Restaurant Equipment Breakdown Insurance: Safeguarding Your Kitchen Backups

Your kitchen equipment is the backbone of your restaurant’s operations. When a refrigerator, fryer, or oven fails unexpectedly, the financial damage extends far beyond the repair bill-lost revenue from closed service windows can devastate your bottom line.

Restaurant equipment breakdown insurance protects you from these costly surprises. At Briggs Agency, Inc., we help restaurant owners understand how this coverage works and why it matters for your business.

What Equipment Breakdown Insurance Actually Covers

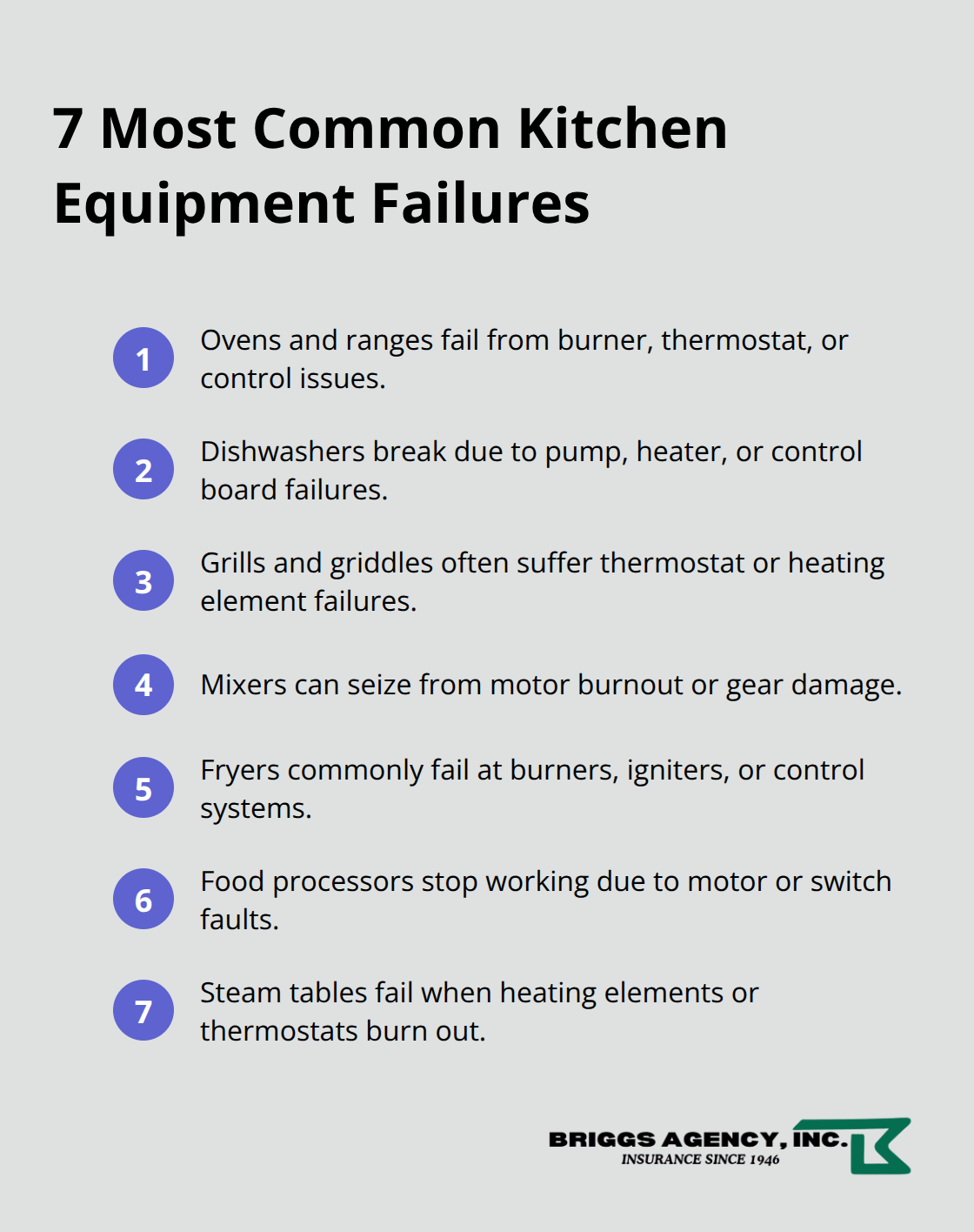

Equipment breakdown insurance protects your restaurant from the sudden, internal failure of mechanical and electrical systems that standard property policies ignore. When your walk-in freezer’s compressor fails, a power surge fries your POS system, or your commercial oven’s heating element burns out, this coverage pays for repairs, replacement costs, and the income you lose while equipment sits idle. Your standard policy covers external threats like fire or theft, but it leaves you exposed when equipment fails from the inside. Equipment breakdown insurance fills that gap by covering the seven most common kitchen failures: ovens and ranges, dishwashers, grills and griddles, mixers, fryers, food processors, and steam tables. It also protects electrical systems including transformers and panels, refrigeration units like walk-ins and ice machines, boilers and pressure equipment, HVAC systems, and even computers and security gear. The coverage includes not just repair or replacement costs but also spoilage losses when refrigeration fails and perishable inventory spoils, plus lost business income during downtime.

Why Spoilage Coverage Matters More Than You Think

Spoilage protection separates adequate coverage from inadequate coverage. A single refrigeration failure costs thousands in spoiled inventory within hours-far more than the repair bill itself. If your walk-in cooler breaks on a Friday night, you replace hundreds of dollars in meat, produce, and prepared foods on top of paying a technician. Equipment breakdown insurance covers these replacement costs directly, preventing one equipment failure from wiping out your weekly food cost margin. This protection proves especially valuable for restaurants that stock high-value proteins or specialty ingredients.

The Real Cost of Downtime Without Protection

The financial impact of equipment failure extends beyond spoilage and repair bills. When your fryer stops working during lunch service, you lose the revenue from every order you cannot fulfill. When your dishwasher fails, you either close for service or manually wash dishes and slow your entire operation to a crawl. Equipment breakdown insurance reimburses this lost income, helping you stay afloat during unexpected closures. Without it, a three-day equipment failure forces you to dip into operating capital or take on debt just to cover payroll and rent while repairs happen.

Coverage That Protects Your Entire Kitchen Ecosystem

