Trucking Insurance Coverage Indiana: How to Bundle for Real Savings

Running a trucking operation in Indiana means managing multiple insurance policies, and most fleet owners overpay because they haven’t bundled their coverage. We at Briggs Agency, Inc. work with trucking companies across the state who discover significant savings simply by combining their liability, physical damage, and cargo coverage with one carrier.

The right bundle cuts your premiums while eliminating the headache of juggling separate policies and agents. Let’s walk through how trucking insurance coverage Indiana actually works and where your real savings hide.

What Indiana Trucking Insurance Actually Covers

Liability Coverage: Your Legal Foundation

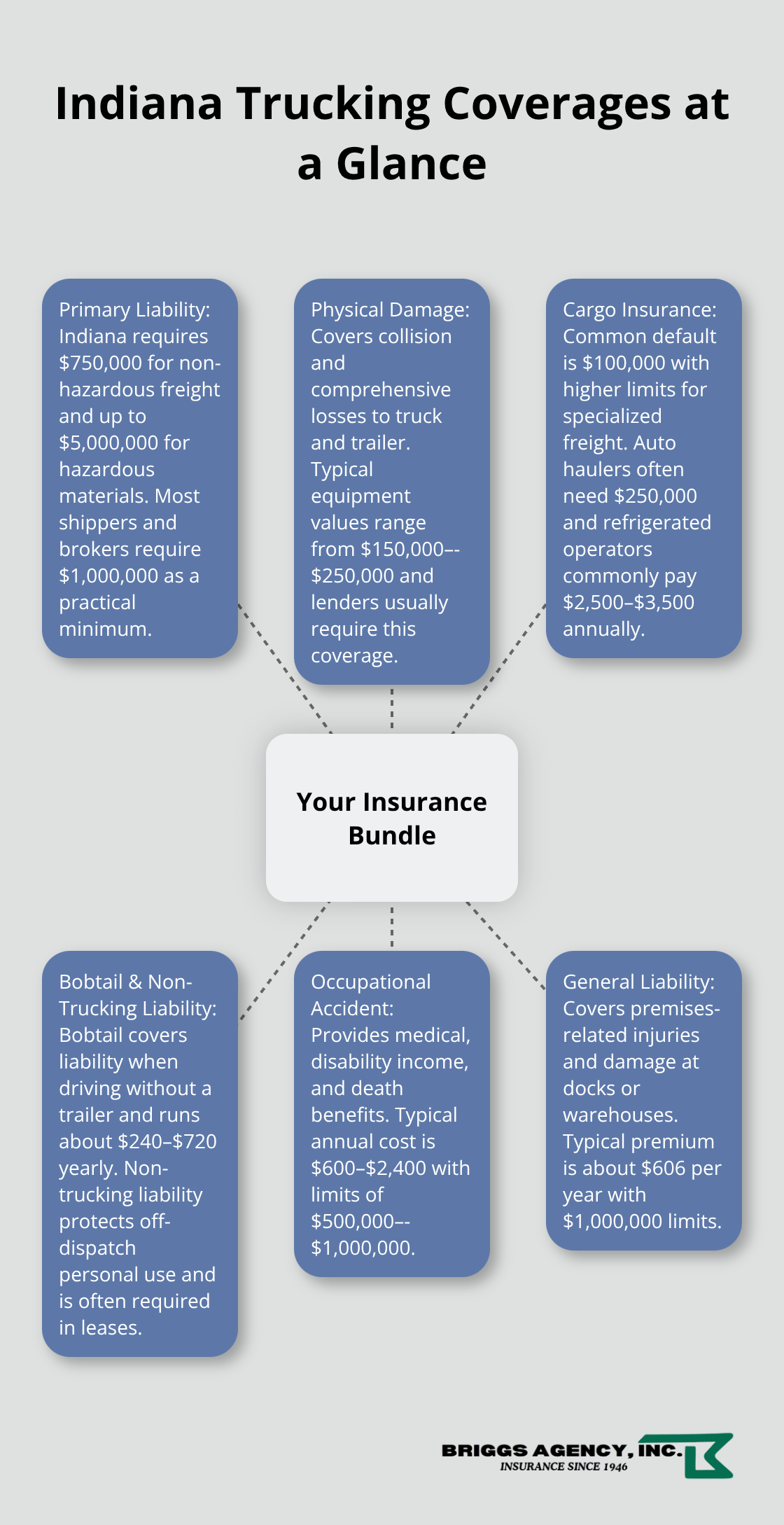

Indiana requires primary liability insurance with minimums of $750,000 for non-hazardous freight and up to $5,000,000 for hazardous materials, according to the Indiana Department of Revenue. Most shippers and brokers demand at least $1,000,000 in primary liability regardless of what the state requires, which means your actual floor sits higher than the legal minimum. In 2025, owner-operators typically pay $8,000–$15,000 annually for $1,000,000 in primary liability coverage, with new authorities landing at the higher end of that range.

Every liability policy includes an MCS-90 endorsement that guarantees public liability coverage and can cover defense costs exceeding $100,000 even when you’re not at fault. The Federal Motor Carrier Safety Administration reports 152,000+ truck accidents occurred in 2024, and the average injury-related crash costs around $148,279, which underscores why under-insuring exposes you to catastrophic financial risk.

Physical Damage and Cargo Protection

Physical damage coverage protects your truck and trailer from collision and comprehensive losses, and lenders almost always require it for financed equipment. Your typical operator equipment has a value between $150,000–$250,000, so the protection matters significantly to your bottom line. Motor truck cargo insurance commonly covers $100,000 by default for around $500–$1,800 per year, but specialized cargo demands higher limits. Auto haulers typically need $250,000 in cargo coverage, while refrigerated freight operators should expect $2,500–$3,500 annually.

