Restaurant General Liability Insurance: Essentials for Dining Establishments

Running a restaurant means managing countless moving parts, and liability risk is one you can’t afford to overlook. A single slip-and-fall accident or food-related incident can result in costly lawsuits that threaten your business.

Restaurant general liability insurance protects you from these financial disasters. At Briggs Agency, Inc., we help dining establishments understand what coverage they need and how to choose the right limits for their operation.

What General Liability Insurance Actually Covers for Restaurants

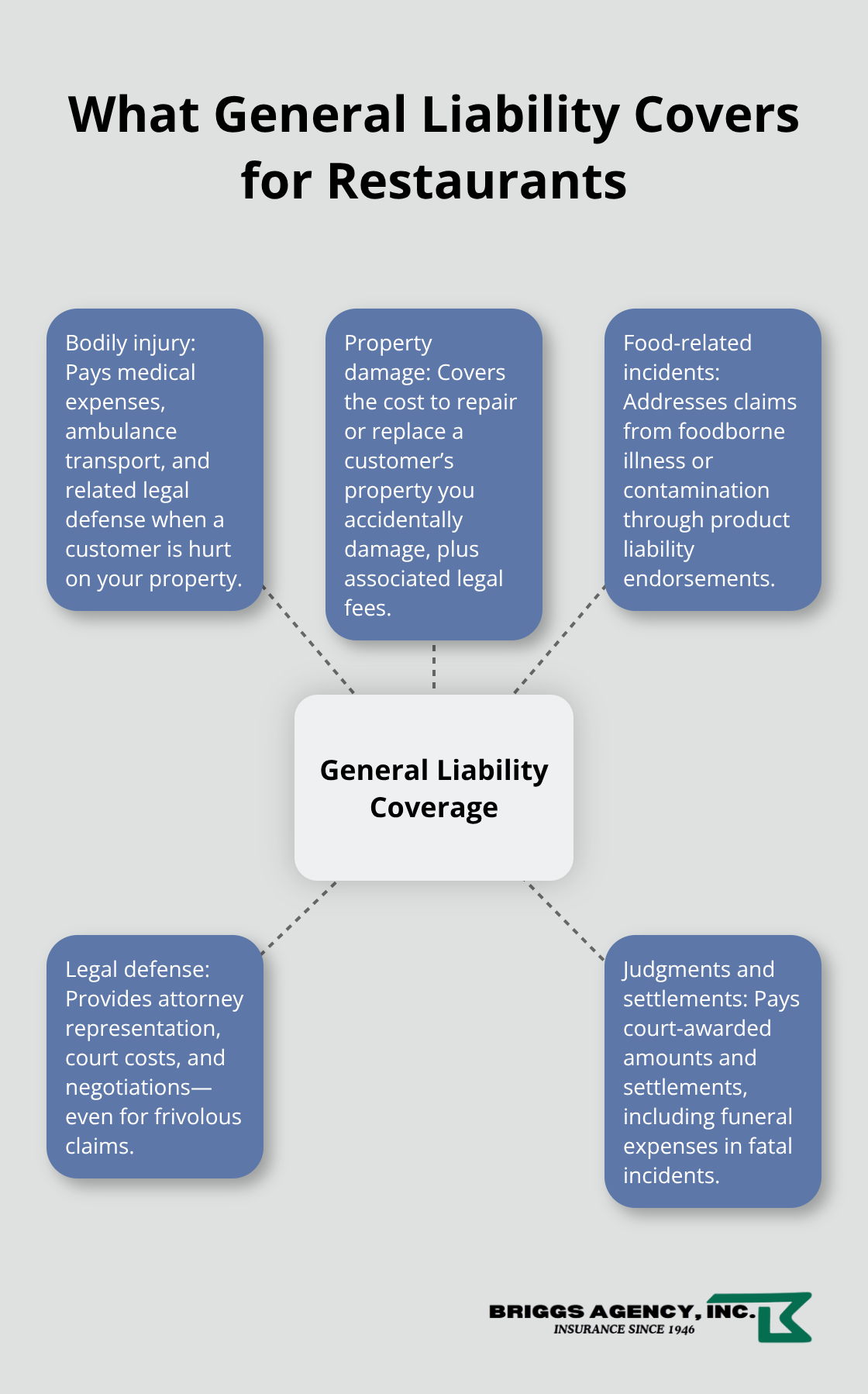

General liability insurance protects your restaurant from the financial fallout of customer injuries and property damage claims that happen on your premises or during your operations. Slip-and-fall accidents are remarkably common in dining establishments and can result in significant liability exposure. When a customer is injured on your property, general liability covers their medical expenses, ambulance transport, and your legal defense fees if they file a lawsuit. The coverage also pays court judgments and settlements, including funeral expenses in fatal incidents. Most restaurants purchase general liability as their first policy because it addresses everyday operational hazards that directly threaten the business.

