Running a garage in Indiana means managing significant risks every single day. Your customers’ vehicles, your equipment, and your business itself all need protection that standard policies simply don’t cover.

Commercial garage insurance in Indiana is specifically designed to handle the unique exposures your operation faces. At Briggs Agency, Inc., we help garage owners understand exactly what coverage they need and why it matters for their bottom line.

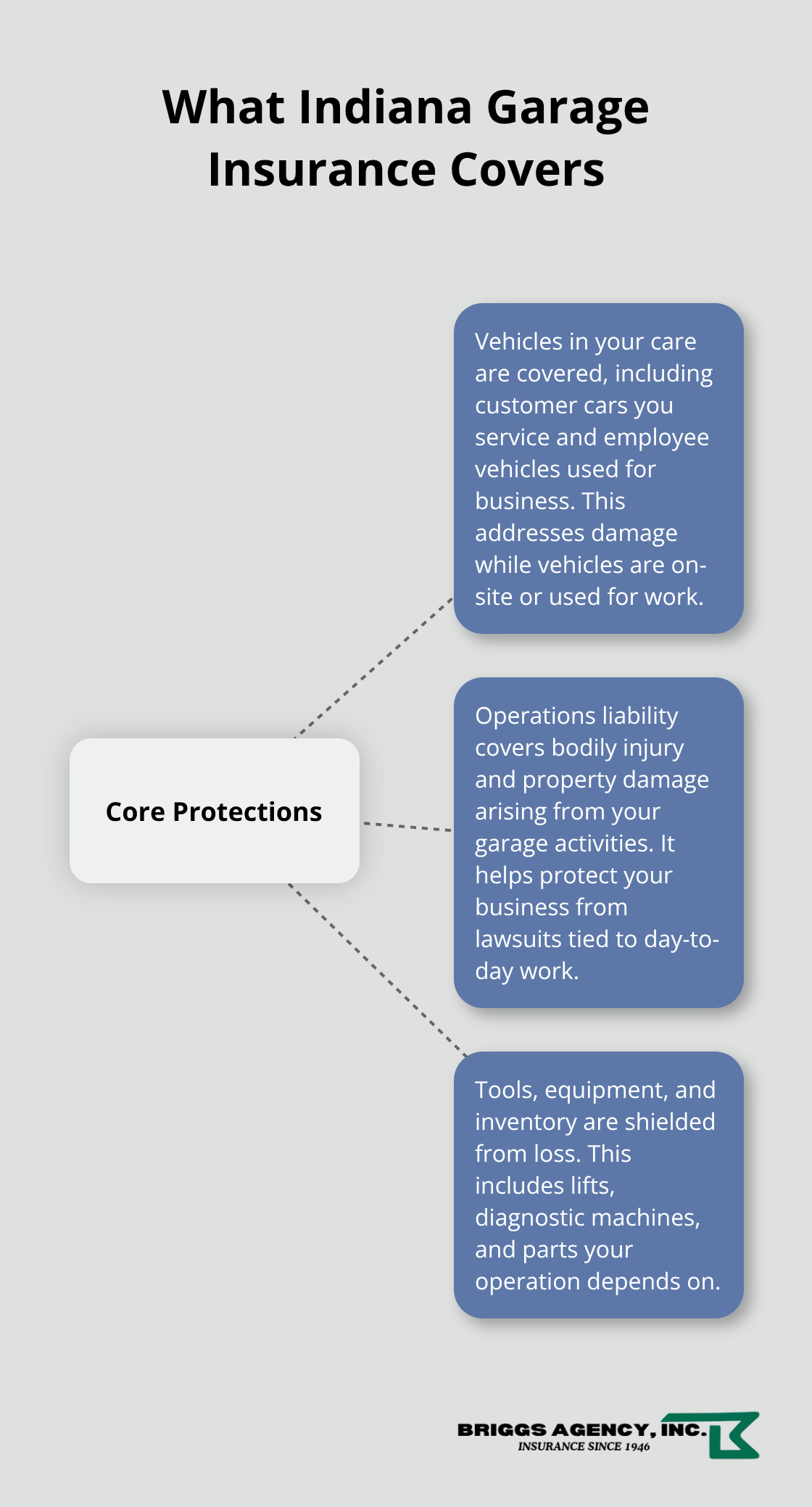

What Your Garage Insurance Actually Covers

