Indiana Restaurant Liability Insurance: Shielding Your Eatery and Guests

Running a restaurant in Indiana means managing countless daily risks. From foodborne illness claims to slip-and-fall accidents, one incident can threaten your business financially and legally.

Indiana restaurant liability insurance protects you and your guests when the unexpected happens. At Briggs Agency, Inc., we help restaurant owners understand what coverage they actually need and how to get it right.

Why Restaurant Liability Insurance Protects Your Bottom Line

Foodborne Illness Claims Hit Hard

Foodborne illness claims strike Indiana restaurants with serious financial consequences. A single outbreak costs tens of thousands in medical claims, lost revenue from closure, and reputation damage that takes months to recover from. Liability insurance covers these medical expenses and legal defense costs, preventing a food poisoning incident from draining your operating capital.

Food safety protocols work hand-in-hand with your coverage. Implementing supplier approval systems, inventory controls, safe food handling training, and cross-contamination prevention lowers both your risk and your insurance premiums. This dual approach-strong operations plus solid coverage-protects your guests and your business.

Slip-and-Fall Accidents: Your Most Common Liability

Slip-and-fall accidents represent the most common premises liability claim in Indiana restaurants. A guest slips on a wet floor, falls in your restroom, or trips over an uneven surface-and suddenly you face medical bills, lost wages claims, and legal fees.

Liability coverage handles third-party bodily injury claims on your premises, including the guest’s medical payments and your defense costs if the claim goes to court. These incidents are entirely preventable with consistent floor maintenance, prompt spill cleanup, clear signage for hazards, and regular staff training on safety protocols. Your insurance protects you when prevention falls short.

Liquor Liability: A Non-Negotiable Coverage

If your restaurant serves alcohol, liquor liability coverage becomes non-negotiable. Dram shop laws vary significantly by location in Indiana, and you face heightened exposure when guests become intoxicated on your premises. This coverage protects you from claims arising from an intoxicated patron’s actions or injuries, covering both third-party bodily injury and your legal defense.

Without liquor liability protection, a single altercation involving an intoxicated guest could exhaust your general liability limits and leave you personally liable for damages. The financial and legal stakes are simply too high to skip this coverage.

Understanding these three core liability exposures-foodborne illness, slip-and-falls, and alcohol-related incidents-shapes the foundation of your restaurant’s protection strategy. Each risk demands specific coverage, and each coverage type addresses real claims that happen in Indiana restaurants every year. The next step is determining exactly which coverages fit your operation and how much protection you actually need.

What Your Restaurant Liability Insurance Actually Covers

Three Core Protection Components

Restaurant liability insurance protects against three main financial exposures when incidents happen on your premises. Bodily injury and property damage coverage pays for a guest’s medical expenses, lost wages, and pain-and-suffering claims if they suffer injury at your restaurant or damage their property while there. Medical payments coverage steps in quickly to cover immediate medical bills without requiring the injured person to prove fault, which often resolves minor incidents before they become lawsuits. Your policy also covers legal defense costs-attorney fees, court costs, and expert witness fees. Indiana courts allow plaintiffs to pursue non-economic damages for pain and suffering, so having adequate legal representation protects both your finances and your ability to defend your operations in court.

Coverage Limits That Match Your Operation

The coverage limits you choose directly impact your protection level and your premium cost. General liability policies typically start at $1 million per occurrence for bodily injury and property damage, though restaurants serving alcohol often carry $2 million limits to account for higher exposure from intoxicated patron claims. Medical payments coverage usually ranges from $1,000 to $10,000 per person and covers treatment costs regardless of fault, making it a practical tool for keeping minor incidents out of the courtroom.

Selecting limits that match your restaurant’s size, seating capacity, alcohol service volume, and equipment value matters far more than picking the cheapest option available. An undersized policy leaves you exposed to personal liability; an oversized policy wastes premium dollars on coverage you don’t need.