Cargo theft costs the trucking industry more than $30 billion annually according to industry data, and many 2024–2025 policies exclude theft unless you add a specific endorsement. This gap in coverage can expose you to substantial losses if you transport high-value or theft-prone freight.

Additional Coverage for Indiana Operations

Beyond these core coverages, Indiana operations often need additional protection depending on what you haul and how you operate. Bobtail insurance covers liability when you drive a truck without a trailer and runs about $240–$720 yearly. Non-trucking liability insurance protects personal use of the truck off dispatch and costs roughly the same, but it differs from bobtail and many lease agreements require it.

Occupational accident insurance offers medical, disability income, and death benefits ranging from $600–$2,400 annually with typical limits of $500,000–$1,000,000, and most lease agreements make this mandatory. General liability insurance covers premises-related injuries and damage at loading docks or warehouses for about $606 per year with typical limits of $1,000,000.

How Your Driving Record and Safety Practices Affect Costs

Your motor vehicle record stands as the single most important rating factor for premiums, so maintaining a clean driving record directly lowers costs. Adding dual-facing dash cameras can reduce premiums by 5–15% and help protect against false claims. Telematics and safety data programs also unlock discounts as insurers reward technology-driven safety approaches.

Choosing the right coverage limits depends on your actual operation. Local and short-haul operations with non-hazardous goods may need lower limits than long-haul carriers, but the baseline remains substantial. The specific cargo you transport and your route patterns should shape your coverage strategy-and that’s where bundling multiple policies with one carrier starts to make real financial sense.