Average coverage typically ranges from $500,000 to $1,000,000 per occurrence, with average premiums around $73 per month for food and beverage establishments.

Bodily Injury Protection That Matters

When a customer slips on a wet floor or gets injured in your dining area, general liability covers their medical treatment and related legal costs. Your policy pays for hospital visits, emergency care, and ongoing treatment without forcing you to pay out of pocket first. This protection extends to employees and third parties on your property, though workers’ compensation handles on-the-job employee injuries separately. Many policies offer $0 deductibles, meaning you pay nothing before coverage kicks in for a covered claim.

Property Damage and Food-Related Liability

If your restaurant accidentally damages a customer’s property, general liability covers replacement costs and legal fees. The coverage also addresses liability from foodborne illnesses and contaminated food, which typically fall under product liability endorsements within your general liability policy. Your general liability coverage protects you financially when food safety issues result in customer claims, helping you manage the financial impact without depleting your reserves.

Legal Costs That Won’t Drain Your Budget

General liability covers legal defense expenses, including attorney fees, court costs, and settlement negotiations. Your insurer assigns legal representation and handles the defense, meaning you’re not paying these substantial costs yourself. This coverage applies whether the claim is legitimate or frivolous, protecting your business from the financial burden of defending yourself in court.

Understanding what your general liability policy covers is only half the battle. The real question becomes whether your restaurant faces specific risks that standard coverage alone won’t address-and that’s where assessing your operation’s unique exposure becomes essential.

Why Your Restaurant Can’t Skip General Liability Insurance

Restaurants experience structure fires at roughly twice the rate of other commercial buildings, with cooking equipment as the leading cause. Yet fires represent only one category of risk that general liability addresses. The real exposure comes from everyday operations: a customer slips on a wet floor near the bar, orders food contaminated during preparation, or suffers an allergic reaction from undisclosed ingredients. The CDC estimates that foodborne illness sickens about 48 million Americans annually, and one outbreak can force a restaurant to close for weeks while investigations proceed and legal claims accumulate. General liability covers the medical expenses, legal defense, and settlement costs that follow these incidents, preventing a single accident from bankrupting your operation. Without this coverage, you’re personally liable for all costs, which can easily exceed $500,000 for a serious slip-and-fall case or foodborne illness outbreak. Most restaurants carry coverage limits between $500,000 and $1,000,000 per occurrence, with premiums averaging $73 per month-a modest investment compared to the financial devastation of an uninsured claim.

The Food Safety Reality

Food poisoning claims fall under product liability endorsements within your general liability policy, covering contamination incidents that result in customer illness or injury. Health code violations carry fines up to $1,000 per violation in many states and may lead to license suspension or closure if you don’t remedy them promptly. General liability helps cover the legal costs of defending your operation during regulatory investigations. Your policy protects you when customers file claims alleging foodborne illness, regardless of whether your restaurant was actually at fault. This distinction matters because frivolous claims still require legal defense, and those attorney fees alone can reach tens of thousands of dollars before a case settles or goes to trial.

Slip-and-Fall Claims Cost More Than Most Owners Expect

Slip-and-fall accidents represent the most common liability exposure in restaurants due to wet floors, spilled food, and busy service areas. Prevention strategies-rapid spill cleanup, wet floor signs, non-slip mats, and documenting incidents with photos and witnesses-reduce risk significantly, yet accidents still occur despite best efforts. When they do happen, medical costs can exceed $500,000, and customers often pursue legal action to cover treatment, lost wages, and pain and suffering.

General liability covers these expenses without forcing you to deplete operating capital or take out loans. Your insurer handles the legal defense and negotiates settlements, allowing you to focus on running the business rather than managing litigation.