How Claims Actually Work

When you file a claim, your insurance company assigns a claims adjuster to investigate, gather evidence, and manage negotiations with the injured party’s attorney. This process typically takes weeks to months depending on claim complexity, but having professional representation from your insurer protects you from making damaging statements or admissions that could increase your liability. The adjuster handles communication with the other party’s legal team, preserves evidence, and works toward settlement or court defense.

Understanding what happens after an incident occurs helps you respond appropriately when it matters most. Your next decision-choosing the right carrier and agent-determines whether you get responsive claims support and coverage that actually fits your restaurant’s unique risks.

Picking Coverage That Fits Your Restaurant

Assess Your Specific Risks and Operations

Start with your operation’s actual risk profile instead of guessing what coverage you need. A pizzeria with a wood-fired oven and delivery fleet faces different exposures than a fine-dining establishment with a full bar and valet parking. Walk through your restaurant systematically: count your employees and their roles, identify which areas see the most guest traffic, assess whether you serve alcohol and how much revenue comes from liquor sales, evaluate your kitchen equipment and its replacement value, and note any unique hazards like open flames or raw bars.

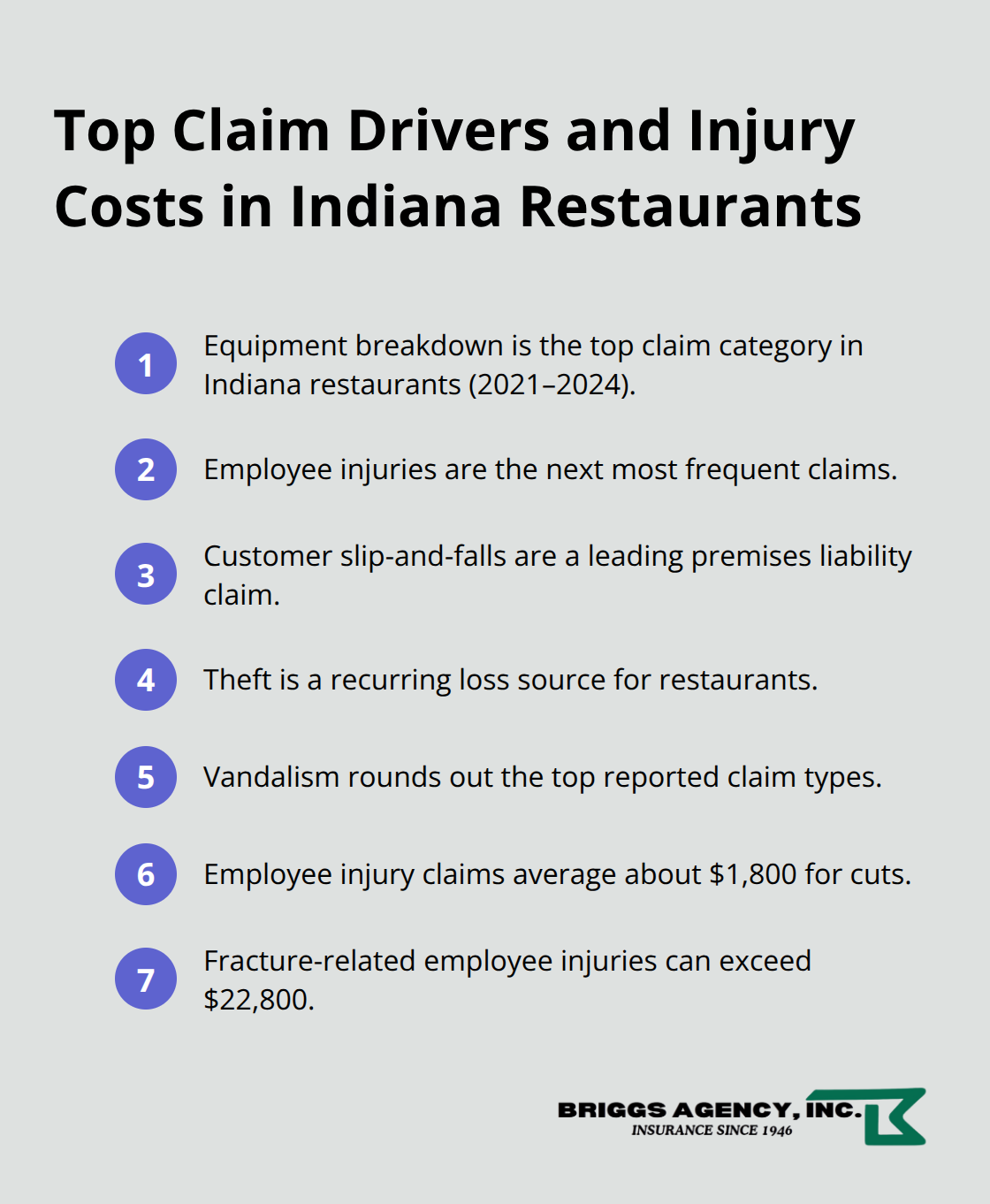

OysterLink data from Indiana restaurants between January 2021 and July 2024 shows that equipment breakdown ranks as the top claim category, followed closely by employee injuries, customer slip-and-falls, theft, and vandalism. This means property coverage protecting your refrigeration and cooking equipment deserves serious attention, not an afterthought. Employee injury claims average around $1,800 for cuts but can exceed $22,800 for fractures, making workers’ compensation non-negotiable.

Once you understand your specific exposures, you can request quotes that address them directly instead of accepting generic packages that either over-insure or leave gaps.

Compare Quotes from Multiple Carriers

Comparing quotes requires looking past price alone, which is where most restaurant owners stumble. Indiana general liability insurance averages $142 per month, and a complete package combining general liability, workers’ compensation, and property coverage runs roughly $359 monthly for a small two-employee operation according to industry data. Bundling multiple coverages typically saves 20 to 30 percent compared to buying policies separately, so always ask carriers about package discounts.

