Restaurant Property Damage Insurance: Safeguarding Your Dining Spot

Your restaurant faces real risks every day-from kitchen fires to burst pipes to severe weather. These incidents can shut down operations, destroy equipment, and threaten your business’s survival.

Restaurant property damage insurance protects your building, equipment, and inventory when disaster strikes. At Briggs Agency, Inc., we help restaurant owners understand what coverage actually means for their specific situation and assets.

Common Causes of Property Damage in Restaurants

Kitchen Fires: Prevention Stops Catastrophe

Kitchen fires rank as the leading threat to restaurant operations, and proper maintenance prevents most of them. The National Fire Protection Association reports that unattended cooking causes the primary incidents, while grease buildup in hoods and ducts creates a secondary risk that compounds rapidly. A single grease fire spreads to your ventilation system in minutes, forcing complete shutdown and potentially destroying thousands of dollars in equipment. Regular hood cleaning following NFPA 96 standards isn’t optional-it’s the difference between a minor incident and catastrophic loss. Many restaurant owners skip this maintenance to save money, then face six-figure property damage claims and weeks of closure.

Your suppression system requires annual inspection and certification; a failed system during a fire means your property damage claim faces denial if negligence is found.

Water Damage: Pipes, Flooding, and Hidden Costs

Burst pipes and flooding create hidden costs that most restaurant owners underestimate. A single burst water line in your building structure destroys drywall, flooring, and electrical systems before you notice it, especially in older establishments with aging infrastructure. Flooding from heavy rain or sewer backups poses an even greater threat-standard property policies often exclude water damage from external sources, leaving you exposed. Temperature control failures in refrigeration units cause inventory spoilage that wipes out thousands of dollars in perishable food within hours, yet many policies require separate spoilage coverage or endorsements to cover this loss.

Weather and Seasonal Threats

Weather-related damage follows predictable seasonal patterns in your region and demands specific coverage. Wind tears off roofs, hail destroys HVAC units, and power outages trigger equipment breakdown that spoils inventory and halts operations. Northern Indiana restaurants face particular risk from severe winter storms that damage roofs and burst pipes simultaneously, yet many owners treat weather coverage as optional. Standard property policies contain gaps that cost money when disaster strikes. Your coverage limits must reflect your actual replacement costs, not what you think you might spend. Understanding what your policy actually covers-and what it excludes-determines whether you recover fully or face unexpected out-of-pocket expenses when property damage occurs.