Why Coverage Limits Matter for Your Bottom Line

A single serious injury claim can exhaust inadequate coverage limits, leaving your restaurant responsible for amounts exceeding your policy maximum. Standard limits of $500,000 to $1,000,000 per occurrence protect most small to mid-sized establishments, but your specific operation may warrant higher limits depending on annual revenue, customer volume, and whether you serve alcohol. Choosing the right limit requires honest assessment of your exposure and consultation with someone who understands restaurant operations. The difference between a $500,000 limit and a $1,000,000 limit typically costs only $20–$30 more per month, yet that additional protection can mean the difference between staying open and closing permanently after a major claim.

Understanding what your restaurant faces financially is one thing; selecting the actual coverage that fits your operation is another. The next step involves evaluating your specific risks and comparing what different policies actually offer.

How to Choose the Right Coverage for Your Restaurant

Choosing general liability coverage for your restaurant requires more than picking a number that sounds reasonable. Start by documenting your operation: dining and kitchen square footage, projected annual sales, number of employees, and whether you serve alcohol or offer delivery services. These specifics directly influence your liability exposure and the coverage limits you actually need. A 2,000-square-foot casual dining establishment with 15 employees faces different risks than a 5,000-square-foot steakhouse with 50 staff members. Most restaurants operate with $500,000 to $1,000,000 per occurrence limits, but your lease agreement may impose minimum requirements you must meet. Failing to verify lease requirements creates a dangerous situation: you could face mid-year policy increases or lease violations if your coverage falls short of what your landlord demands.

Coverage Limits That Match Your Operation

Many commercial leases require higher limits-typically $2 million per occurrence and $4 million aggregate-so review your lease before settling on limits. The premium difference between $500,000 and $1,000,000 coverage typically runs $20–$30 monthly, making the upgrade inexpensive insurance against catastrophic exposure. Your specific operation determines whether standard limits suffice or whether higher coverage makes sense for your financial protection. A restaurant with high customer volume and alcohol service warrants stronger limits than a small café with minimal foot traffic.

Understanding Deductibles and Real-World Costs

Deductibles represent what you pay before your insurance covers a claim, and this choice directly impacts both your monthly premium and your financial risk. Many restaurants purchase policies with $0 deductibles, meaning coverage activates immediately when a claim occurs. A $0 deductible policy costs more monthly than a $1,000 or $2,500 deductible option, but eliminates the risk of scraping together cash during a crisis. For restaurants operating on thin margins, a $0 deductible makes financial sense because you avoid unexpected out-of-pocket expenses when slip-and-fall accidents or food-related claims emerge.

If you choose a higher deductible to reduce premiums, maintain enough cash reserves to cover that amount without disrupting operations. A single serious injury claim could cost $500,000 or more in medical expenses and legal fees; your deductible determines how much of that you personally absorb before coverage kicks in. The decision between deductibles ultimately depends on your financial position and risk tolerance, not on what sounds cheapest at first glance.

