Restaurant Business Interruption: Planning for Revenue Gaps

Restaurant closures happen fast, and when they do, the financial damage spreads quickly. A single equipment failure, health code violation, or weather event can shut down your doors for days or weeks, leaving you scrambling to cover payroll and rent while revenue stops cold.

At Briggs Agency, Inc., we’ve seen how restaurant business interruption catches owners off guard. The good news is that proper planning and the right insurance can protect your bottom line when the unexpected strikes.

What Threatens Your Restaurant’s Operations

Weather, Utilities, and Supply Chain Risks

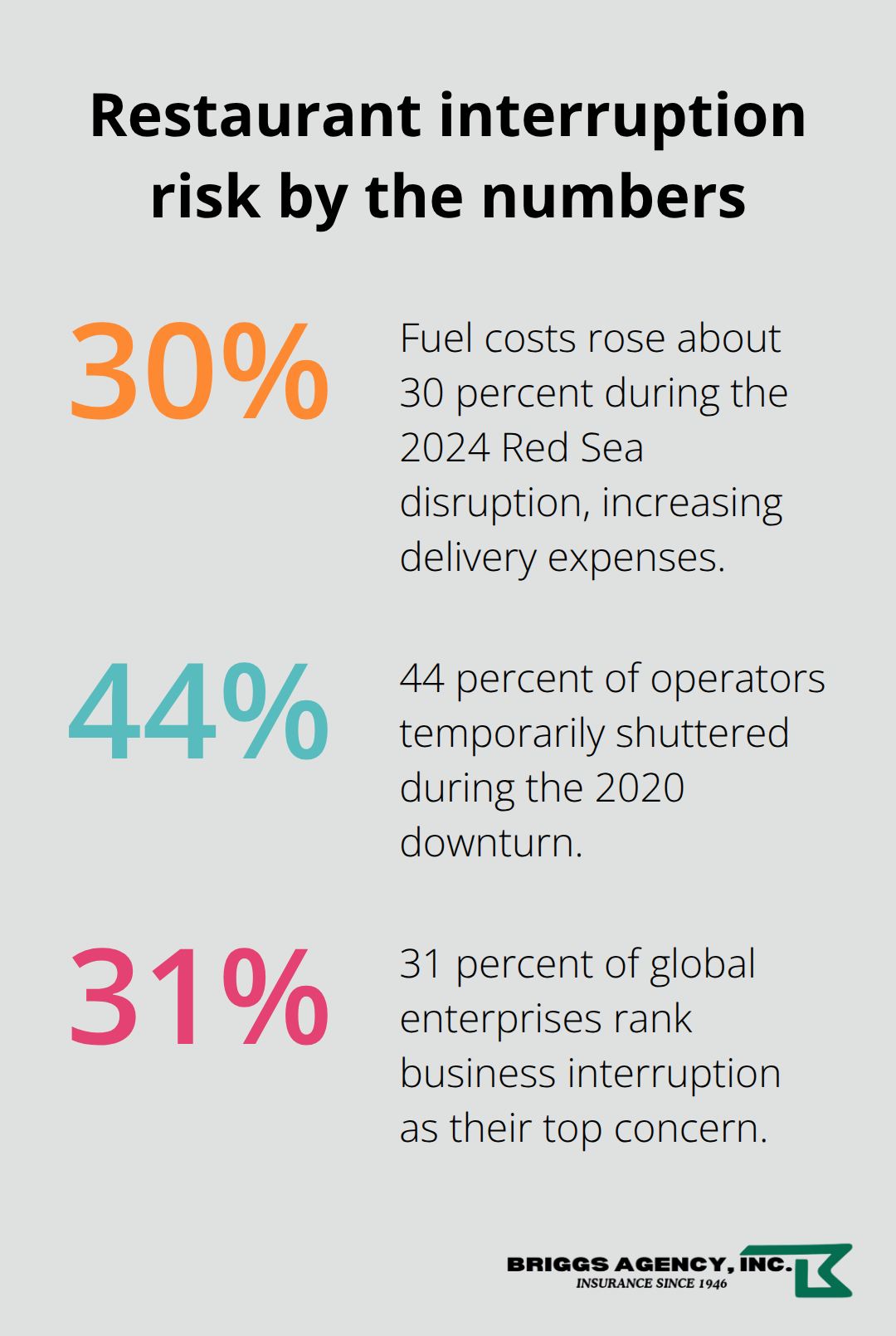

Weather events and utility failures hit restaurants harder than most businesses because operations depend on continuous power, reliable deliveries, and consistent staffing. Utility outages cause immediate revenue loss, a risk that intensifies during Atlantic hurricane season from June through November. Equipment breakdowns compound the problem-a failed walk-in cooler or kitchen range stops service for hours, spoils inventory, and forces menu cuts that drive customers away. Supply chain disruptions extend downtime unpredictably. The Red Sea shipping disruption in 2024 added roughly 4,000 miles and 2–3 weeks to shipments for restaurants relying on global suppliers, with fuel costs rising about 30 percent. A missing delivery of specialty ingredients forces menu changes that reduce revenue.

Health Code Violations and Disease Outbreaks

Health code violations and disease outbreaks create a different kind of threat. A positive COVID case among staff or a health inspection failure forces an immediate shutdown, and the World Health Organization’s 2020 pandemic declaration exposed a critical gap: many restaurant insurance policies exclude non-damage interruptions like disease outbreaks, leaving owners unprotected when forced closures happen without physical damage to the building.

Staffing Gaps and Their Revenue Impact

Staffing departures directly shrink seating capacity and sales. A missing server reduces revenue by shortening how many tables you can serve during a shift. The Canadian Federation of Independent Business reports that about 1 in 4 small businesses permanently close after a disaster, and Forbes Tech Council data shows 44 percent of operators temporarily shuttered during the 2020 downturn while fixed costs like mortgage and rent continued to accumulate.

Kitchen hazards compound staffing challenges, as your team faces constant exposure to burns, cuts, and slip hazards in tight spaces with high-pressure operations.