How Bundling Cuts Your Actual Trucking Costs

The Real Numbers Behind Bundled Savings

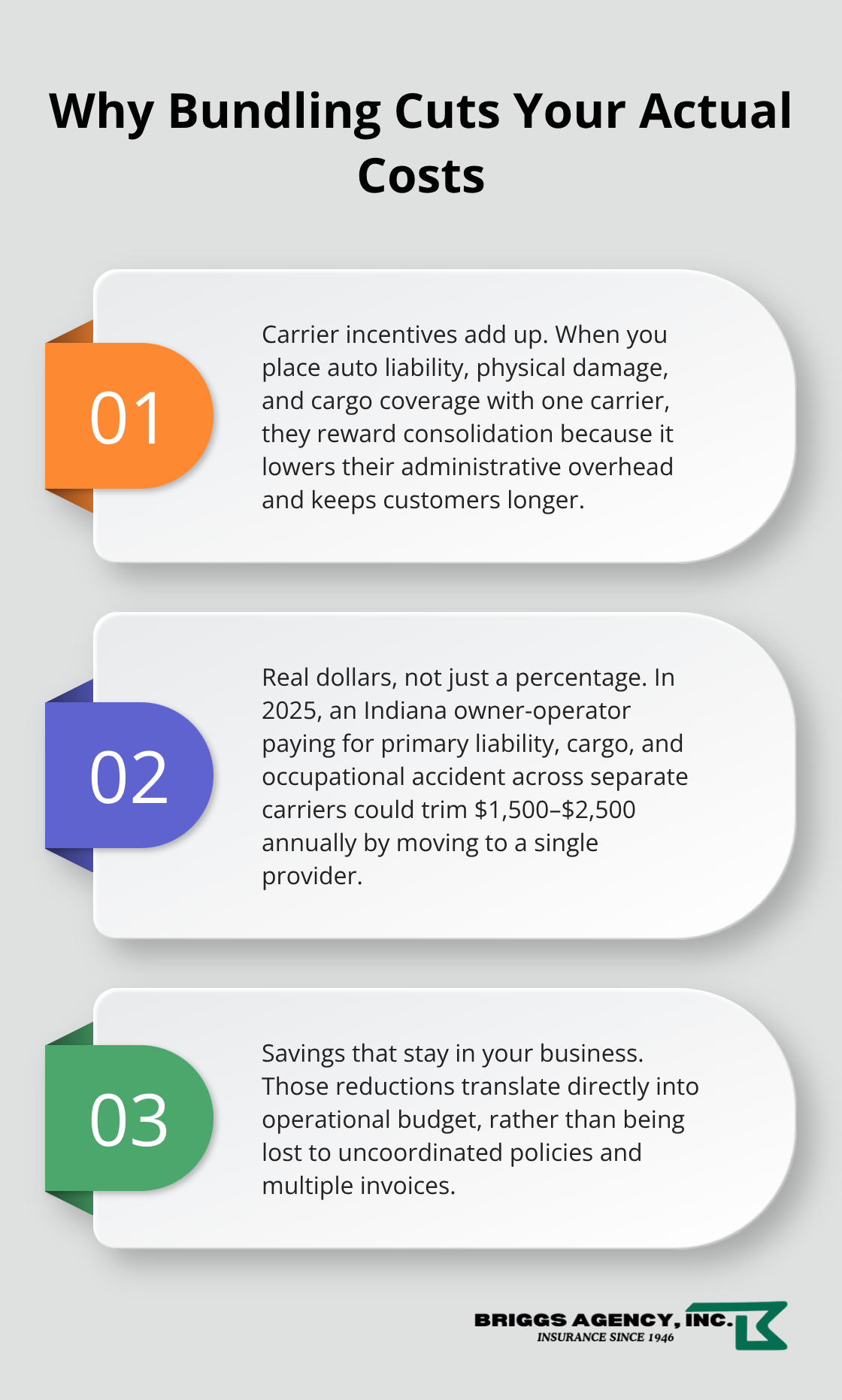

Bundling saves 10–15% on premiums according to industry standards, but the real value extends far beyond that percentage discount. When you combine auto liability, physical damage, and cargo coverage under one policy, carriers reward that consolidation because it reduces their administrative overhead and attracts customers who stay longer. In 2025, an Indiana owner-operator paying $8,000–$15,000 for primary liability, $500–$1,800 for cargo, and $600–$2,400 for occupational accident insurance across three separate carriers could easily trim $1,500–$2,500 annually by moving everything to a single provider. That’s not theoretical savings-that’s real money staying in your operational budget.

The discount compounds when you add physical damage coverage, bobtail insurance, or general liability, since each additional policy bundled often qualifies for an additional percentage reduction. Many Indiana trucking operations pay more than necessary simply because their policies sit scattered across multiple agents with no coordination between them.

