Crown Point Trucking Insurance: Fleet Protection for Local Carriers

Running a trucking operation in Crown Point means managing risks that go far beyond standard business insurance. Your fleet faces unique exposures-from cargo liability to regulatory compliance-that require specialized protection.

At Briggs Agency, Inc., we work with local carriers every day and understand exactly what coverage gaps can cost your business. This guide walks you through the trucking insurance options that actually matter for your operation.

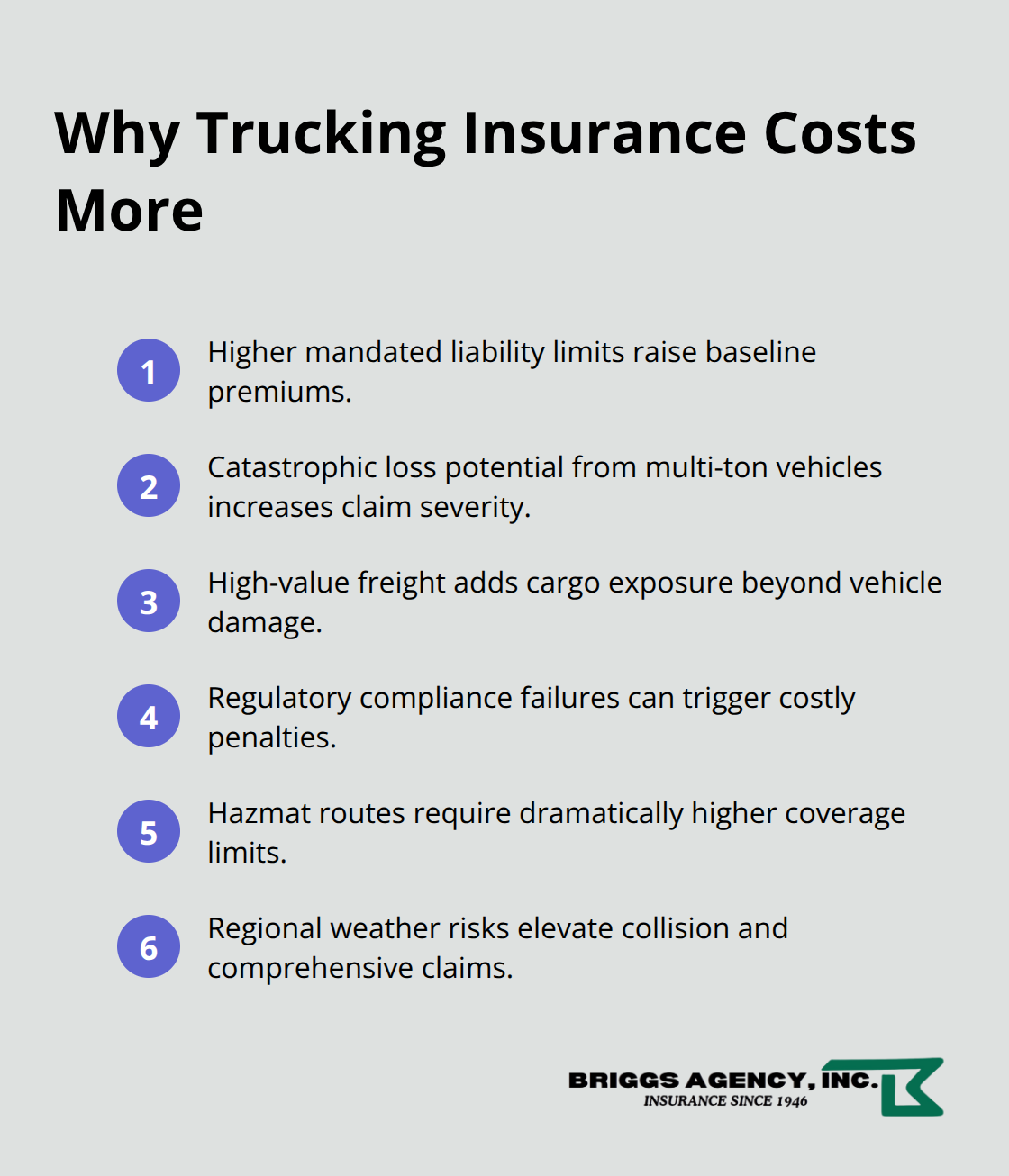

Why Trucking Insurance Costs More Than Standard Auto Coverage

Trucking insurance operates in a completely different risk universe than standard commercial auto policies. Indiana minimum liability for commercial trucking is $750,000 for non-hazardous freight, with requirements jumping to $5,000,000 for hazmat shipments according to FMCSA standards. That’s not a minor difference-it reflects the genuine catastrophic exposure your operation faces. A single accident involving a loaded truck can generate six-figure claims that would bankrupt a business relying on basic auto coverage.

Standard commercial policies simply don’t account for the scale of damage a multi-ton vehicle can inflict, the value of freight you’re transporting, or the regulatory penalties that follow a compliance failure.

Cargo and Equipment Require Separate Protection

Your freight isn’t covered under vehicle damage policies. Motor truck cargo coverage protects you when goods are damaged, spoiled, or lost during transport-and this matters far more than most owner-operators realize. Temperature-controlled cargo creates an especially tricky exposure: if your refrigeration fails mid-route and spoils a load of perishables worth $50,000, standard physical damage coverage won’t touch it. You need specific provisions that cover spoilage losses tied to equipment failure. Likewise, service trucks