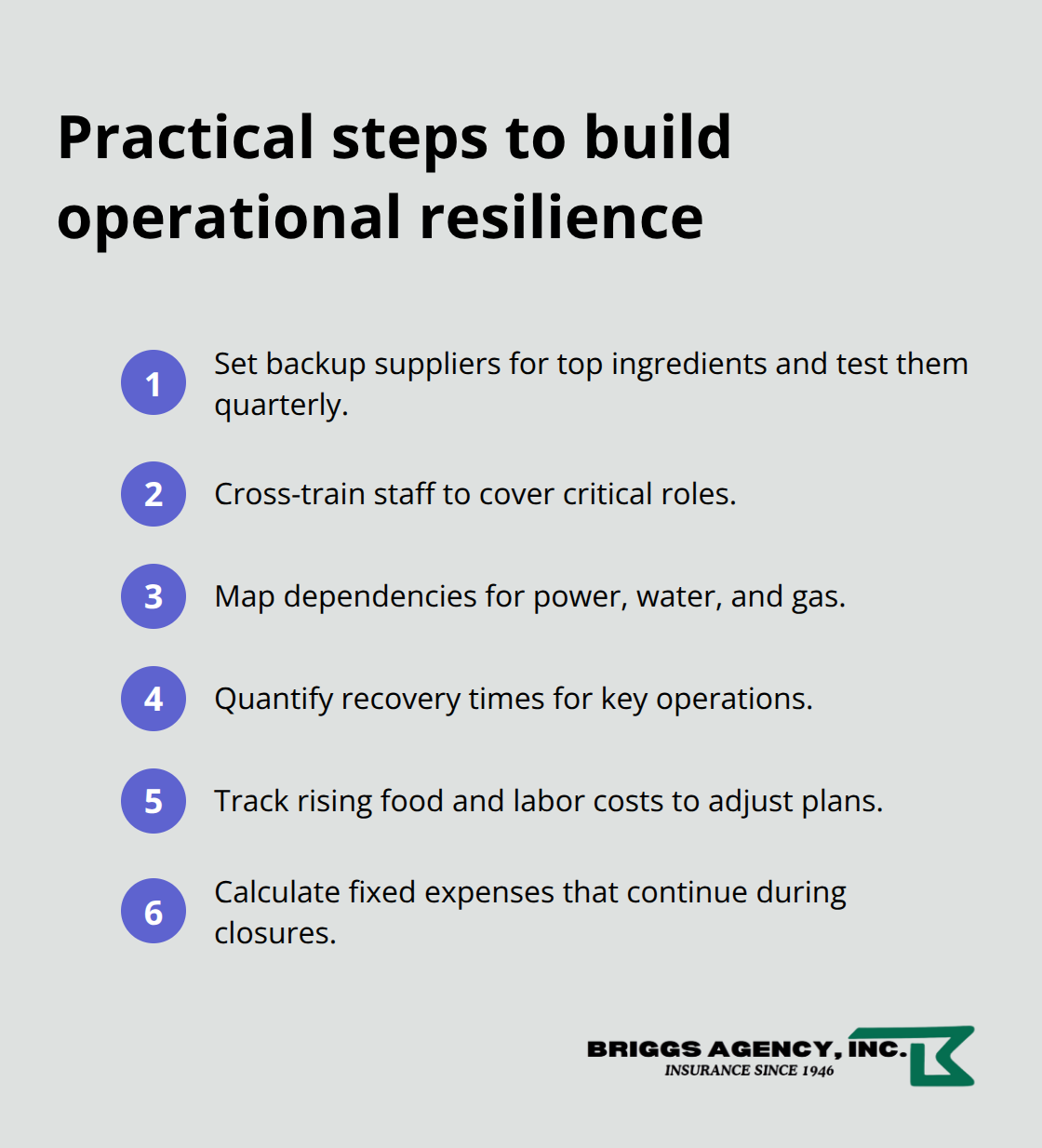

Building Operational Resilience

These aren’t theoretical risks-they’re operational realities that demand concrete planning. Identify at least two backup suppliers for your top 20 ingredients and test them quarterly to protect against single-point failures. Cross-train staff so multiple people handle critical roles; a single absence won’t shut down service. Map your dependencies-which operations fail if electricity drops, if water stops, if gas lines rupture-and quantify recovery times.

Food costs have risen roughly 25 percent and labor costs roughly 18 percent over the past two years according to Restaurants Canada, which means fixed overhead during a closure drains cash faster than ever. The threat isn’t whether an interruption happens; it’s how fast you can respond and how well you’re protected when it does. That protection starts with understanding what your operation actually costs to maintain when revenue stops.

What Really Costs You When Revenue Stops

The Immediate Financial Drain

A three-day closure from a kitchen fire doesn’t just mean three days without sales. During those 72 hours, your mortgage or lease payment still arrives, your insurance premiums don’t pause, and your utilities keep running even though the kitchen sits dark. According to the Allianz Global Survey 2024, 31 percent of global enterprises rank business interruption as their top concern, and restaurants face this risk acutely because fixed costs dwarf variable ones. Food costs and labor fluctuate with volume, but rent, property taxes, loan payments, and baseline utility costs remain fixed whether you operate or stay closed. The math turns brutal fast: a mid-sized restaurant with 150 covers per day at a 30 percent profit margin loses roughly 4,500 dollars in daily profit during a forced closure. That same restaurant still owes 3,000 to 5,000 dollars in fixed monthly expenses divided across daily operations. Three weeks of downtime means 15,000 to 35,000 dollars in lost profit plus another 10,000 to 15,000 dollars in fixed costs that consumed cash with zero revenue to offset them.