Operational Simplicity That Reduces Your Workload

The second major advantage is operational simplicity that directly reduces your administrative burden. Managing policies with one agent means a single renewal date, one invoice, one point of contact for claims, and one source of truth for your coverage limits and exclusions. When a claim happens-and it will-you contact one person who understands your entire operation rather than hunting through three different policy documents and three different customer service lines.

Renewal time becomes straightforward instead of chaotic, and you avoid the common mistake of letting a policy lapse while you’re juggling paperwork from multiple carriers. Additionally, bundling forces clarity about coverage gaps that exist when policies are separate.

Closing Coverage Gaps Before They Cost You

A specialized trucking insurer can identify where your auto liability ends and your cargo coverage begins, or where your physical damage exclusions create exposure you didn’t realize. That gap-closing alone often prevents costly underinsurance situations that could cost tens of thousands when a claim occurs. Your local agent should customize your bundle around your actual operation rather than accepting a generic package designed for all trucking operations.

The specifics of what you haul, where you operate, and how your equipment is financed all shape which coverages matter most to your bottom line. This is where the conversation shifts from what you should buy to what actually protects your Indiana trucking business.

How to Build Your Indiana Trucking Bundle Step by Step

Assess What You Actually Own and Operate

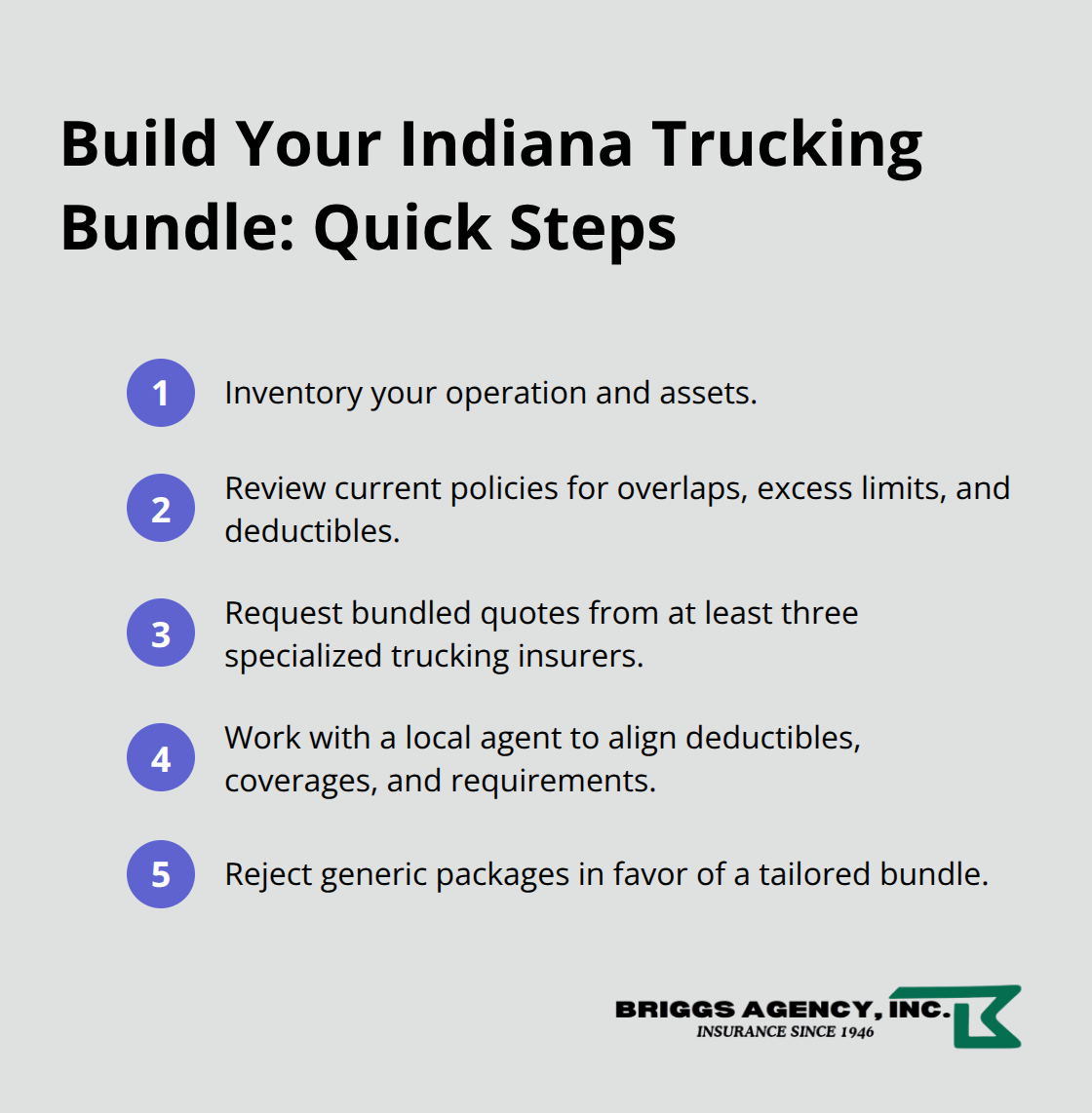

Start with a complete inventory of your operation. List your truck values, trailer worth, typical cargo types, annual mileage, whether you haul hazardous materials, and which routes dominate your schedule. This inventory becomes your baseline for coverage decisions.

An owner-operator hauling refrigerated freight across three states needs entirely different coverage than someone running local deliveries with a box truck. The specifics matter because they determine which policies genuinely protect your operation and which ones you can optimize for cost.

Review Your Current Policies for Overlaps and Excess Coverage

Pull your current policies and note the coverage limits, deductibles, and annual premiums for each. Many Indiana trucking operators pay for overlapping coverage or carry limits that far exceed their actual exposure. If you haul non-hazardous freight within a 150-mile radius, you probably don’t need the $5,000,000 hazmat liability limit that long-haul carriers require. That misalignment between your risk profile and your coverage costs you money every single year.

Request Bundled Quotes from Multiple Carriers

