Indiana Contractor Liability Insurance: Risks, Rules, and Remedies

Running a contracting business in Indiana means facing real liability exposure every single day. Property damage claims, job site injuries, and third-party lawsuits can drain your finances fast-which is why Indiana contractor liability insurance isn’t optional, it’s essential.

At Briggs Agency, Inc., we’ve helped countless contractors understand their coverage gaps and build protection strategies that actually work. This guide walks you through the risks you face, what Indiana requires, and how to choose coverage that fits your operation.

What Liability Risks Hit Indiana Contractors Hardest

Property Damage Claims Cost More Than You Think

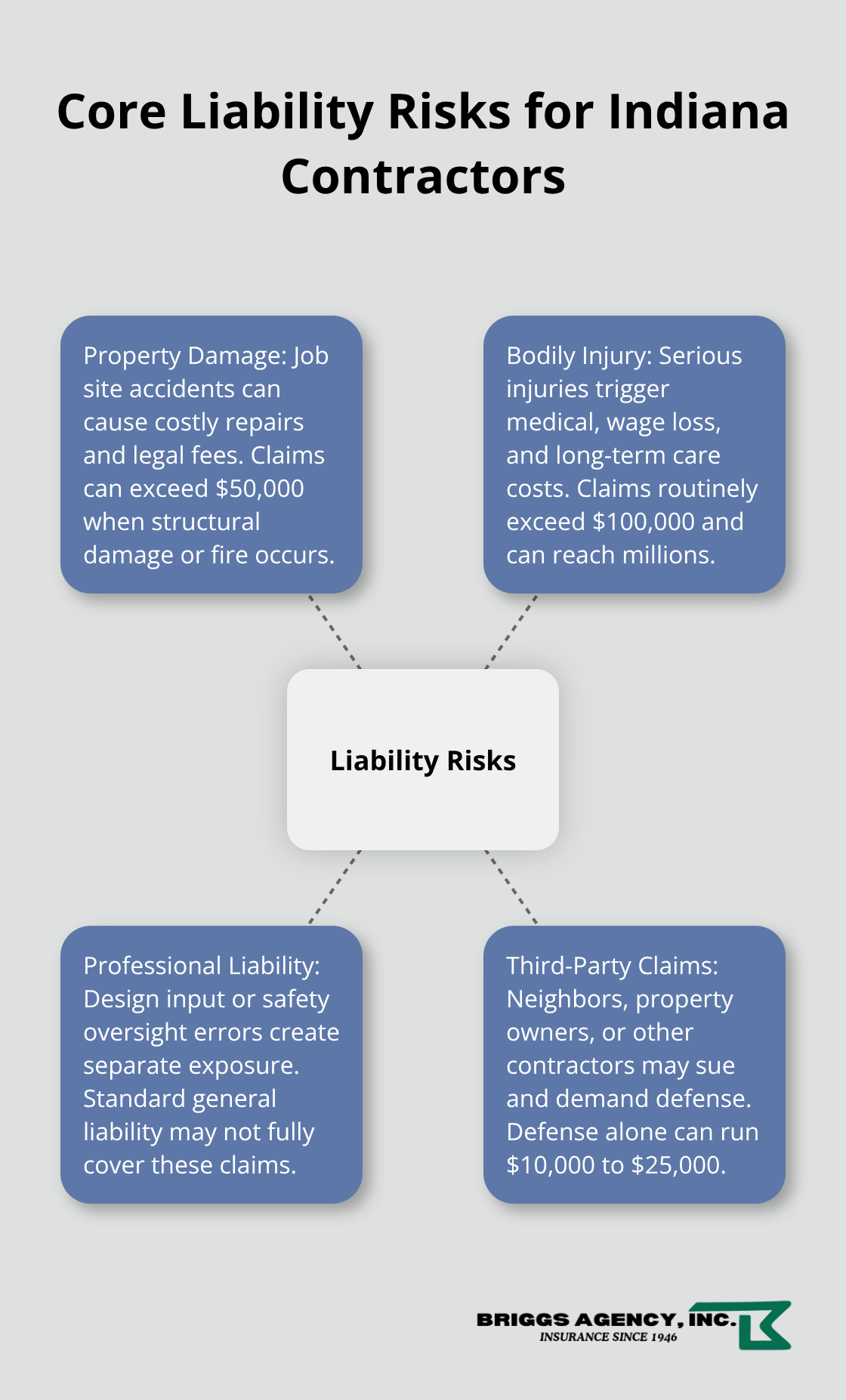

Property damage on job sites happens faster than most contractors expect. A dropped tool through a client’s roof, equipment damage during transport, or accidental structural harm during renovation work costs thousands in repairs and legal fees. Indiana contractors face these claims regularly, and without proper coverage, a single incident wipes out months of profit. General liability insurance covers these scenarios, but many contractors underestimate the actual dollar exposure. A roofing mistake that damages underlying structure, improper demolition that harms adjacent property, or equipment that causes fire damage easily exceeds $50,000 in claims. The cost isn’t just the repair bill-it includes investigation expenses, legal defense, and settlements that drag on for months.

Bodily Injury Claims Create Overlapping Liability Exposure

Bodily injury claims on job sites present even steeper financial risk. Construction accidents involving your workers, subcontractors, or third parties create multiple layers of liability. If a worker from your subcontractor gets injured on your project and their employer’s workers’ compensation coverage proves insufficient, they may pursue a