Rising Costs Amplify the Damage

Restaurants Canada reports that food costs rose roughly 25 percent and labor costs roughly 18 percent over the past two years, which means your fixed-cost burden has grown while margins have compressed. A disruption that might have been survivable five years ago now threatens the business itself. Your overhead expenses accelerate the financial crisis during any shutdown. Mortgage payments, property taxes, insurance premiums, and loan obligations don’t pause for closures-they accelerate the cash drain. Equipment leases, franchise fees, and utility minimums continue accumulating. A two-week closure that once cost 20,000 dollars in lost profit now costs 30,000 dollars or more because your baseline expenses have risen faster than your ability to raise menu prices.

The Hidden Cost: Customer Loss and Market Share Erosion

The damage extends beyond the immediate shutdown period. When you reopen, customers don’t automatically return. About 1 in 4 small businesses permanently close after a disaster according to the Canadian Federation of Independent Business, and revenue loss during closure directly correlates with that failure rate. Your regulars discover competitors during your downtime, loyalty erodes, and staff departures compound the problem because experienced servers and kitchen staff take jobs elsewhere when you close unexpectedly. Market share loss isn’t theoretical-it’s measurable. A restaurant that closes for two weeks loses not just 14 days of revenue but also the ongoing revenue from customers who shifted their habits. Recovery takes months, not days. Some never come back.