Contact at least three specialized trucking insurers and request quotes for bundled packages rather than individual policies. The difference in pricing can be substantial. An operator bundling $1,000,000 primary liability, $250,000 cargo coverage, and $150,000 physical damage with one carrier will typically pay significantly less than spreading those same limits across three separate providers. Request quotes that show the per-policy cost and the bundled discount separately so you see exactly where the savings come from.

Work with a Local Agent to Customize Your Package

Bring those quotes to a local agent who understands Indiana operations. A specialized trucking agent can identify which deductible levels make sense for your cash flow, whether you need bobtail coverage based on your dispatch patterns, and whether your equipment financing requires physical damage protection. The right bundle structure often saves $1,500–$2,500 annually while actually expanding coverage in critical gaps. Your agent should also confirm that your bundle complies with Indiana Department of Revenue requirements and any shipper or broker mandates you’re contractually bound to meet.

Reject Generic Packages in Favor of Customized Solutions

Never accept a generic package. The best bundle reflects your specific operation, not a template designed for all trucking businesses. Your local agent should tailor coverage around your actual needs rather than forcing you into a one-size-fits-all structure that leaves you either overinsured or exposed.

Final Thoughts

Bundling your trucking insurance coverage in Indiana delivers real savings that compound over time. An owner-operator moving from three separate policies to one bundled package typically saves $1,500–$2,500 annually while gaining the operational simplicity of a single renewal date, one invoice, and one agent who understands your entire operation. That money stays in your business instead of flowing to multiple carriers, and the administrative burden of managing separate policies disappears entirely.

Start by listing what you own and operate, then pull your current policies to identify overlaps and excess coverage you’re paying for unnecessarily. Request bundled quotes from at least three specialized trucking insurers, comparing the per-policy costs and bundled discounts side by side. The variation in pricing across carriers is substantial, and you won’t know your actual savings until you see those numbers in writing.

Work with a local agent who specializes in trucking operations and understands Indiana’s specific requirements (your agent should customize your bundle around your actual risk profile rather than forcing you into a generic package). We at Briggs Agency, Inc. have worked with Indiana trucking companies for decades, helping them build bundled packages that protect their equipment, cargo, and liability exposure while cutting unnecessary costs. Reach out to discuss your operation and get a customized quote that shows exactly where your savings hide.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.