Truckers Liability Insurance Indiana: What It Covers for Drivers

Running a trucking operation in Indiana means understanding your legal obligations and protecting your business from financial risk. Truckers liability insurance Indiana is more than a legal requirement-it’s your safeguard against costly claims that could shut down your operation.

At Briggs Agency, Inc., we help drivers and fleet owners navigate the coverage options that actually matter for their routes and cargo. This guide breaks down what you need to know to make informed decisions about your protection.

What Truckers Liability Insurance Actually Covers

The Foundation of Your Legal Protection

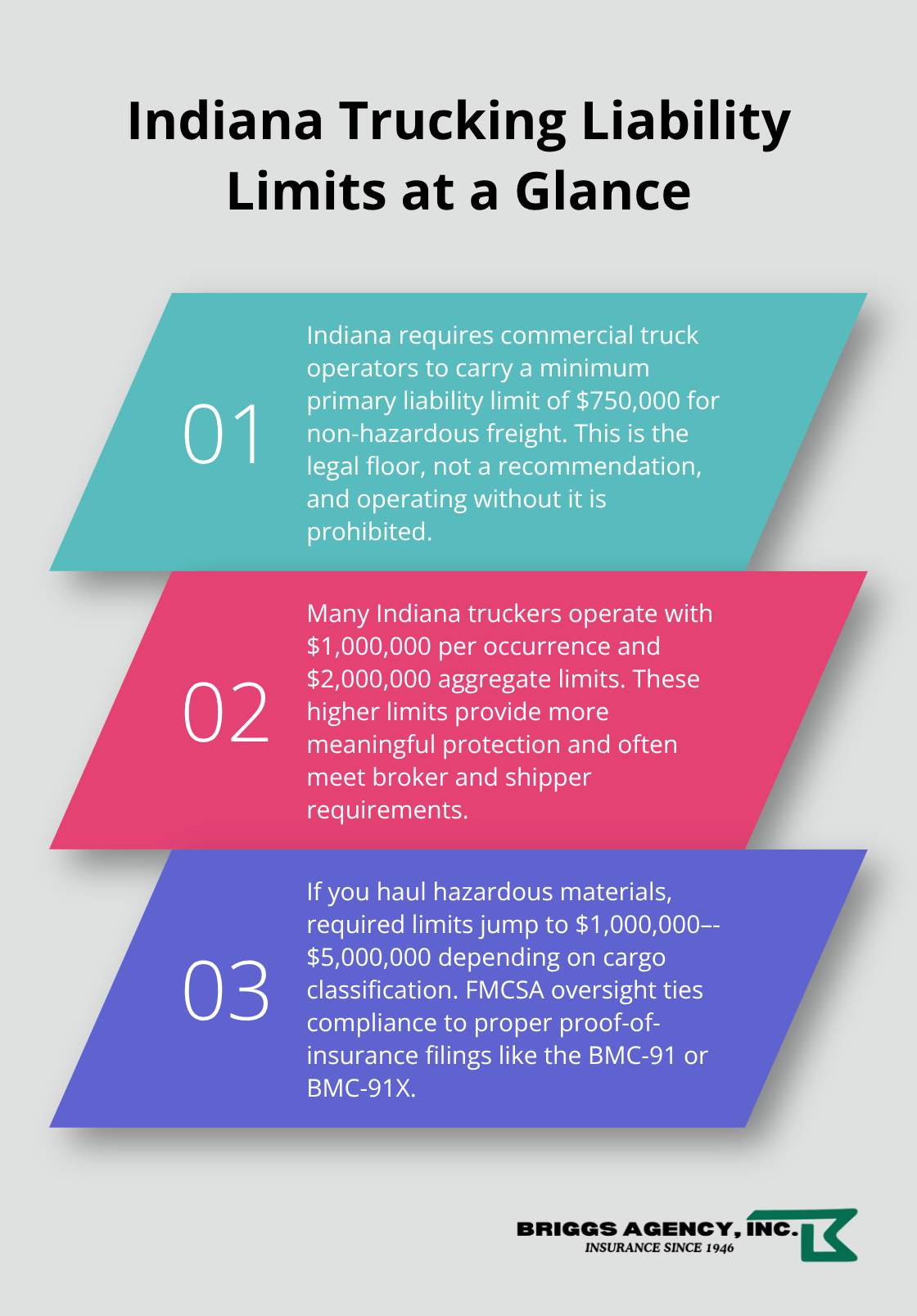

Truckers liability insurance protects you when you cause bodily injury or property damage to someone else while operating your truck. This coverage activates when you’re at fault in an accident-it pays for the other person’s medical bills, lost wages, pain and suffering, and repairs to their vehicle or property. Indiana law requires all commercial truck operators to carry minimum primary liability coverage of $750,000 for non-hazardous freight. If you haul hazardous materials, that requirement jumps to $1,000,000 to $5,000,000 depending on your cargo type. Without this coverage, you cannot legally operate, and the FMCSA will suspend or revoke your operating authority if you fail to maintain proof of insurance through the required BMC-91 or BMC-91X filings.

