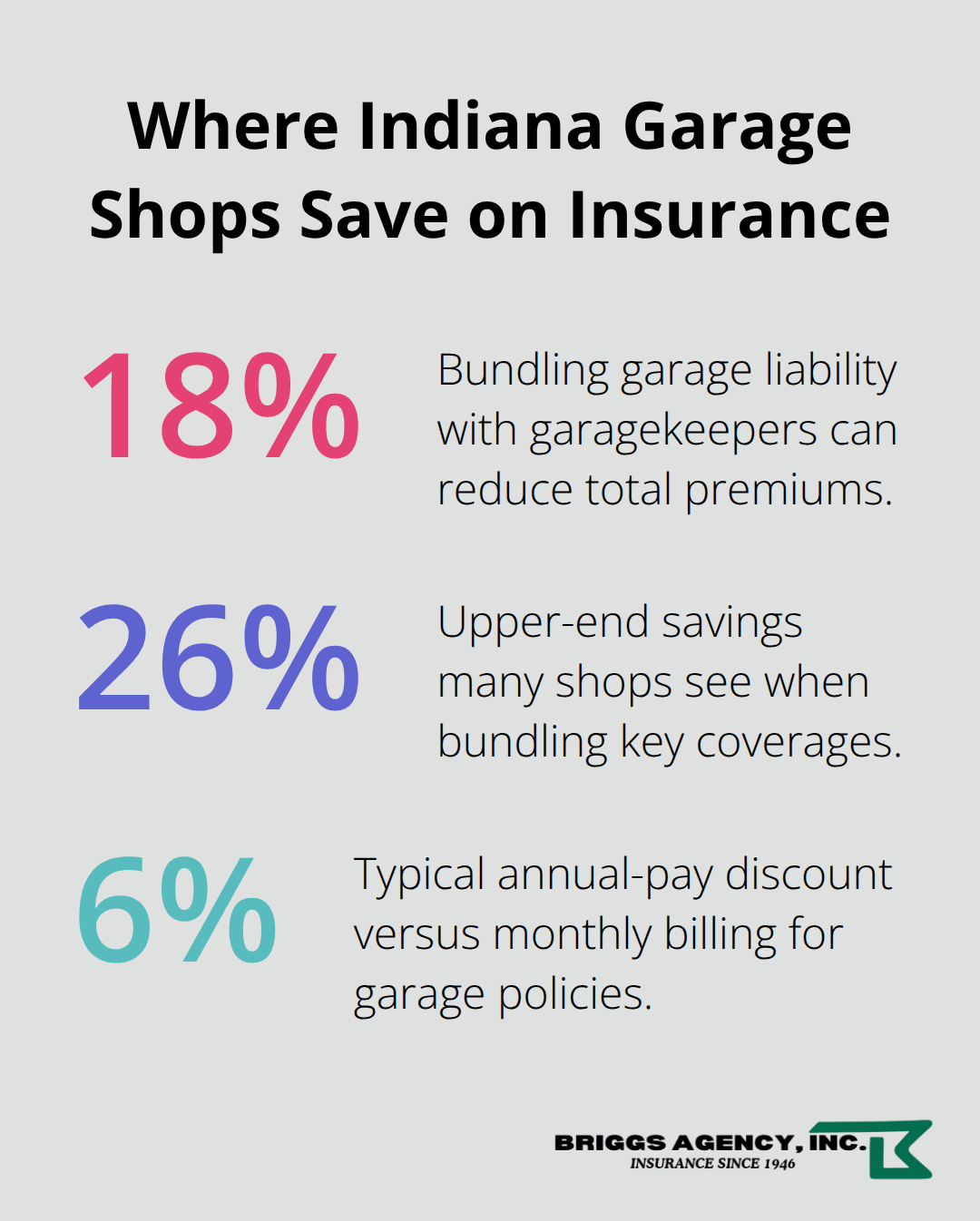

The difference between these two coverages matters significantly. Garage liability responds when your operations cause damage to someone else’s vehicle, while garagekeepers liability covers damage to vehicles your customers leave with you. In Indiana, auto repair shops typically pay around $149 per month for general liability coverage and can bundle garage liability with garagekeepers liability to reduce total premiums by roughly 18% to 26% compared to buying policies separately.

Why Standard Commercial Policies Leave You Exposed

Standard commercial general liability policies have significant gaps for auto service businesses. A typical commercial policy excludes motor vehicle liability because insurers view garage operations as specialized, high-risk work. If a customer’s car is damaged while stored at your shop or if an employee causes an accident during a test drive, your general liability policy will likely deny the claim. This is why Indiana garages cannot rely on off-the-shelf business coverage.

Garage owners policies are tailored specifically to address these scenarios, with limits commonly ranging from $250,000 to $500,000 for garagekeepers coverage depending on your operation size and vehicle types you service. For shops handling high-value vehicles like classic cars or luxury models, higher limits become critical.