carrying expensive tools, diagnostic equipment, or specialized aftermarket gear need riders that cover these assets separately. A deductible of $500 to $1,000 works for vehicle collision, but your equipment and cargo exposures demand different thresholds based on actual shipment values and tool inventory.

Regulatory Compliance Creates Non-Negotiable Coverage Demands

The FMCSA requires proof of insurance via forms BMC-91 or BMC-91X before you legally operate as a for-hire carrier. A lapsed policy doesn’t just cost you money-it revokes your operating authority and triggers Indiana BMV fines and registration issues. Coverage gaps can strand your fleet while you sort paperwork. Hazmat shipments demand environmental cleanup cost coverage and regulatory fine protection that standard policies exclude entirely. Indiana’s winter weather (ice, hail, thunderstorms) increases collision risk and liability claims dramatically, especially for operations running heavy truck traffic through Lake County corridors. Your policy must account for these seasonal and geographic realities, not just generic national averages.

Protect Against Underinsured Drivers and Employee Vehicle Use

Uninsured or underinsured motorist coverage becomes critical when another driver causes a six-figure accident and carries minimal coverage. Without this layer, you absorb the gap out of pocket. Non-owned and hired vehicle liability protects your operation when employees use personal or rental vehicles for business purposes-a coverage most standard policies handle poorly or exclude entirely. These gaps expose your business to significant financial risk that extends well beyond your own fleet.

Understanding these distinct coverage layers sets the foundation for selecting the right protection. The next section walks you through the specific coverage options that address these exposures and help you build a policy tailored to your Crown Point operation.