Vehicle Coverage for Customers and Employees

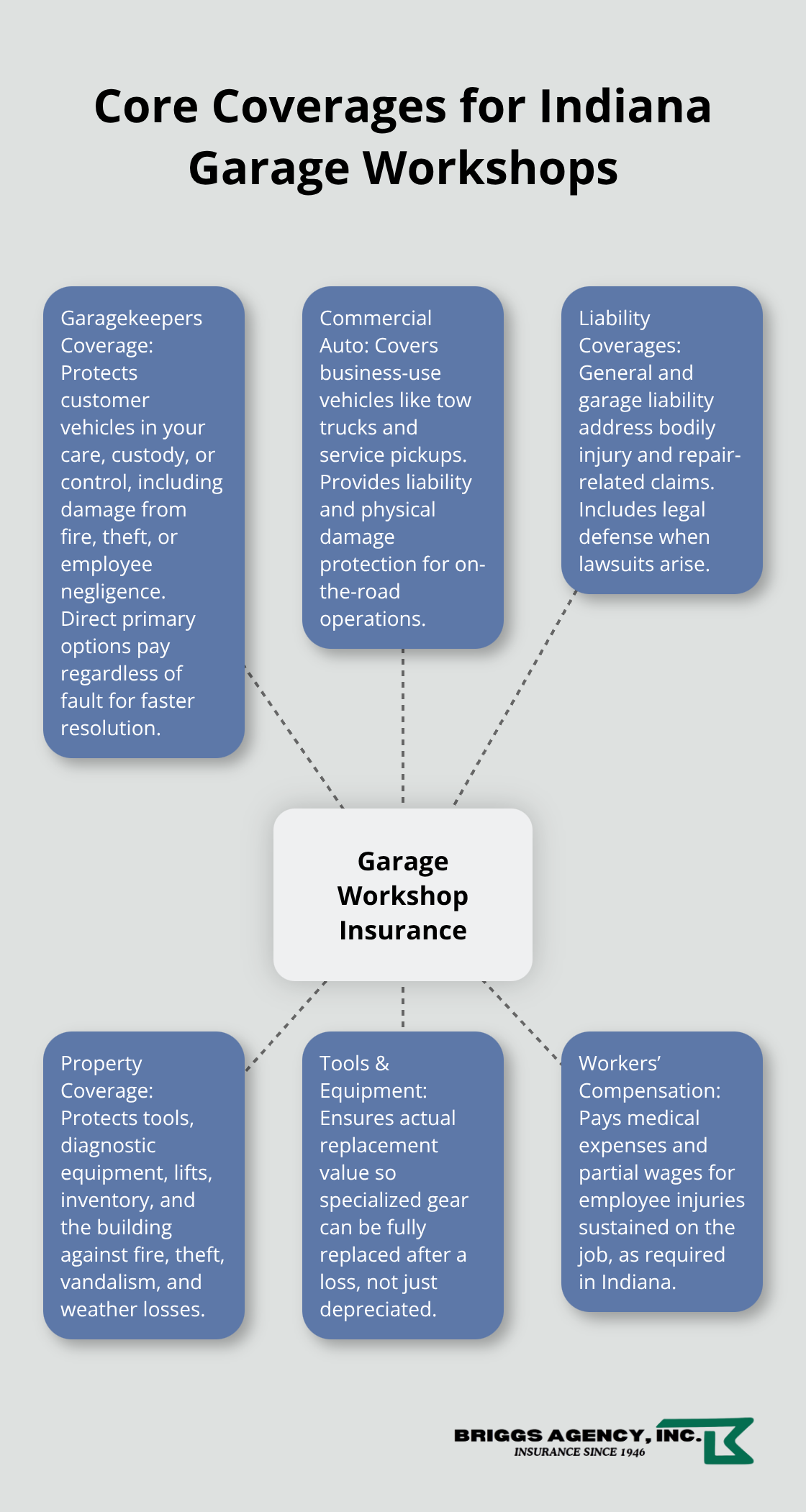

Commercial garage insurance in Indiana protects three critical areas of your operation that standard business policies leave exposed. First, it covers vehicles in your care-both customer cars you service and employee vehicles used for business. Second, it protects your liability when someone gets hurt or property gets damaged as a result of your garage operations. Third, it shields your tools, equipment, and inventory from loss.