Tailoring Coverage to Your Specific Operations

When you evaluate coverage, discuss with your insurance professional how the policy responds to your specific activities-whether you offer delivery service, road testing, collision repair, or paint booth work. Each service line carries different risk levels and may require endorsements or higher coverage limits. The cost varies by location, operation scope, and claims history, but bundling coverages and paying annually instead of monthly typically saves 6% to 9% on premiums.

Understanding what your policy actually covers for each activity you perform protects your business from unexpected claim denials. The next section explores the specific coverage options available and what protection each one provides for your shop’s daily operations.

What Your Garage Policy Actually Covers

Liability Protection for Customer Vehicles

Liability protection for customer vehicles sits at the heart of your garage owners policy, and this is where most shop owners discover how inadequate their previous coverage truly was. When a customer’s car sustains damage while in your care-whether during a test drive, while parked on your lot, or during servicing-garagekeepers liability covers that loss up to your policy limits, typically $250,000 to $500,000 depending on your operation size and the vehicles you handle. This protection applies to theft, weather damage, accidents, and incidents that occur during storage or service work. If you service high-value vehicles like luxury cars or classics, higher limits become essential because a single incident could exceed standard coverage amounts. The cost difference between $250,000 and $500,000 in garagekeepers coverage is modest-often just $20 to $40 monthly-so underinsuring this protection creates unnecessary risk when the premium adjustment is so small.

Protecting Your Tools and Equipment

Tools, equipment, and inventory require separate consideration within your garage policy structure. Your diagnostic equipment, lifts, paint booths, compressors, and shop tools represent significant capital investment, and a standard garage policy may not automatically protect them. Commercial property coverage within a garage owners policy protects these assets against fire, theft, and weather damage while they sit in your facility. Indiana auto repair shops report equipment values ranging from $50,000 to well over $200,000 depending on service offerings, making this protection non-negotiable.

Bundling Coverage for Maximum Savings

When you bundle commercial property with garage liability and garagekeepers coverage, shops typically save 18% to 26% on total premiums compared to purchasing policies separately, which means protecting your equipment becomes more affordable when combined with other coverages. This bundling strategy allows you to maintain robust protection across all critical areas of your operation without stretching your budget.

Workers Compensation and Safety Investment

Workers compensation insurance protects your employees and your business from injury claims, with Indiana rates averaging around $147 monthly for auto repair shops. This coverage becomes legally required once you hire your first employee in Indiana, and the cost is tax-deductible. Shops that invest in ASE certifications and documented safety training often qualify for premium discounts of 5% to 15%, so formalizing your safety practices directly reduces insurance costs while improving your operation’s risk profile.

Your coverage decisions today shape how well your business handles tomorrow’s unexpected incidents. The next section examines the specific gaps that many Indiana garage owners overlook-and how to address them before they become costly problems.

What Coverage Gaps Actually Cost Indiana Garage Owners

Most Indiana shop owners face claim denials only after a loss occurs. The problem isn’t that garage policies lack options-it’s that many shops purchase minimum coverage and skip the endorsements that actually protect daily operations. Uninsured customer vehicles sitting on your lot represent genuine exposure that standard garagekeepers liability often fails to cover completely. If a customer’s vehicle has a lapsed insurance policy and sustains damage while parked at your facility, your garagekeepers coverage applies, but the customer may have no way to recover losses beyond your policy limits. This creates tension because customers expect your facility to protect their cars, yet your coverage caps out at $250,000 to $500,000 depending on your policy. High-value vehicles or multiple cars on your lot simultaneously could exceed these limits in a single incident. Shops handling luxury vehicles, classics, or fleet work frequently underestimate this risk and face situations where a major loss remains partially uncompensated.

Test Drives and Road Service Exposures

Test drives and road service create a different coverage challenge that catches many shop owners off guard. When your mechanic test-drives a customer’s vehicle after repair and causes an accident, garage liability coverage applies-but only if the policy explicitly covers road testing activities. Indiana Code Title 27, § 27-8-9-6 specifically defines road testing as a covered activity, yet many shops fail to confirm this protection exists in their actual policy documents. The distinction matters because some insurers restrict road testing to post-repair verification only, while others exclude it entirely unless an endorsement is added. A mechanic who causes $75,000 in damage to another vehicle during an unauthorized or inadequately covered test drive exposes your shop to direct liability that your policy might not cover.

Hired and Non-Owned Vehicle Liability Gaps

Hired and non-owned vehicle liability gaps emerge when you use rental vehicles for business purposes or when employees operate their personal vehicles for shop-related tasks. Standard garage policies do not automatically cover these scenarios, yet many shops regularly use rental trucks for parts delivery or employee vehicles for customer pick-up services. The cost to add hired and non-owned vehicle coverage typically runs $15 to $30 monthly, yet most shops never request it because they do not recognize the exposure. This gap represents a significant blind spot for shops that depend on vehicle mobility for daily operations.