Why Minimum Coverage Often Falls Short

The real question isn’t whether you need liability insurance-it’s whether the minimum coverage is enough for your actual operation. Many Indiana truckers operate with $1,000,000 per occurrence and $2,000,000 aggregate limits, which provides substantially more protection than the state minimum and often satisfies broker and shipper requirements. Your cargo type, routes, and vehicle size all affect your risk exposure. A hazmat hauler operating interstate faces far greater liability exposure than a local delivery driver, and your insurance should reflect that reality.

Tailoring Coverage to Your Operation

Your specific routes, cargo, and business model determine what coverage actually protects you. A family-owned, independent agency like Briggs Agency, Inc. (serving Crown Point and the surrounding area since 1946) represents multiple top-rated carriers, which means their experienced local agents can compare options and tailor policies to your needs rather than settling for the bare legal minimum that leaves you exposed. The difference between minimum coverage and adequate coverage often comes down to understanding your actual liability exposure-something a local agent who knows Indiana trucking operations can help you identify.

What Bodily Injury and Property Damage Liability Actually Covers

How These Two Components Protect You

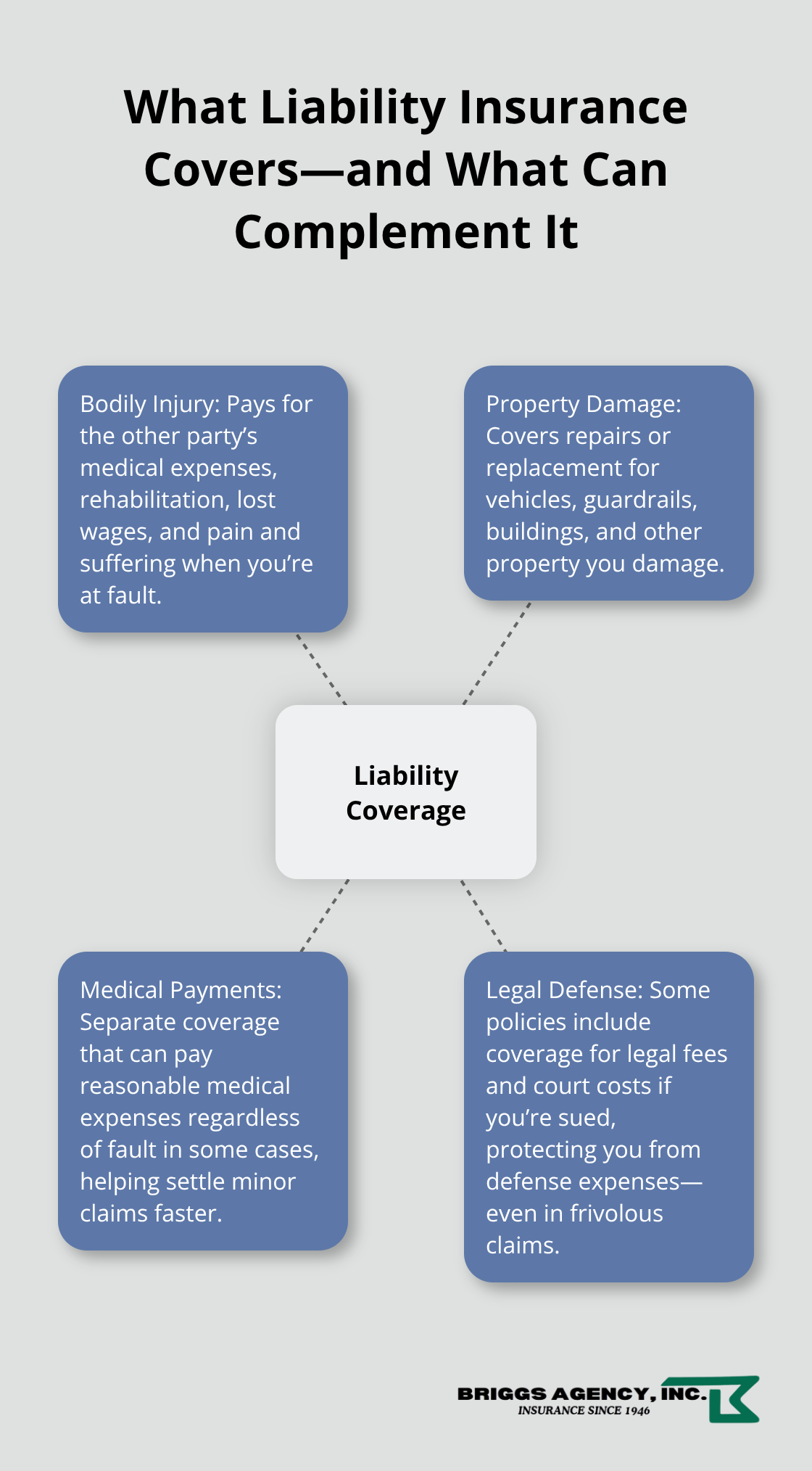

Bodily injury and property damage liability coverage pays for costs when you cause an accident that injures someone or damages their property. Bodily injury liability covers the other driver’s medical expenses, rehabilitation costs, lost wages, and pain and suffering claims. Property damage liability covers repairs or replacement of the other person’s vehicle, guardrails, buildings, or any other property your truck damaged. Indiana requires you to carry both components as the foundation of your legal protection.