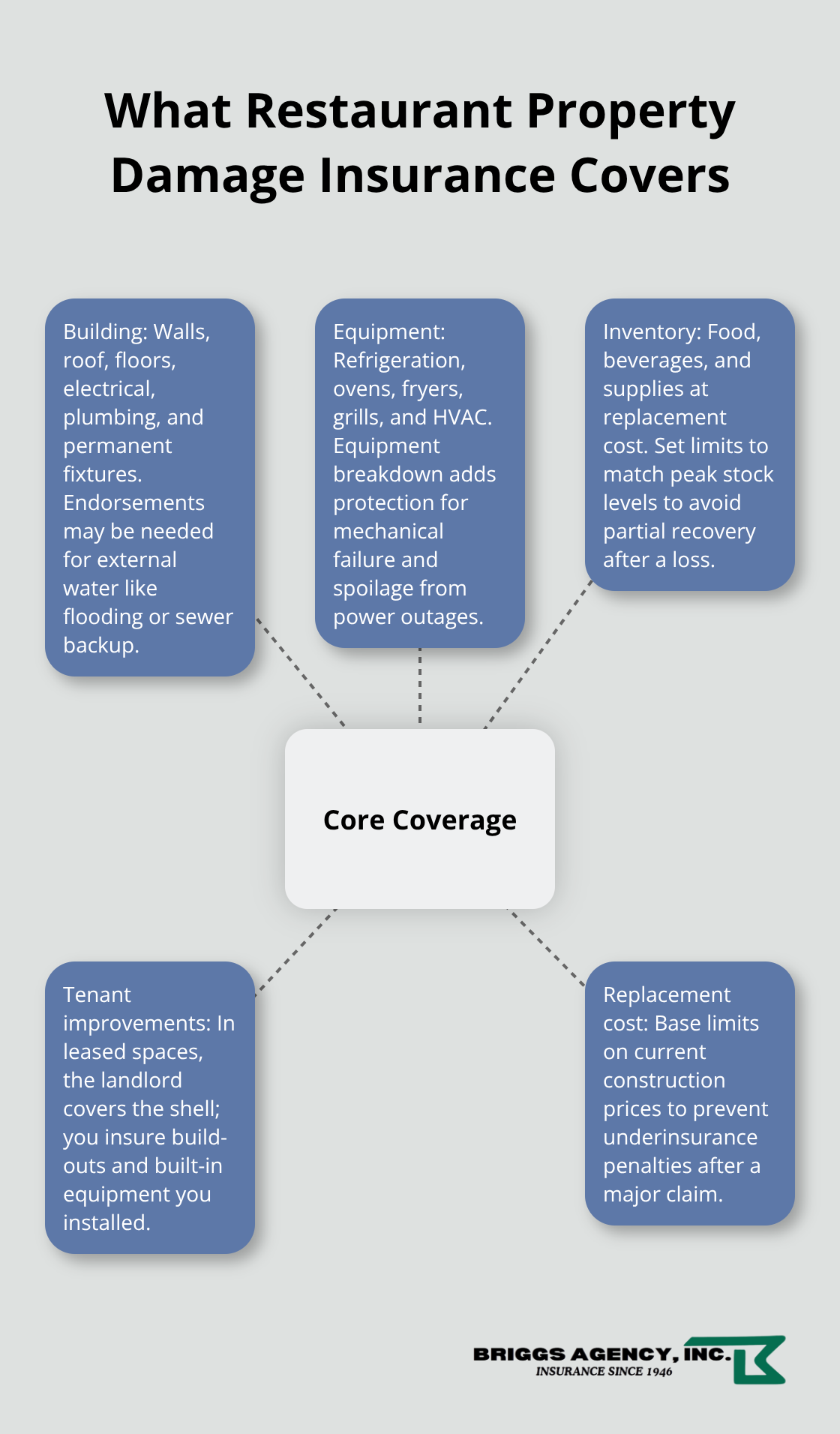

What Restaurant Property Damage Insurance Covers

Restaurant property damage insurance protects three critical areas of your operation, but understanding exactly what falls under each category prevents costly coverage gaps when you file a claim.

Building Structure and Permanent Fixtures

Your building structure includes the walls, roof, flooring, electrical systems, plumbing, and permanent fixtures like built-in counters or walk-in coolers that you cannot remove without structural damage. Most policies cover damage from fire, wind, hail, theft, and vandalism to these components, though water damage from external sources like flooding or sewer backup often requires separate endorsements.

If you occupy a leased space, your landlord’s policy covers the building shell, but you need your own coverage for tenant improvements and built-in equipment you installed. Your replacement cost should reflect current construction prices in your area, not what you originally paid five or ten years ago. Underinsuring your building means you absorb the difference when reconstruction costs exceed your policy limit, a painful reality many owners face after major damage.

Equipment and Appliances

Equipment and appliances demand separate attention because standard property coverage sometimes limits what it pays for commercial kitchen gear. Your refrigeration units, ovens, fryers, grills, and HVAC systems need explicit coverage with limits matching their replacement value. Equipment breakdown coverage protects against mechanical failure and spoilage from power outages, which standard property policies exclude entirely. A commercial refrigerator costs between $3,000 and $8,000 to replace, and spoilage from a single cooling failure destroys $5,000 to $15,000 in perishable inventory within hours. Your policy should specify coverage for both stored equipment and units actively operating during service hours.

Inventory and Stock

Inventory and stock coverage protects food, beverages, and supplies at their replacement cost, not what you paid wholesale. Many restaurant owners carry inventory limits far below their actual stock value, then face partial recovery when fire or water destroys their supplies. Your policy covers inventory both in storage areas and actively on hand during service hours, provided your limits match your actual stock levels.