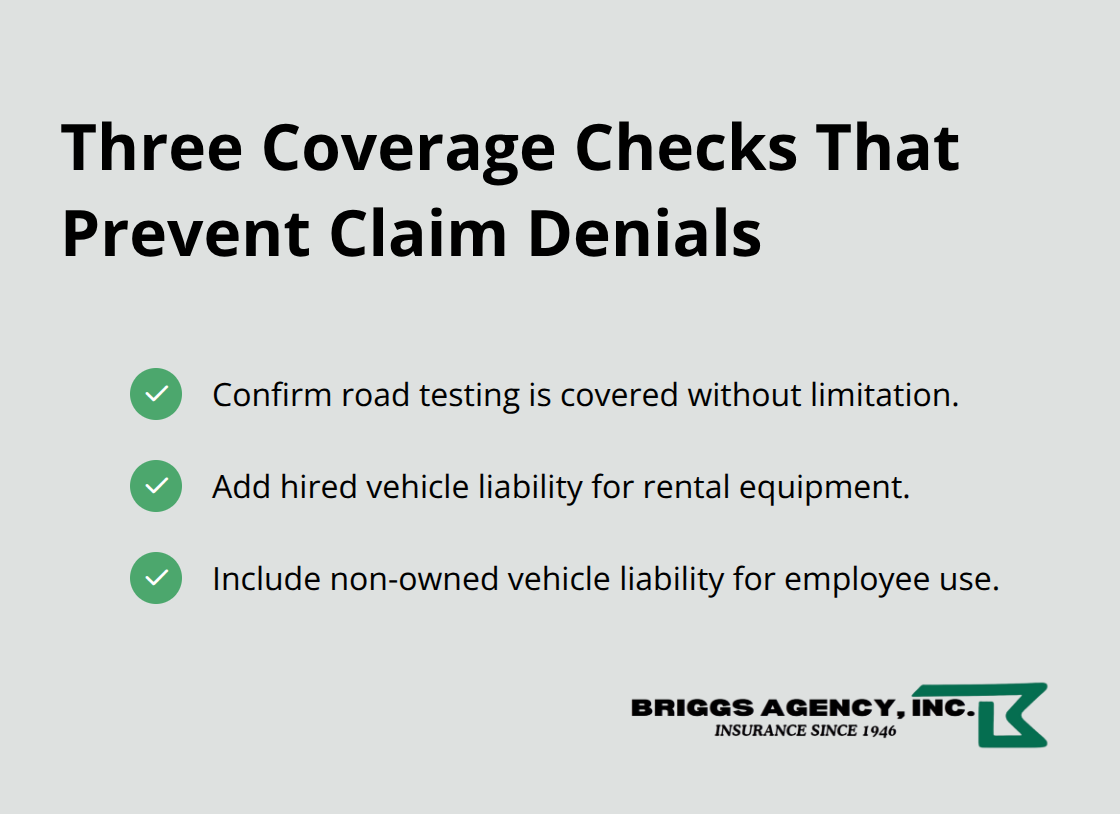

Verification Steps That Prevent Costly Denials

Shops operating in Indiana should verify with their agent whether their current policy covers road testing without limitation, includes hired vehicle liability for rental equipment, and addresses non-owned vehicle use by employees. These three gaps represent the most common reasons claims get denied after incidents occur.

Taking time to confirm coverage specifics before a loss happens protects your operation from unexpected financial exposure and ensures your policy actually matches your business activities.

Final Thoughts

A garage owners policy in Indiana protects your business from the specific risks that standard commercial coverage ignores. Throughout this guide, we’ve shown how liability gaps during test drives, uninsured customer vehicles on your lot, and hired vehicle exposures create financial exposure that catches shop owners unprepared. Bundling garage liability with garagekeepers coverage saves you 18% to 26% on premiums while filling the protection gaps that matter most.

Confirming that road testing, hired vehicles, and non-owned vehicle liability appear explicitly in your policy prevents costly claim denials after incidents occur. Many shop owners discover their existing policies lack critical endorsements or carry limits too low for their operation size. Contact an agent who understands Indiana garage operations and can review your current coverage against your actual business activities.

At Briggs Agency, Inc., we’ve served Crown Point and surrounding Indiana communities since 1946, helping business owners like you compare coverage options from multiple carriers and build policies that match your specific needs. Our independent agency represents top-rated insurers, which means we find competitive pricing without locking you into one company’s limited options. Reach out to us today to discuss your garage owners policy and confirm you’re protected for every activity your shop performs.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.