third-party claim against you. Indiana’s workers’ compensation system is designed to provide medical benefits and partial wage replacement without requiring the injured worker to prove fault. However, third-party liability claims allow them to sue for additional damages when another party shares fault. A serious injury claim-permanent disability, lost wages, ongoing medical care-routinely exceeds $100,000 and can reach into the millions. Your general liability policy covers defense costs and damages, but inadequate limits leave you personally liable for anything beyond your policy cap.

Professional Liability and Third-Party Claims Add Separate Exposure

Professional liability claims add another layer of risk. If you provide design input, consult on building methods, or oversee safety protocols, errors or negligence in those services create separate exposure. A faulty design recommendation or failure to catch a safety violation that causes injury opens you to claims that standard general liability doesn’t fully cover. Third-party claims also arise when property owners, neighboring businesses, or other contractors sue you for damages caused by your work. These lawsuits demand legal defense even before determining fault, and defense costs alone reach $10,000 to $25,000 depending on complexity. Your insurer covers these expenses, but only if you maintain adequate professional liability or general liability limits. Delayed notification to your insurer can void coverage, so reporting incidents immediately becomes non-negotiable.

Understanding these three liability categories-property damage, bodily injury, and third-party claims-shows why Indiana contractors cannot afford to underinsure. Each risk category carries its own financial exposure, and they often overlap on the same project. The next section examines what Indiana law actually requires contractors to carry and how state regulations shape your coverage obligations.