Why Minimum Coverage Leaves You Exposed

The state minimum of $750,000 for non-hazardous freight sounds substantial until you face a serious accident involving multiple vehicles or injuries. A single multi-vehicle crash easily exceeds $2 million in damages when you factor in medical treatment, lost income, and long-term care for seriously injured parties. Many Indiana truckers choose $1,000,000 per occurrence with $2,000,000 aggregate limits instead of the minimum, which provides meaningful cushion against catastrophic claims that could otherwise wipe out your business.

How Your Cargo and Routes Affect Your Liability Exposure

Your actual liability exposure depends on what you haul and where you drive. Hazmat carriers operating interstate face significantly higher risk and must carry $1,000,000 to $5,000,000 in coverage depending on cargo classification. Even within general freight, your routes matter: a driver regularly traveling I-94 through dense Chicago traffic faces different exposure than someone making local deliveries in rural areas.

Additional Protections That Work Alongside Liability

Medical payments coverage, separate from liability, covers reasonable medical expenses for injured parties regardless of fault in some cases, which helps settle minor claims faster and keeps your rates stable. Some policies also include coverage for legal fees and court costs if you’re sued, protecting your business from the expense of defending yourself even in frivolous claims. An experienced local agent who understands Indiana trucking operations will assess your specific cargo types, annual mileage, interstate movements, and growth plans to recommend coverage that matches your actual risk rather than leaving you underprotected or overpaying for unnecessary limits.

Matching Your Coverage to Your Actual Risk

Start With Your Cargo and Routes

Your cargo and routes determine whether the state minimum protects you or leaves you exposed. If you haul hazardous materials, your decision is straightforward: Indiana and federal law require $1,000,000 to $5,000,000 depending on your cargo classification, so you need coverage that meets those mandates. For general freight, the calculation becomes more specific. A local delivery driver making short runs in rural areas faces different exposure than someone regularly driving I-94 through congested Chicago traffic or crossing state lines frequently.

Document your typical routes, the weight and type of cargo you carry, and your annual mileage. This information directly affects your liability risk and the coverage limits you actually need. Many Indiana truckers operating general freight settle on $1,000,000 per occurrence with $2,000,000 aggregate limits rather than the $750,000 state minimum, which gives them real cushion without overextending costs.

Check Your Client Contracts

Some brokers and shippers now require higher limits as a condition of business, so checking your client contracts matters. If you work with multiple brokers or shippers, you might find they request different coverage amounts. Understanding those requirements upfront prevents delays when you need to activate loads.

Request Quotes From Multiple Carriers

Different carriers price trucking risk differently based on their loss history, underwriting approach, and appetite for specific cargo types or routes. One carrier might offer aggressive pricing on general freight but charge significantly more for hazmat operations, while another does the opposite. Request quotes from at least three carriers and ask them to evaluate the same coverage limits so you can compare actual prices rather than different protection levels.

When you contact insurers, provide your driving record, driver certifications and training, specific areas where you operate, materials you haul, annual miles, and any interstate movements. This detail allows them to give accurate quotes instead of rough estimates that shift later. Carriers also evaluate your growth plans, so mentioning expansion helps them structure policies that scale with your business rather than forcing you to renegotiate annually.

Work With an Agency That Represents Multiple Carriers

A local agency represents multiple top-rated carriers and handles the comparison work for you, pulling quotes and evaluating options based on your specific operation rather than steering you toward one solution. They also manage your FMCSA filings and financial proof of responsibility documentation, which saves you time navigating regulatory requirements.

Final Thoughts

Truckers liability insurance in Indiana protects your operation from financial devastation when accidents happen. The state minimum of $750,000 for non-hazardous freight meets legal requirements, but your actual coverage should match your cargo type, routes, and business model. Hazmat carriers need $1,000,000 to $5,000,000 depending on cargo classification, while general freight operators often find that $1,000,000 per occurrence with $2,000,000 aggregate limits provides meaningful protection without unnecessary expense.

Finding adequate protection starts with documenting your operation-write down your typical routes, cargo types, annual mileage, and any interstate movements. Request quotes from multiple carriers and ask them to evaluate identical coverage limits so you can compare actual prices, since different carriers price trucking risk differently based on their underwriting approach and loss history. Your brokers and shippers may also require specific coverage amounts, so reviewing client contracts prevents delays when you need to activate loads.

A local agency that represents multiple top-rated carriers saves time and delivers better results than handling this work alone. Briggs Agency, Inc. handles the comparison work, pulls quotes based on your specific operation, and manages your FMCSA filings and financial proof of responsibility documentation. Contact us to discuss your truckers liability insurance Indiana requirements and get quotes from carriers that match your operation.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.