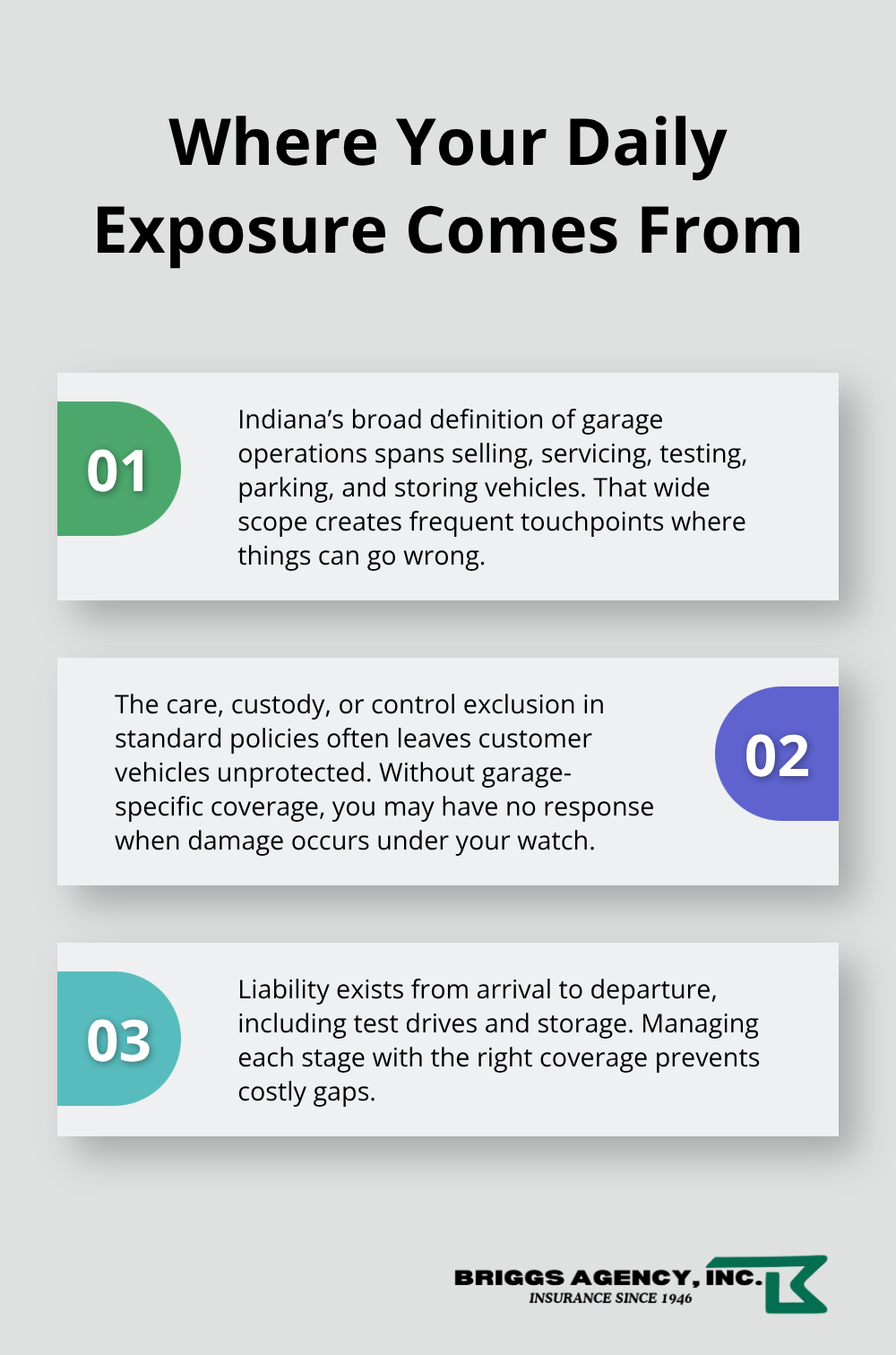

Indiana Code Title 27 defines garage liability to include selling, leasing, repairing, servicing, delivering, testing, road testing, parking, or storing motor vehicles. This broad scope means your coverage should extend from the moment a customer’s car pulls into your lot through test drives and storage until it leaves. The care, custody, or control exclusion found in standard policies creates a major gap-it excludes damage to customer vehicles left with you for repair or storage.

Closing the Garagekeepers Coverage Gap

Garagekeepers liability specifically covers a customer’s vehicle damaged while it sits on your premises, whether from weather, theft, vandalism, or accidents during storage. You have three garagekeepers options: Legal Liability covers damage only when you’re negligent, Direct Primary covers losses regardless of fault (including weather and theft), and Direct Excess provides the broadest protection by paying regardless of liability and only in excess of other insurance.

For most Indiana shops, Legal Liability is the standard choice, but if you store vehicles regularly or operate in high-risk areas, Direct Primary deserves serious consideration. Your liability coverage addresses what happens when a mechanic test-drives a customer’s vehicle and causes an accident or when a customer gets injured on your property. Garage liability covers bodily injury and property damage claims from these situations, protecting your business from lawsuits that could otherwise devastate operations.

Equipment, Tools, and Inventory Protection

Commercial auto coverage protects vehicles you own or operate-tow trucks, service vehicles, and pickup trucks used for business purposes. Tools, equipment, and inventory protection covers everything from diagnostic machines and lifts to spare parts and supplies stored on-site. This coverage responds to theft, fire, vandalism, and other perils that could shut down your operation.

Indiana garages should map their actual operations against policy language to confirm coverage for road testing, vehicle storage, and delivery activities. Ask your insurer specifically whether overnight vehicle storage, test drives on public roads, and equipment stored in work bays are covered under the policy you’re considering.