How Location Shapes Your Coverage and Costs

Location matters significantly for your coverage costs and available options. Urban restaurants with higher property values and greater foot traffic face higher premiums than rural establishments, while areas prone to severe weather or flooding see rate increases of 15 to 25 percent depending on historical loss data. Northern Indiana restaurants face particular exposure to winter storms and seasonal flooding that demand specific endorsements beyond standard policies. Your actual replacement costs for building components, equipment, and inventory determine whether your policy limits provide adequate protection or leave you exposed. Calculating these numbers accurately before disaster strikes separates full recovery from unexpected out-of-pocket expenses.

How to Choose the Right Coverage for Your Restaurant

Assess Your Property Value and Assets

Start with a detailed inventory of everything your restaurant owns, because guessing at property values guarantees underinsurance. Walk through your building with a calculator and list every item: the cost to replace your roof, HVAC system, flooring, walk-in coolers, POS terminals, furniture, and smallwares. Contact three local contractors and obtain actual quotes for roof replacement, not estimates from five years ago. A 2,000-square-foot restaurant building in Northern Indiana costs between $150 and $250 per square foot to rebuild after total loss, meaning your structure alone requires $300,000 to $500,000 in coverage.

Equipment replacement costs vary dramatically. A commercial six-burner range runs $4,000 to $7,000, a walk-in cooler costs $8,000 to $15,000, and a complete hood system with suppression reaches $12,000 to $25,000. Your inventory value fluctuates seasonally, but calculate your peak stock level and use that figure for your insurance limit. Most restaurant owners underestimate their inventory by 30 to 40 percent because they forget about beverages, dry goods in storage, and prepared food in coolers.

Document everything with photos and receipts, then add 10 to 15 percent to your calculations to account for inflation and the reality that replacement costs exceed original purchase prices. Many restaurants carry limits 20 to 30 percent below their actual replacement costs, a mistake that costs thousands when disaster strikes.