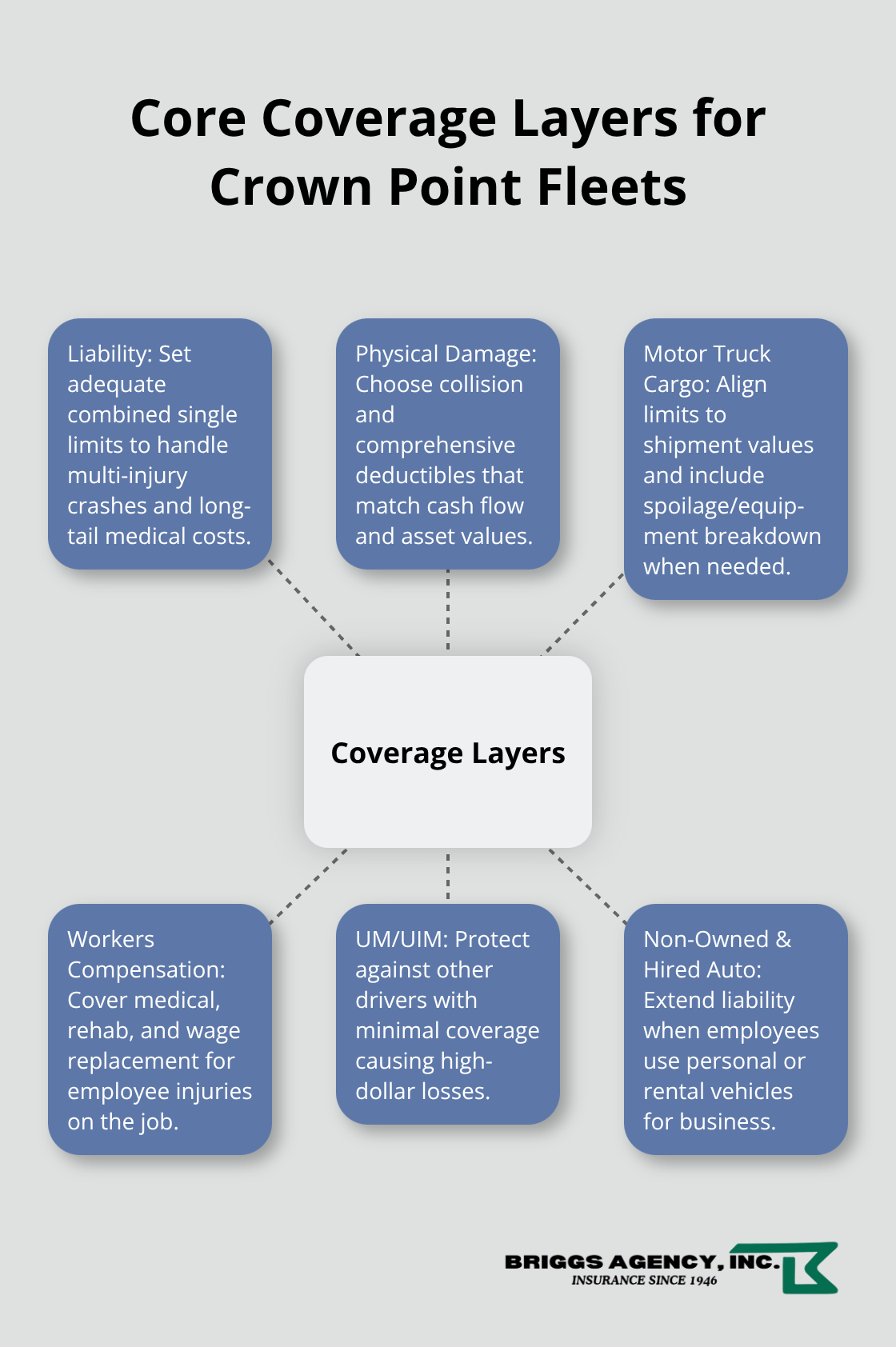

The Coverage Layers That Keep Crown Point Fleets Protected

Liability Coverage Forms Your Foundation

Liability coverage forms the foundation of any trucking operation, and the numbers matter more than most carriers realize. Indiana minimum liability sits at $750,000 for non-hazardous freight, but that floor leaves you dangerously exposed. A single accident involving your truck striking a passenger vehicle can easily generate $2 million in bodily injury claims when multiple people are injured, medical care extends over years, and lost wages accumulate. Many Crown Point carriers operate with $1 million in combined single-limit liability, which provides meaningful protection without excessive premium burden.

The real gap appears when you factor in uninsured or underinsured motorist coverage. If another driver causes a crash and carries only Indiana’s minimum $25,000 in liability, your uninsured motorist layer absorbs the difference, protecting your operation from absorbing six figures out of pocket. Without this coverage, you self-insure against other people’s inadequate policies.

Physical Damage Coverage Protects Your Assets

Physical damage coverage protects your actual assets-trucks, trailers, and cargo-and requires honest assessment of what you transport and what your vehicles are worth. Collision coverage typically carries deductibles between $500 and $2,500; choosing the right deductible involves calculating your cash flow tolerance against premium savings. A $1,000 deductible represents a practical middle ground for most fleet operations.