Why Insurance Bridges the Gap

Business interruption insurance compensates for lost income and helps pay for ongoing expenses, ensuring your restaurant can recover and reopen without financial strain. The policy protects your ability to weather the storm and emerge intact. Understanding what coverage you actually need requires calculating your specific exposure-the daily revenue you generate, the fixed costs you carry, and how long your operation could survive without income. That calculation determines whether your current coverage matches your actual risk or leaves you exposed to a financial crisis that planning alone cannot prevent.

How Much Business Interruption Coverage Do You Actually Need

Calculate Your Daily Revenue and Fixed Costs

Business interruption insurance for restaurants isn’t about picking a number and hoping it covers the damage. It’s about calculating what your operation actually costs to maintain when revenue stops, then building coverage around that specific number. Start with your gross revenue from the last 12 months and divide it by 365 to find your average daily revenue. Then identify your fixed costs: mortgage or lease, property taxes, insurance premiums, loan payments, utility minimums, and payroll for salaried staff who stay on the payroll during a closure. These costs don’t pause when you close.

A restaurant generating 8,000 dollars in daily revenue with 3,500 dollars in fixed monthly expenses faces a brutal equation during downtime. Each day closed costs you roughly 267 dollars in fixed expenses plus the profit margin you would have earned on that day’s revenue. Over two weeks, that adds up to roughly 8,000 dollars in fixed costs alone, not counting lost profit.

Account for Rising Overhead and Compressed Margins

According to the National Restaurant Association, food and labor costs for the average restaurant have each gone up 35% over the last 5 years, which means your baseline overhead has expanded faster than your pricing power. That compression makes underinsurance far more dangerous than it was five years ago. Coverage limits should reflect your worst-case restoration timeline, not the average disruption. If a major equipment failure or supply chain collapse could force you closed for three weeks, your coverage should protect against a full three-week loss, not a one-week assumption.

Adjust your calculation for seasonality: a summer closure costs more for a restaurant with peak season revenue than a winter closure. Growth trends matter too. If you’ve expanded capacity or added a second location, your coverage needs to reflect that expanded exposure.