Aligning Your Operations with Your Policy

Misalignment between what you do daily and what your policy covers is where problems emerge. The broad language in garage operations definitions can be interpreted differently by insurers, so confirmation matters. Your specific business model-whether you focus on repairs, sales, storage, or a combination-determines which coverages you actually need and how much protection each one should provide.

Why Indiana Garage Owners Can’t Skip This Coverage

The Real Financial Exposure You Face

Indiana garage owners face real financial exposure that most don’t fully appreciate until something goes wrong. Indiana Code Title 27 explicitly recognizes garage liability as a distinct coverage category because standard commercial policies leave dangerous gaps. When a customer’s vehicle sits damaged in your lot overnight or a mechanic causes an accident during a test drive, your basic liability policy won’t respond. A single incident involving a customer’s vehicle can trigger lawsuits that exceed $50,000 in damages, and without proper garagekeepers coverage, you absorb the full amount personally.

Multiple Exposure Points Throughout Your Day

Indiana’s broad definition of garage operations-which includes selling, leasing, repairing, servicing, delivering, testing, road testing, parking, and storing vehicles-creates multiple exposure points throughout your day. The care, custody, or control exclusion means that standard policies specifically exclude the very situations garage owners face most frequently. Your operation exposes you to liability at every stage, from the moment a customer’s car arrives through test drives and storage until it leaves your premises.

How Coverage Gaps Damage Your Reputation

Your business reputation depends on how you handle customer vehicles and property. A single incident where a customer’s car suffers damage under your watch spreads quickly through local networks, costing you far more in lost business than the actual insurance claim would have covered. Direct Primary garagekeepers coverage removes the negligence requirement entirely, protecting you from weather events, theft, and storage incidents regardless of fault-this matters enormously in Indiana’s climate where hail and winter storms damage vehicles regularly.