Comprehensive coverage handles theft, weather damage (critical during Indiana’s harsh winters), vandalism, and animal strikes. Many carriers underestimate exposure here-a severe hailstorm can damage an entire fleet in minutes, and comprehensive coverage absorbs those costs while collision does not.

Motor Truck Cargo Coverage Matches Your Shipments

Motor truck cargo coverage specifically protects the freight you transport, and this is where operational details become essential. Temperature-controlled loads demand explicit spoilage protection if refrigeration fails; standard cargo policies won’t cover product loss from equipment breakdown. High-value shipments require cargo limits matching actual values with roughly a 20 percent cushion for growth and contingencies.

Service vehicles carrying diagnostic tools, specialized equipment, or aftermarket gear need equipment riders covering these assets separately from vehicle damage. Align deductibles to your inventory value rather than your vehicle collision deductible.

Workers Compensation Covers Your Team

Workers compensation protects employees injured on the job and covers medical expenses, rehabilitation, and wage replacement. Indiana requires this coverage for any business with employees. Strong workers comp coverage reduces your exposure when a driver sustains a back injury loading freight or suffers an accident-related injury.

Premium calculations tie directly to your payroll and job classification. Owner-operators with no employees can exclude themselves, but this decision should align with actual operational structure and growth plans. The specific coverage you select-liability limits, deductibles, cargo protection, and workers comp-directly shapes your ability to operate safely and profitably in Crown Point’s competitive transportation market. Selecting the right combination requires understanding not just what regulations demand, but what your actual operation exposes you to each day.