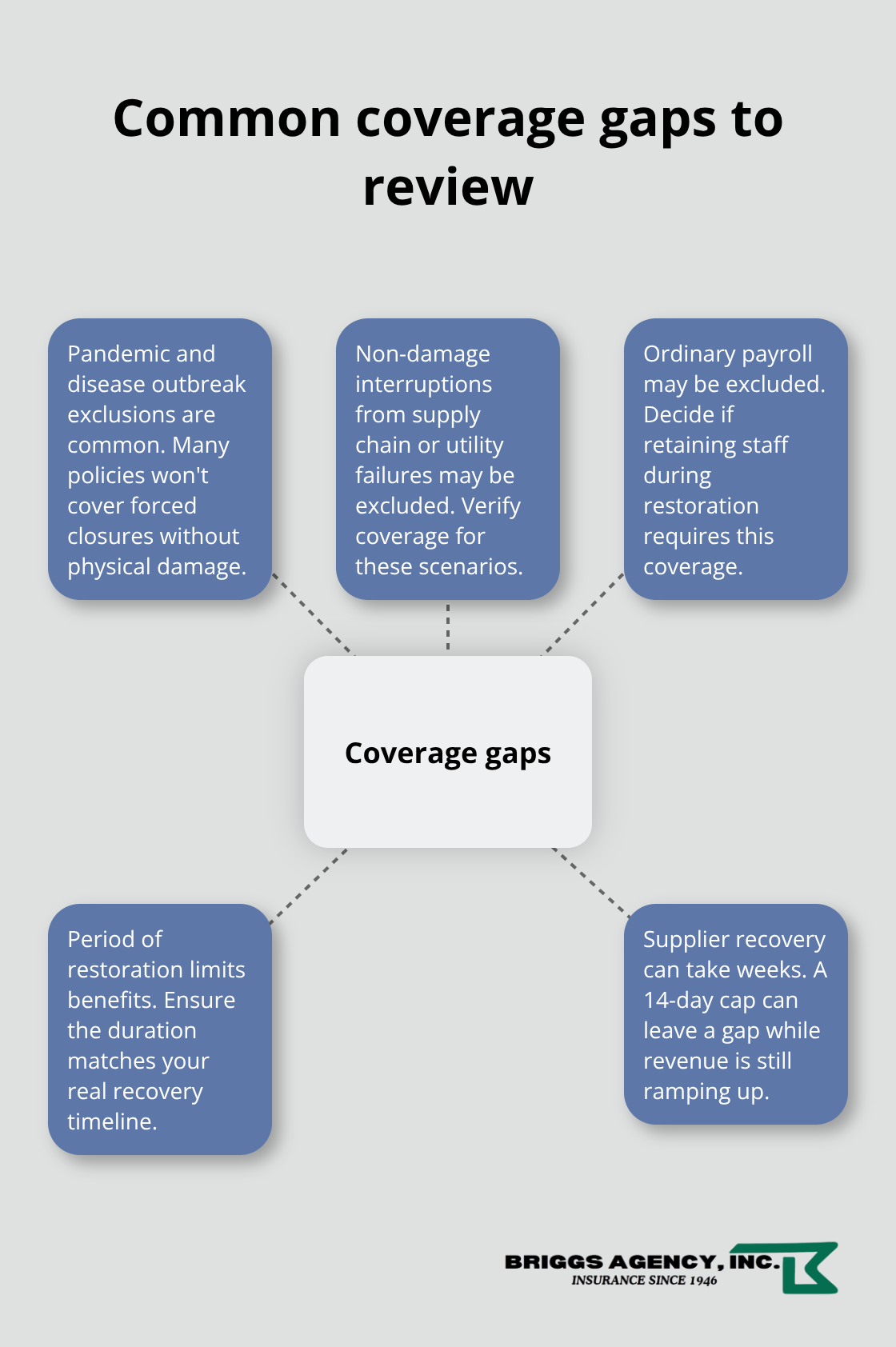

Identify Policy Exclusions and Coverage Gaps

The policy language itself determines what actually gets covered, and many restaurant owners miss critical gaps. Pandemic and disease outbreak exclusions appear in standard policies, a problem highlighted by the COVID-19 pandemic when many restaurants discovered their coverage didn’t protect against forced closures without physical property damage. Verify that your policy covers non-damage interruptions if your restaurant faces supply chain risk, utility disruptions, or health code enforcement actions.

Some policies exclude ordinary payroll entirely, cutting your premium but leaving you exposed when you need to retain your team during restoration. The period of restoration clause defines how long benefits run after you reopen. If your supplier network takes four weeks to fully restore after a disruption, but your policy covers only 14 days of restoration, you face a gap when revenue is still ramping up and fixed costs continue.

Extend Coverage for Longer Recovery Periods

Consider adding an extended restoration endorsement if your supply chain or customer recovery takes longer than standard terms. Work with an insurance professional who understands restaurant operations to review your specific policy language and identify exclusions that could leave you exposed. At Briggs Agency, Inc., our experienced local agents compare options across multiple carriers and tailor policies to match your actual risk, helping you avoid the gaps that catch restaurant owners off guard.

Final Thoughts

Restaurant business interruption strikes without warning, and the financial damage spreads fast when fixed expenses continue while revenue stops. A mid-sized restaurant loses thousands in daily profit during downtime, plus thousands more in fixed costs that never pause (mortgage, insurance, utilities, loan payments). Food and labor costs have risen sharply over the past two years, which means your overhead burden weighs heavier than ever, making even short closures financially devastating.

Business interruption insurance bridges the gap between what planning prevents and what it cannot. A solid continuity plan with backup suppliers, cross-trained staff, and documented procedures reduces your exposure and speeds recovery, but planning alone does not pay your mortgage when you face forced closure. Insurance covers lost income and ongoing expenses, protecting your ability to weather the storm and reopen without financial strain.

Calculate your actual daily revenue and fixed costs, then review your current coverage to see if it matches your real exposure. Check your policy language for exclusions around disease outbreaks, utility disruptions, and extended restoration periods. We at Briggs Agency, Inc. understand restaurant operations and can help you compare coverage options across multiple carriers to find protection that actually covers your bottom line when the unexpected strikes.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.