Indiana Contractor Insurance Requirements and Regulations

Local Licensing Rules Vary Across Indiana Cities

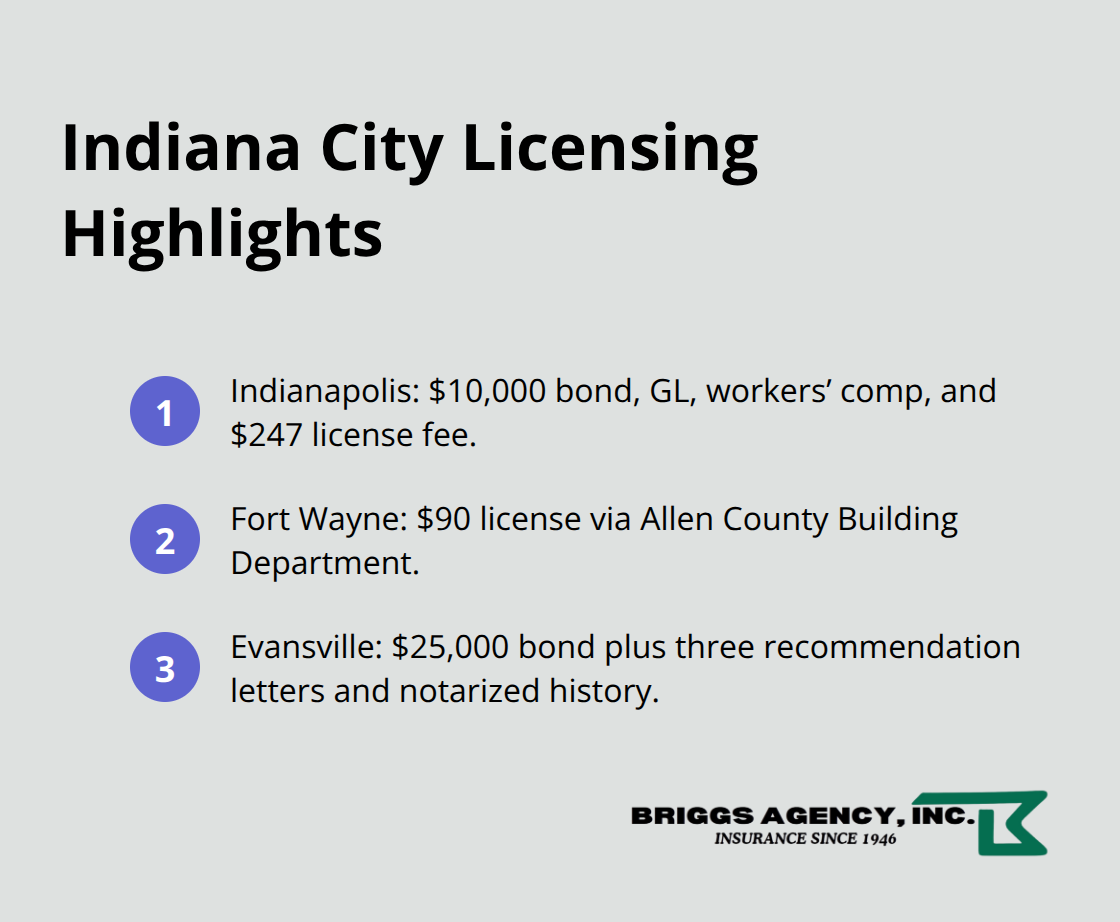

Indiana has no statewide general contractor license requirement, but that doesn’t mean you operate without regulations. Local jurisdictions set their own rules, and they differ significantly across the state. In Indianapolis, the Department of Business and Neighborhood Services issues general contractor licenses and requires a $10,000 surety bond, proof of business registration, general liability insurance, workers’ compensation coverage, and a $247 license fee. Fort Wayne contractors pay $90 for a general contractor license through the Allen County Building Department, while Evansville requires a $25,000 surety bond, three letters of recommendation, and notarized criminal history forms through the Vanderburgh County Building Commission. Your licensing obligations depend entirely on where you operate.

If you work across multiple Indiana cities, you manage different fees, different bond amounts, and different renewal cycles. Indianapolis licenses expire every two years; Fort Wayne renews annually; Evansville offers one-year or two-year options. Skipping compliance costs you fines, lost bids, and potential license suspension.

Workers’ Compensation Coverage Is Non-Negotiable

Workers’ compensation insurance is mandatory in Indiana if you have employees, and this requirement has no gray area. Your insurer covers medical expenses, wage replacement, and vocational rehabilitation for job site injuries without your employees proving fault. This no-fault system protects workers and shields you from direct employee lawsuits over workplace injuries, but only if you maintain active coverage. The moment you hire your first employee, you must carry workers’ compensation or face penalties that exceed the cost of the policy itself.

General Liability Forms Your Foundation

General liability insurance forms the foundation of contractor protection and is often required by local licensing authorities or client contracts. It covers bodily injury, property damage, and legal defense costs when third parties claim harm from your operations. Many contractors assume general liability handles everything, but it doesn’t cover professional liability claims if you provide design services or safety consulting. Your actual coverage limits matter enormously. A $1 million general liability policy sounds solid until a serious injury claim hits $1.5 million, leaving you personally liable for the gap. Contractors in Indiana typically carry $1 million to $2 million in general liability limits depending on project size and risk.

Additional Coverage Types Protect Specific Exposures

Commercial auto insurance is mandatory for business-owned vehicles and covers work-related accidents. Tools and equipment insurance protects your job site gear from theft or damage. Professional liability becomes essential if you oversee safety programs or provide construction consulting. A Business Owner’s Policy bundles general liability with commercial property insurance to reduce costs while covering both liability and on-site equipment or materials.