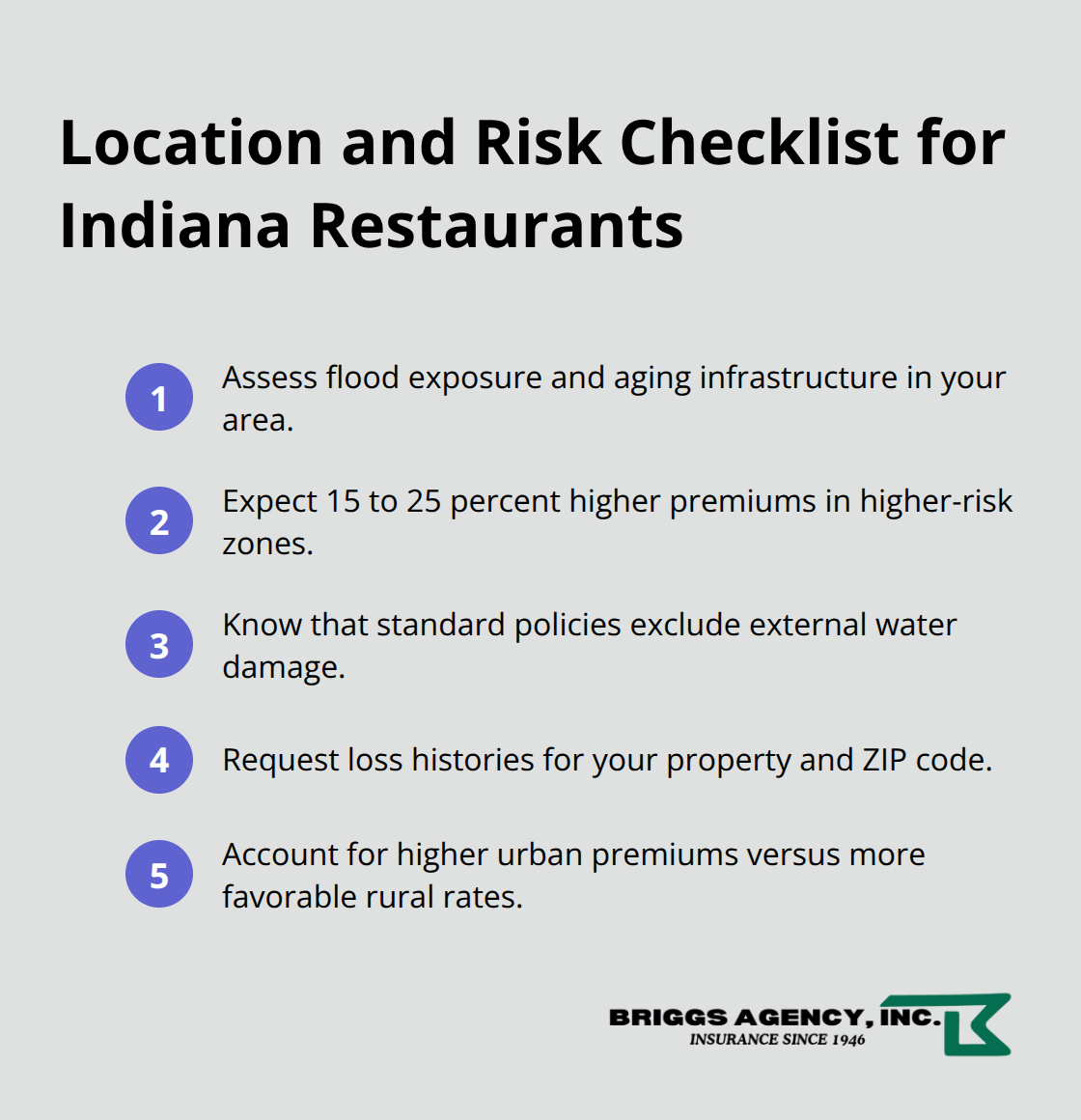

Evaluate Your Location and Risk Factors

Your location directly determines both your coverage needs and your costs, making regional risk assessment non-negotiable. Properties in flood-prone areas or communities with aging infrastructure face 15 to 25 percent higher premiums for property coverage, and standard policies exclude water damage from external sources entirely.

Northern Indiana restaurants need specific endorsements for sewer backup coverage, off-premises power outage spoilage protection, and winter storm damage that standard policies limit or exclude. Ask your insurance agent for your specific property’s loss history and the historical frequency of claims in your ZIP code for fire, water, wind, and weather events. Restaurants in high-traffic urban areas pay more for property coverage due to higher replacement costs and increased exposure, while those in lower-density areas typically see more favorable rates.

Review Policy Limits and Deductibles

Your deductible choice directly impacts your premium and your out-of-pocket exposure. A $1,000 deductible costs significantly less than a $500 deductible, but you absorb that $1,000 in losses when claims occur. Try a deductible you can afford to pay without straining your cash flow, because underfunding this decision forces you to skip claims on smaller losses.

Review your replacement cost calculations annually and adjust your limits whenever you renovate, purchase new equipment, or expand your operation. Coverage that protected you adequately last year may leave you exposed today. Your insurance agent can help you identify gaps in your current policy and recommend endorsements that match your specific operation and location.

Final Thoughts

Restaurant property damage insurance protects your building, equipment, and inventory from the real threats that force closure and drain your finances. Walk through your restaurant, document what you own, obtain current quotes from local contractors, and calculate your peak inventory value-this work takes a few hours but prevents the painful discovery after a fire or flood that your coverage falls $50,000 or $100,000 short of what you need to rebuild. Your location in Northern Indiana shapes both your risks and your coverage needs, with winter storms, seasonal flooding, and aging infrastructure demanding specific endorsements that standard policies exclude.

Review your policy annually, especially after renovations or equipment purchases, because coverage that worked last year may leave gaps today. Choose a deductible you can actually afford to pay without straining cash flow, and verify that your limits match current replacement costs, not what you paid five years ago. Your restaurant deserves protection from someone who understands local risks and your business.

We at Briggs Agency, Inc. have served Northern Indiana restaurants and businesses since 1946, helping owners understand what protection actually means for their specific operation. As an independent agency representing multiple top-rated carriers, we compare options and tailor restaurant property damage insurance to deliver competitive pricing and the right coverage for your situation. Contact Briggs Agency, Inc. to review your current coverage, identify gaps, and build a property damage insurance program that matches your actual needs.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.