Equipment breakdown insurance covers far more than just cooking equipment. Your electrical systems (transformers, panels, power cables) receive protection, as do communications and security systems (computers, POS terminals, CCTV, fire alarms). Mechanical systems like water pumps, ventilation, motors, and specialized production equipment fall under coverage. Boilers and pressure equipment (heating units, hot water systems, cookers, sterilizers) are typically included, along with refrigeration systems that keep your inventory safe. This comprehensive approach means a single policy protects the interconnected systems your restaurant depends on every single day.

What Separates Equipment Breakdown from Standard Property Insurance

Standard commercial property insurance covers external perils-fire, theft, weather damage-but explicitly excludes internal mechanical and electrical failures. Equipment breakdown insurance addresses the opposite risk: it covers sudden, accidental internal failures while excluding wear and tear or gradual faults. The two policies complement each other (not compete), creating a complete protection strategy. Most restaurant owners discover this gap only after an equipment failure leaves them unprotected, which is why understanding the distinction matters before you need to file a claim. The next step involves assessing your specific equipment inventory and determining what coverage limits actually protect your operation.

Why Restaurant Owners Need Equipment Breakdown Coverage

The True Cost of Your Kitchen Equipment

Commercial kitchen equipment represents one of your largest capital investments, and unexpected failure creates severe financial consequences. A walk-in freezer compressor costs $3,000 to $8,000 to replace, but the spoiled inventory inside costs far more. A commercial oven replacement runs $5,000 to $15,000 depending on capacity. A commercial kitchen equipment replacement costs POS system overhaul hits $1,000 to $5,000.

These aren’t theoretical numbers-they’re the actual replacement costs restaurant owners face when equipment fails. Standard property insurance ignores these internal failures entirely, leaving you personally responsible for both the replacement equipment and the income lost while your kitchen sits idle.

How Equipment Breakdown Insurance Protects Your Bottom Line

Equipment breakdown insurance fills this gap that standard policies leave open. The coverage pays for repair costs, replacement expenses, and the revenue you lose during downtime. Without it, a single equipment failure forces you to choose between closing temporarily and absorbing thousands in losses or staying open while operating at reduced capacity. One failed compressor or burned-out heating element can drain your cash reserves faster than you can recover.

The Hidden Financial Impact of Downtime

The financial impact of downtime extends far beyond the repair bill itself. The National Restaurant Association projects U.S. foodservice sales to exceed $1 trillion in 2025, which means downtime affects not just your daily revenue but your ability to meet customer expectations and maintain your reputation. When your dishwasher fails during dinner service, you face two bad options: close for service and lose that night’s revenue, or manually wash dishes and slow your entire operation while customers wait longer for tables.