Understanding Your Premium Costs

Insurance costs vary based on business size, claims history, and services offered. General liability averages around $100 per month, workers’ compensation around $168 per month, and commercial auto around $180 per month for Indiana contractors according to industry data. Your specific premiums depend on your operation’s details, so obtaining actual quotes from carriers beats guessing. Check with your specific city or county government before taking on projects, because assuming you know the rules across all your service areas will hurt you eventually. Once you understand what Indiana requires and what coverage costs, the real challenge becomes selecting limits and deductibles that actually protect your business without overpaying for unnecessary coverage.

How to Choose the Right Contractor Liability Coverage

Map Your Actual Job Site Exposure

Start by mapping your actual job site exposure instead of copying another contractor’s policy limits. A residential kitchen remodel carries vastly different risk than commercial office construction or demolition work. Your property damage exposure depends on what you touch-a drywall contractor working inside existing homes faces lower structural damage risk than a foundation specialist or roofer whose mistakes affect building integrity. Bodily injury exposure scales with project complexity and crew size. A solo painter has minimal workers’ compensation claims risk; a general contractor managing fifteen subcontractors on a commercial site faces exponential injury exposure.

Review your past three years of projects and identify which ones created the most significant liability concerns. Did you work near occupied buildings where property damage could harm neighboring businesses? Did you handle heavy equipment or work at heights where serious injuries become likely? Did you provide any design input or safety oversight that extends beyond standard execution? These specifics determine whether $1 million in general liability suffices or whether $2 million makes sense.

Set Coverage Limits That Protect Your Business

Indiana contractors need liability insurance to protect their business-most client contracts and municipal requirements demand $1 million minimum. For larger commercial projects or high-risk work like demolition or excavation, $2 million becomes standard. Professional liability becomes non-negotiable if you design safety systems, specify materials, or consult on construction methods. A $1 million professional liability policy costs roughly $40 to $60 monthly but protects you when design recommendations cause injury or property damage.

Deductibles represent your out-of-pocket responsibility before insurance kicks in. A $500 deductible means you pay the first $500 of any claim; a $2,500 deductible cuts your premium but increases your risk. Most Indiana contractors choose $1,000 deductibles as the practical middle ground-low enough to absorb without destroying cash flow, high enough to reduce premiums meaningfully. Higher deductibles make sense only if you maintain substantial emergency reserves.

Get Quotes and Compare Carrier Options

Actual quotes from multiple carriers reveal how your specific operation affects pricing far better than industry averages. A roofing contractor with fifteen employees and five years of claims history pays dramatically different premiums than a residential painter with no employees and a clean record. When you contact an agent, have your business revenue, number of employees, types of projects, claims history, and service areas ready. Agents ask these questions not to be intrusive but because they directly impact your premium and coverage suitability.

A contractor claiming $500,000 annual revenue but carrying $2 million in general liability with a $500 deductible is likely overpaying; another contractor with $2 million revenue and only $1 million coverage is gambling. Your agent can identify these misalignments and adjust limits and deductibles to match both your risk profile and budget. Compare quotes from multiple top-rated carriers to find competitive pricing without sacrificing coverage.