Working with Agents Who Understand Restaurant Operations

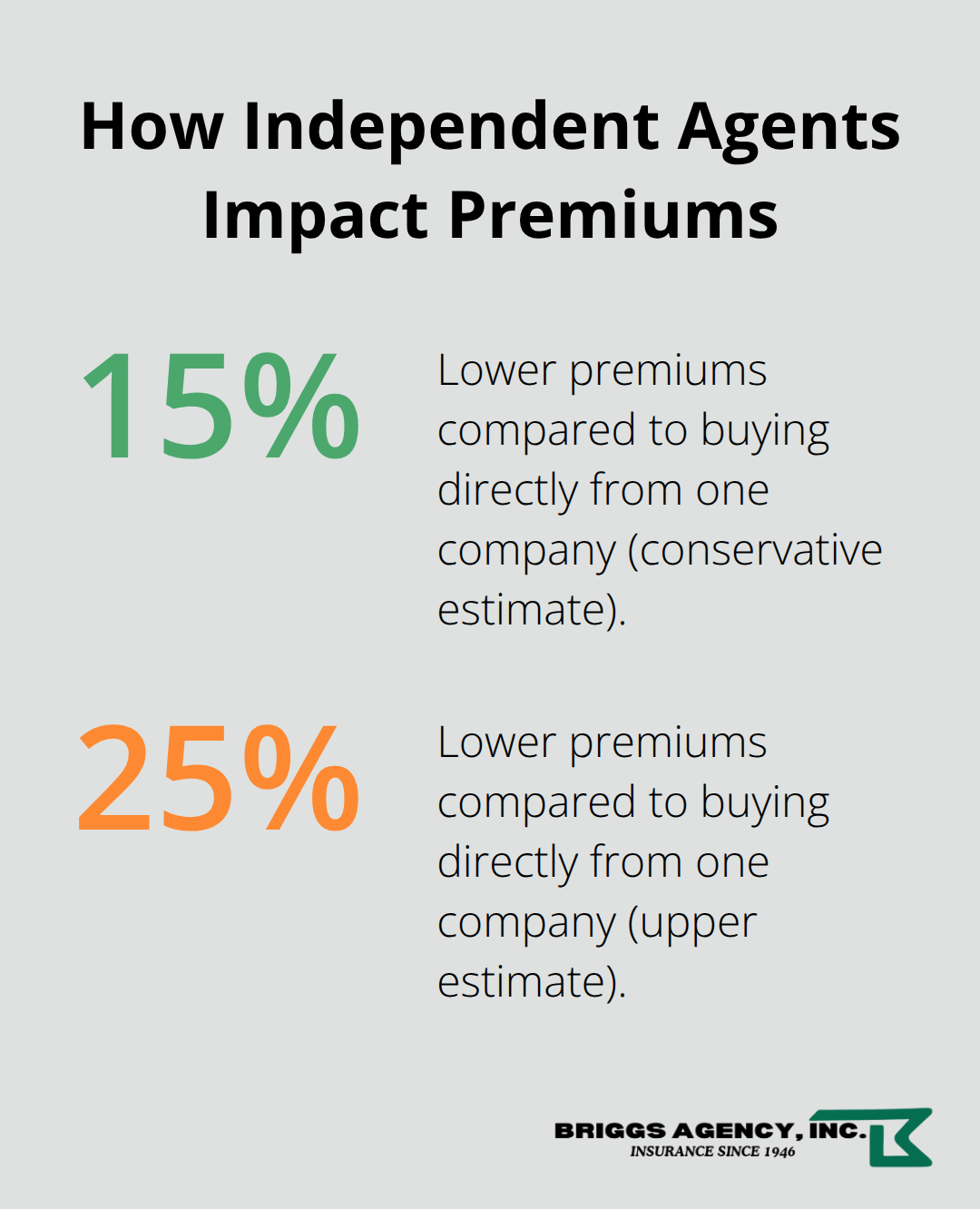

Independent agents who understand restaurant operations make the difference between generic coverage and protection tailored to your actual risks. Independent agents represent multiple insurance carriers, meaning they can shop your quote across different companies rather than steering you toward a single insurer. This access to multiple carriers typically results in 15–25% lower premiums compared to buying directly from one company.

An agent familiar with restaurants knows which endorsements matter for your specific menu and service model. If you serve alcohol, your agent identifies liquor liability gaps that general liability alone won’t address. If you operate delivery or catering, the agent verifies you have hired and non-owned auto coverage for vehicles transporting food. If you’ve recently upgraded kitchen equipment, the agent confirms your property limits reflect current replacement value rather than outdated figures. Your agent should ask detailed questions about your staffing, menu offerings, facility layout, and equipment rather than simply quoting a standard package. Agents who take time to understand your operation catch exposures you might miss entirely, potentially saving you from devastating underinsurance.

Final Thoughts

Restaurant general liability insurance forms the foundation of financial protection for any dining establishment, yet purchasing a policy marks only the start of your protection strategy. Review your coverage annually with your agent to confirm limits still match your lease requirements, equipment value, and customer volume-especially after you expand your dining area, add staff, or begin serving alcohol. Risk management practices reduce claims and lower insurance costs over time, so implement rapid spill cleanup protocols, maintain non-slip flooring in high-traffic areas, and train staff on food safety procedures that prevent contamination incidents.

Document all accidents with photos and witness statements, even minor ones, because this information proves invaluable if claims emerge later. Regular maintenance of kitchen equipment and dining areas prevents equipment failures and injuries that could otherwise trigger expensive claims. These proactive steps work alongside your restaurant general liability insurance to protect both your employees and your bottom line.

We at Briggs Agency, Inc. understand the specific risks restaurants face in our community. As an independent agency representing multiple carriers, we compare options across different insurers to find competitive pricing and coverage tailored to your operation. Contact us today to discuss your restaurant’s coverage needs and receive a personalized quote that reflects your actual exposure rather than generic industry assumptions.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.