A three-day refrigeration failure forces you to discard hundreds of dollars in perishable inventory on top of paying for emergency repairs and losing the income from meals you couldn’t prepare. Equipment failures hit hardest during peak seasons when you cannot afford to close, yet that’s precisely when your equipment works hardest and fails most often. For restaurants operating on typical 3 to 5 percent profit margins, a single week of equipment downtime without protection eliminates an entire month’s profit.

Why Spoilage Coverage Separates Adequate Protection from Inadequate Protection

Equipment breakdown insurance reimburses lost income during repairs, covers spoilage costs directly, and pays for emergency labor charges-protecting your cash flow when you need it most. Spoilage protection alone justifies the coverage cost. A single refrigeration failure costs thousands in spoiled inventory within hours, far exceeding the repair bill. If your walk-in cooler breaks on a Friday night, you replace hundreds of dollars in meat, produce, and prepared foods on top of paying a technician. Equipment breakdown insurance covers these replacement costs directly, preventing one equipment failure from wiping out your weekly food cost margin.

Understanding what your kitchen equipment actually costs to replace and how long you could survive without that equipment reveals why this coverage matters. The next step involves assessing your specific equipment inventory and determining what coverage limits actually protect your operation.

How to Choose the Right Equipment Breakdown Policy

Inventory Your Equipment and Calculate Real Replacement Costs

Start with a complete inventory of your kitchen equipment and its replacement cost. Walk through your kitchen and list every piece of commercial equipment that would disrupt service if it failed: refrigerators, freezers, ovens, ranges, fryers, grills, dishwashers, ice machines, POS systems, HVAC units, boilers, and any specialized equipment specific to your cuisine. Contact your equipment suppliers or check recent invoices to determine actual replacement costs, not guesses. A commercial walk-in cooler runs $8,000 to $15,000 installed. A high-capacity commercial oven costs $5,000 to $12,000. A POS system overhaul hits $1,000 to $5,000. These specific numbers matter because your coverage limits must reflect what you would actually spend to replace failed equipment. Underestimating replacement costs leaves you exposed to gaps when you file a claim. Most restaurant owners discover this mistake too late, after equipment fails and they cannot replace it quickly because their coverage limits fall short of actual replacement expenses.