Bundle Policies and Add Specialized Coverage

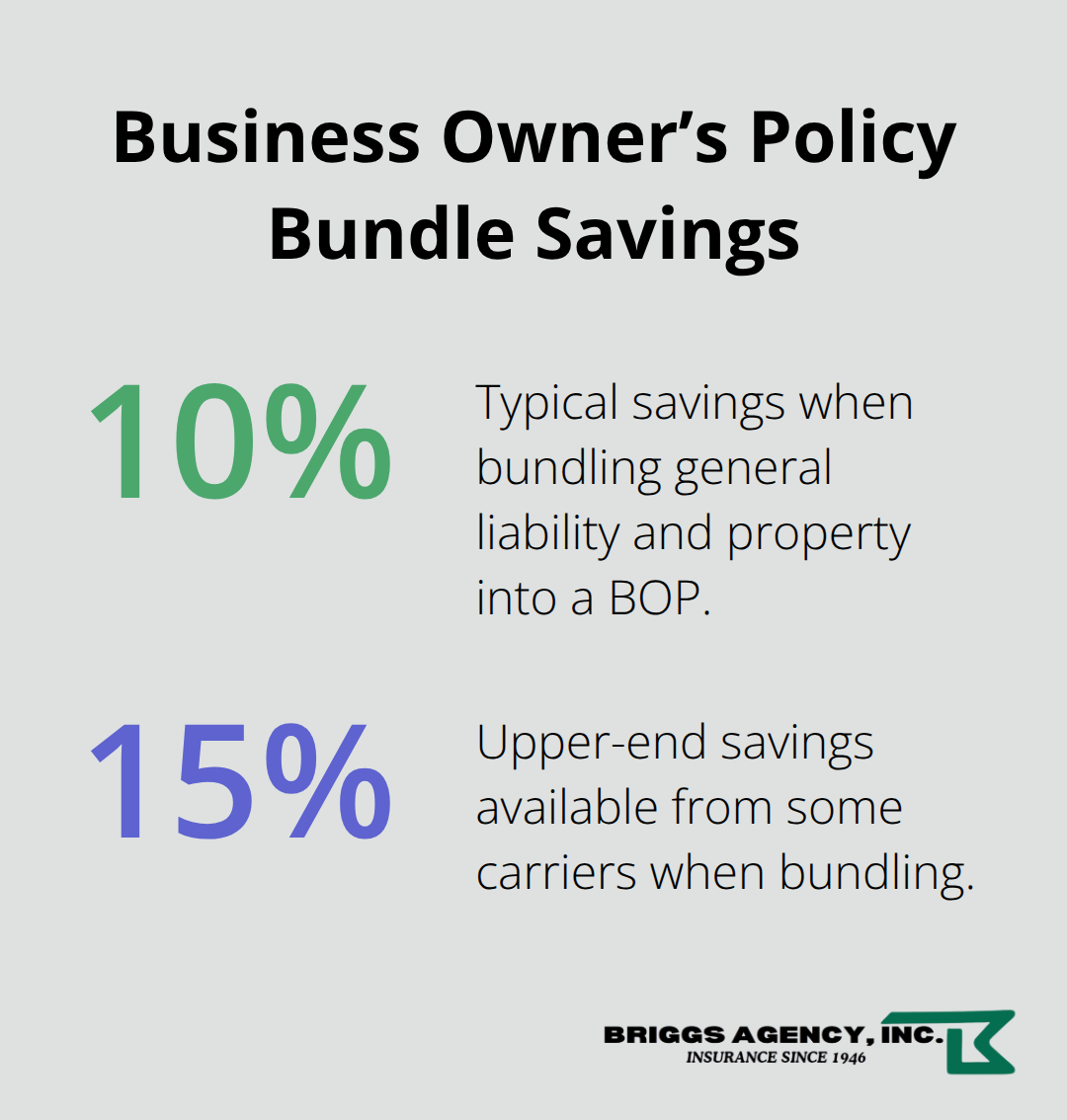

Bundling general liability with commercial property insurance through a Business Owner’s Policy typically saves 10 to 15 percent compared to purchasing policies separately. If you own equipment, tools, or materials stored on job sites, inland marine coverage protects against theft and damage-an essential add-on for contractors whose equipment represents significant capital investment. Request certificates of insurance from your agent once policies activate; many client contracts require proof of coverage before work begins, and delays in obtaining certificates cost you project start dates and client relationships.

Final Thoughts

Protecting your contracting business starts with honest assessment of your actual risks and ends with coverage that matches those risks without gaps or waste. Indiana contractor liability insurance isn’t a checkbox item or a cost to minimize-it’s the financial foundation that keeps your business standing after accidents happen. Property damage, bodily injury, and third-party claims overlap constantly on real job sites, which means underestimating any one of them puts your entire operation at risk.

Your licensing obligations vary by city, your workers’ compensation requirement is absolute if you have employees, and your general liability limits must reflect the scale and complexity of your projects. A $1 million policy works for smaller residential work; larger commercial projects demand $2 million or more. Professional liability becomes essential the moment you provide design input or safety oversight, and deductibles should balance premium savings against your ability to absorb out-of-pocket costs without disrupting operations.

The practical next step is gathering quotes from multiple carriers rather than accepting industry averages as your reality. Your specific business-your revenue, employee count, claims history, and project types-determines your actual premium and appropriate coverage limits. We at Briggs Agency, Inc. have guided Indiana contractors through these decisions since 1946, and we compare options to tailor policies that deliver competitive pricing and the right protection for your operation.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.