Location-Specific Risks in Indiana

If you operate in areas like Evansville, Jasper, or Henderson, vehicle storage during service represents a standard practice that requires explicit coverage confirmation with your carrier. Working with a local broker who understands Indiana’s specific requirements helps you avoid the common mistake of assuming your current policy covers situations it explicitly doesn’t. The right policy protects not just your vehicles and equipment but the trust your customers place in your operation.

Understanding what your current coverage actually includes-and what it excludes-is the first step toward protecting your business. The next section walks you through how to assess your specific risks and choose the right commercial garage insurance for your operation.

How to Choose the Right Commercial Garage Insurance

Start by mapping exactly what happens at your garage each day. Do you test-drive vehicles after service? Store customer cars overnight? Operate tow trucks for deliveries? Sell or lease vehicles? Each activity creates specific insurance needs that differ from your neighbors’ operations. An Indiana body shop focusing on collision work faces different exposures than a transmission specialist or a used car dealership. List your actual business activities and the vehicles involved before comparing carriers or requesting quotes. This inventory becomes your foundation for evaluating whether a policy truly covers your operation.

Confirm Coverage for Your Specific Activities

The care, custody, or control exclusion in standard policies means you cannot assume coverage exists just because your current insurer wrote your general liability policy. Contact your existing carrier and ask them to confirm in writing whether your policy covers vehicle test drives on public roads, overnight vehicle storage on your premises, and delivery of vehicles to customers. Most garage owners discover gaps only after a claim gets denied, so push for specific answers about your exact business model. Indiana Code Title 27 recognizes garage operations as distinct because the exposures are real and substantial.

When comparing policies from different carriers, request sample policy language showing how garagekeepers coverage applies to your situation. Progressive Commercial and other major carriers offer online quotes where you can enter your ZIP code and describe your operations, generating location-specific options within minutes. The quote process itself clarifies what coverage types exist and helps you understand pricing differences between Legal Liability, Direct Primary, and Direct Excess garagekeepers options.

Evaluate Cost Against Your Risk Profile

Insurance cost varies significantly based on your claims history, the types of vehicles you handle, and your coverage selections. If you store high-value vehicles or operate in areas prone to weather damage, Direct Primary garagekeepers coverage costs more upfront but eliminates the negligence requirement, meaning weather or theft losses get paid regardless of fault. For shops storing primarily customer vehicles awaiting routine service, Legal Liability garagekeepers coverage typically provides adequate protection at lower cost.