Set Coverage Limits That Match Your Equipment Value

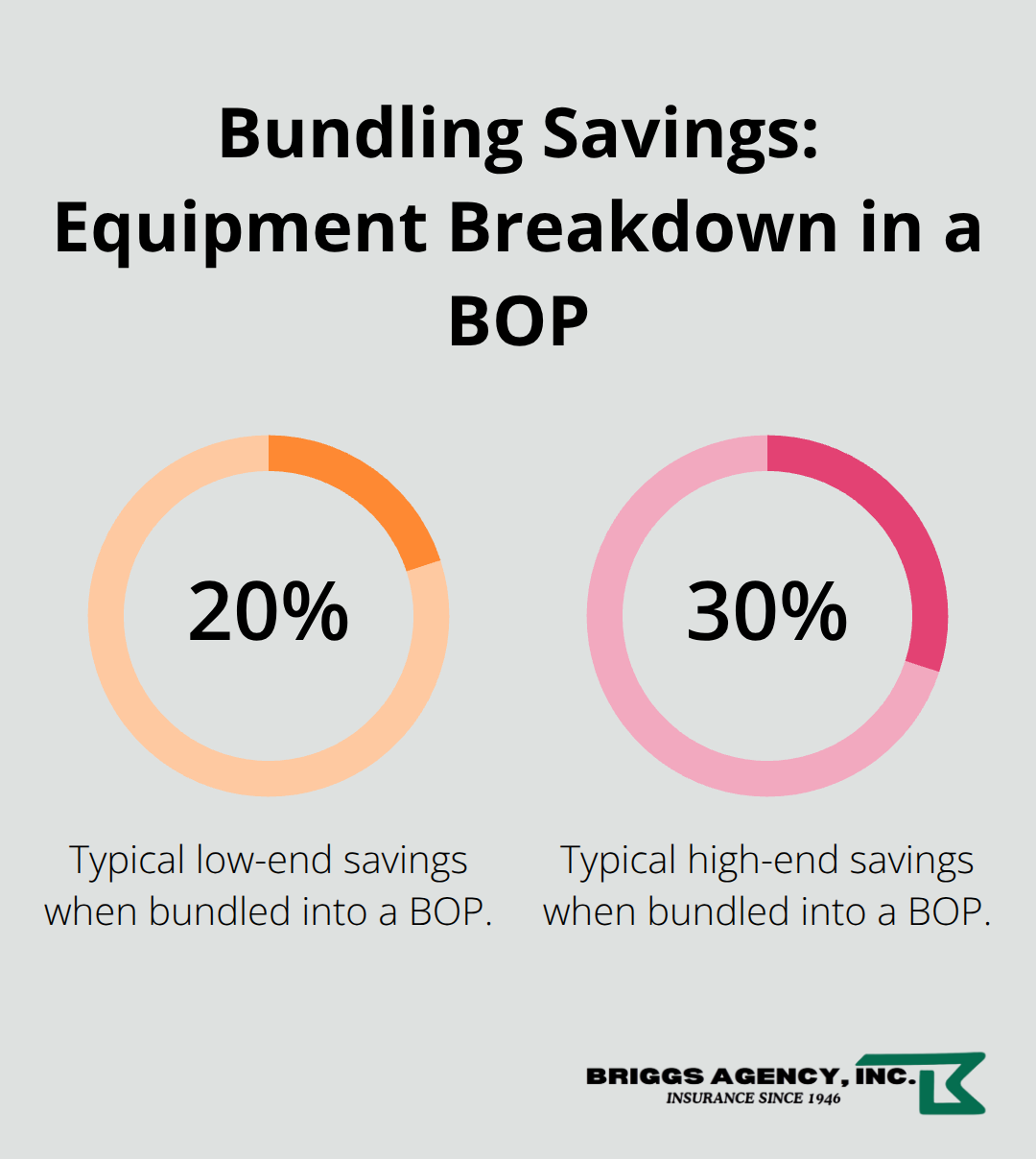

Your coverage limits should equal your total equipment replacement value plus estimated spoilage losses. For a full-service restaurant with extensive cooking equipment, this typically ranges from $50,000 to $150,000 depending on kitchen size and equipment mix. Fast-casual restaurants with fewer fryers and griddles may need $30,000 to $75,000. The National Restaurant Association notes that bundling equipment breakdown coverage into a Business Owner’s Policy typically saves 20 to 30 percent compared to purchasing separate policies, and costs often start around $5 per month when added as an endorsement.

Choose a Deductible That Fits Your Cash Flow

Your deductible directly affects your premium: a $1,000 deductible costs less than a $500 deductible, but forces you to absorb more of each claim. Choose a deductible you can comfortably pay from operating cash without straining your business. A higher deductible works well if your restaurant maintains strong cash reserves and can weather small repair costs. A lower deductible makes sense if equipment failures would strain your ability to pay out of pocket (for example, if your profit margins run thin or seasonal revenue fluctuates significantly).

Work with a Local Agent to Customize Your Protection

A local insurance agent can walk you through your specific equipment, help you calculate realistic replacement costs, and recommend coverage that matches your actual risk profile rather than generic industry averages. They compare multiple carriers to find the best combination of coverage, cost, and claims support for your restaurant’s unique equipment mix and operational needs. We at Briggs Agency, Inc. represent multiple top-rated carriers, which allows our experienced local agents to tailor policies that deliver competitive pricing and the right protection for your restaurant’s specific situation.

Final Thoughts

Equipment breakdown insurance protects your restaurant from financial devastation when mechanical or electrical failures strike. The coverage pays for repairs, replacement costs, spoilage losses, and lost income during downtime-gaps that standard property insurance simply does not address. For restaurants operating on thin profit margins, a single week without critical equipment can eliminate an entire month’s earnings, making restaurant equipment breakdown insurance a practical investment rather than an optional add-on.

Your next step is straightforward: inventory your kitchen equipment, calculate realistic replacement costs, and determine what coverage limits actually protect your operation. Choose a deductible that fits your cash flow situation, then connect with an insurance professional who understands restaurant operations and can compare multiple carriers to find competitive pricing and the right protection for your specific equipment mix. We at Briggs Agency, Inc. represent multiple top-rated carriers, which means we compare options rather than push a single solution.

Contact Briggs Agency, Inc. today to discuss how equipment breakdown coverage fits into your complete protection strategy. Our local agents are ready to walk you through your specific situation and help you avoid the financial devastation that equipment failures cause.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.