However, the cheapest quote often excludes critical coverages or carries high deductibles that hurt when claims happen. Compare three to five quotes side by side using the same coverage limits, deductibles, and endorsements, then evaluate what each carrier actually covers. Some insurers exclude food spoilage from equipment breakdown claims unless you add an endorsement; others include it automatically. Liquor liability limits, cyber liability options, and business interruption coverage vary significantly between carriers.

Work with a Local Agent

An independent agent gives you access to multiple carriers’ quotes without shopping around yourself, saving hours while ensuring you see all viable options. Local agents understand Indiana’s specific liability landscape, neighborhood crime patterns, and which carriers respond fastest to claims in our state. Before meeting with an agent, assess what kind of coverage you’re seeking so your conversation stays focused and productive. At Briggs Agency, Inc., our experienced local agents represent multiple top-rated carriers and compare options to tailor policies that deliver competitive pricing and the right protection for your restaurant’s unique needs.

Final Thoughts

Restaurant liability insurance protects your business from financial devastation when incidents happen. The three core exposures-foodborne illness, slip-and-fall accidents, and liquor liability-account for the majority of claims Indiana restaurants face each year. Indiana restaurant liability insurance works best when it matches your actual operation, not a generic package designed for every restaurant equally.

Your next step is straightforward: assess your specific risks, gather quotes from at least three carriers, and review coverage options side by side. Look past price alone, since a policy that costs $50 less monthly but excludes food spoilage or carries inadequate liquor liability limits creates dangerous gaps when claims arrive. An independent agent who understands Indiana’s liability landscape, knows which carriers respond fastest to claims in our state, and represents multiple top-rated insurers saves you time while ensuring you see all viable options.

At Briggs Agency, Inc., our experienced local agents compare coverage options to deliver competitive pricing and the right protection for your restaurant’s unique needs. Contact us to discuss your restaurant’s coverage today and reduce risk while safeguarding what you’ve built.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.