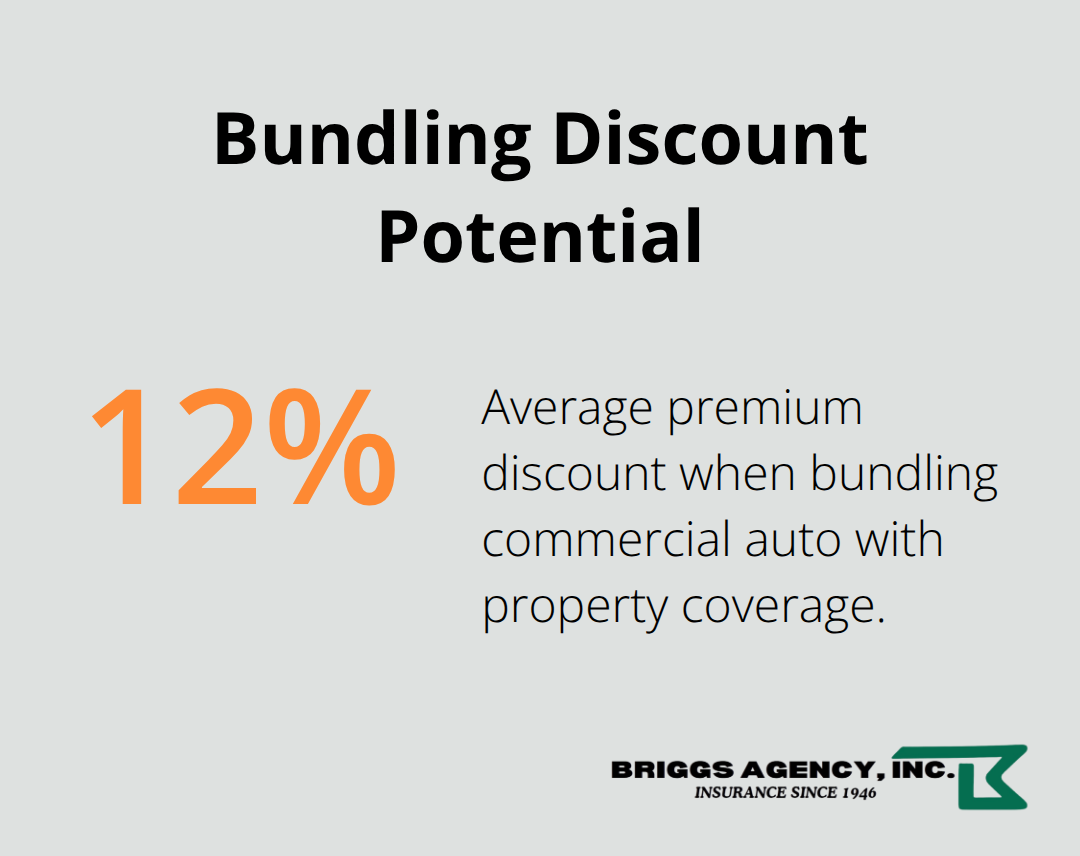

Bundling commercial auto coverage with property protection yields average discounts around 12 percent, so request a bundled quote to reduce your overall premium. Request quotes from multiple carriers rather than accepting the first proposal, especially if your current agent represents only one company. This approach reveals actual differences in how insurers price your specific operation and what each carrier includes in their standard garage policies.

Partner with a Local Agent Who Understands Indiana Garage Operations

An agent familiar with Indiana garage operations understands the specific language in Indiana Code Title 27 and how different insurers interpret broad definitions like garage operations. Briggs Agency, Inc., a family-owned independent agency in Crown Point serving the community since 1946, represents multiple top-rated carriers, which means our experienced local agents can compare options and show you actual differences in coverage and pricing rather than presenting a single solution. Local agents throughout Indiana know the regional risks affecting garages, from winter weather damage to theft patterns in specific communities.

Ask any potential agent whether they can explain in plain language exactly what your policy covers and what it excludes, using your specific business activities as examples. An agent who hesitates or relies on vague language like “everything should be covered” is not the right fit. Confirm that your agent will review your insurance premium payments annually as your business changes, because adding new services or equipment can create coverage gaps in your existing policy.

Final Thoughts

Commercial garage insurance in Indiana protects your operation from exposures that standard policies explicitly exclude. The care, custody, or control exclusion creates real gaps, and a single incident involving a customer’s vehicle, employee injury, or equipment loss can cost tens of thousands of dollars and damage your reputation in the community. The right policy structure-combining garage liability, garagekeepers coverage, and commercial auto protection-addresses these exposures directly and keeps your business operational when problems occur.

Start by listing your actual business activities and contact your current insurer to confirm in writing what your existing policy covers and excludes. Ask specifically about test drives, vehicle storage, and equipment protection, and if your carrier hesitates or provides vague answers, that signals a need to seek quotes from other carriers. Request proposals from multiple companies rather than accepting the first option, and compare how each insurer prices your specific operation (the 12 percent average discount available through bundling commercial auto with property coverage makes this comparison financially worthwhile).

We at Briggs Agency, Inc. understand Indiana garage operations because we’ve served Crown Point and the surrounding community since 1946. As an independent agency representing multiple top-rated carriers, our experienced local agents compare actual coverage options and pricing rather than presenting a single solution. Contact Briggs Agency, Inc. today to discuss your commercial garage insurance needs and receive a customized quote that reflects your actual exposures.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.