Finding the Right Trucking Insurance Partner

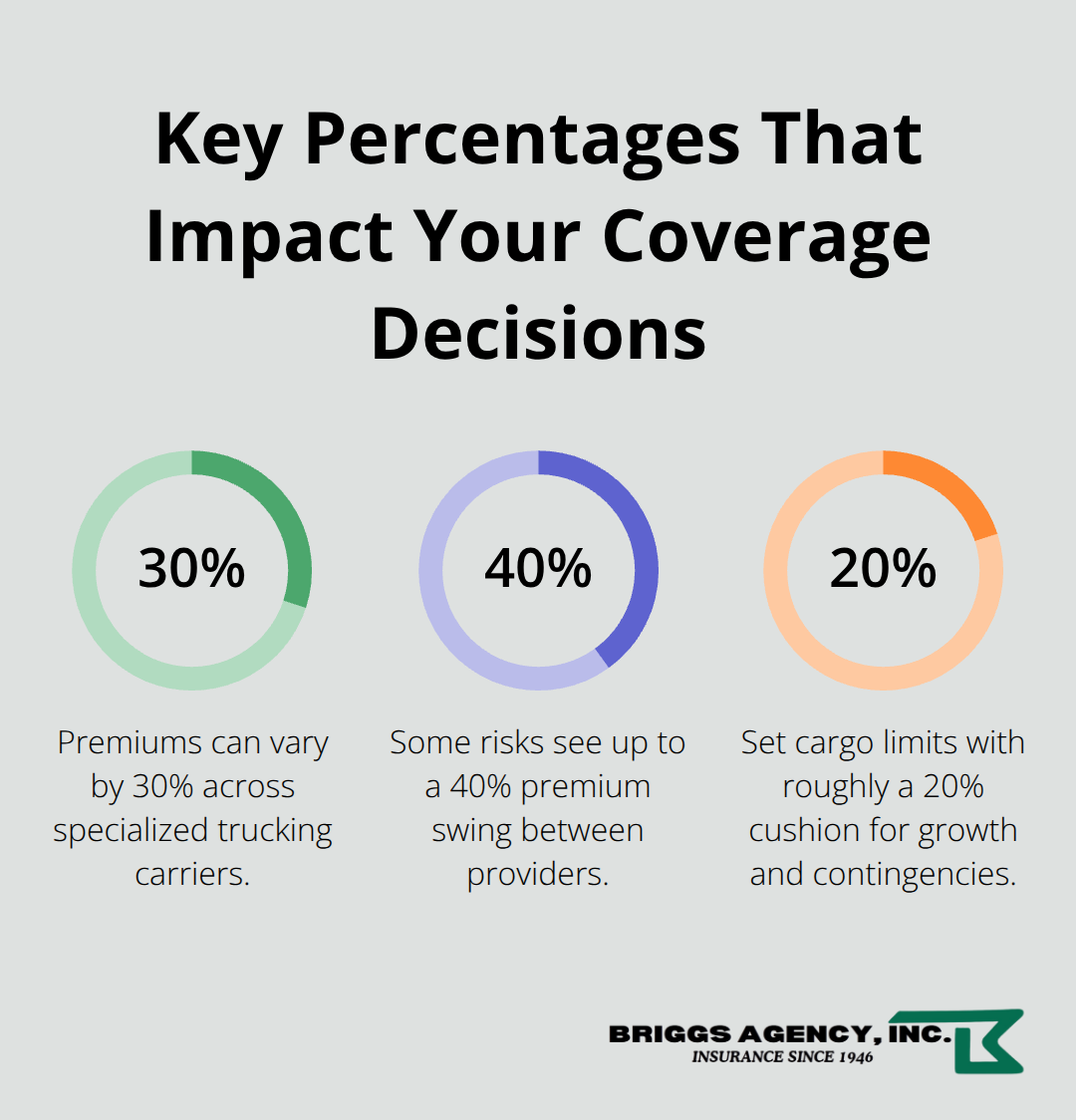

Selecting a trucking insurance provider in Crown Point requires moving beyond premium quotes and actually examining what coverage you receive and how an agency will support your operation when claims happen. Most carriers focus on price, but the cheapest quote often reflects the weakest protection. Commercial auto insurance for light-duty vehicles typically costs $250 to $400 per month, though this varies dramatically based on your safety record, driver experience, cargo type, and whether you operate hazmat routes. A quote $2,000 below market should trigger questions about what coverage limits or protections were cut to hit that number. The real cost of underinsurance emerges when a claim exceeds your limits and you’re writing checks out of pocket.

Shop Multiple Carriers for True Price Comparison

Obtain quotes from at least three specialized trucking carriers to account for the 30 to 40 percent premium variation across providers and to identify which carriers actually understand Crown Point operations versus those applying generic national pricing. Generic policies miss local exposures entirely-Lake County’s heavy truck traffic, winter weather patterns, and warehouse district concentrations create distinct risks that local brokers recognize while national carriers often ignore. An independent agent representing 15 or more A-rated carriers can shop your risk across Travelers, Liberty Mutual, Progressive, Cincinnati, Auto-Owners, Western Reserve Group, AmTrust, and Hartford simultaneously, comparing not just premiums but actual coverage structures side-by-side.

Conduct Thorough Discovery Before Accepting Quotes

The agent you select should conduct detailed discovery before quoting, asking specific questions about your vehicles, drivers, routes, and loss history over the past five years. This process takes time-don’t trust anyone who quotes within minutes of a phone call. Strong underwriting relies on tools like CAB reports to understand your safety history and identify necessary follow-up actions.

Verify Claims Support and Operational Competence

Claims handling separates good agencies from mediocre ones; request references and ask how quickly the agency secures proof of insurance for new contracts-same-day certificate issuance within hours after binding demonstrates operational competence. Verify that your agent monitors BMC-91 filings actively to prevent accidental authority loss and can coordinate additional insured language when customers demand it.

Partner with Local Expertise

An independent agency in Crown Point understands the specific exposures your operation faces daily rather than applying national averages that miss what matters in your market. Local agents translate trucking regulations into practical coverage that protects your fleet against the risks you actually encounter on Lake County roads and beyond.

Final Thoughts

Protecting your Crown Point trucking operation requires more than finding the cheapest policy-the coverage decisions you make today determine whether a single accident drains your business or whether your fleet continues operating safely and profitably. Liability limits, cargo protection, physical damage deductibles, and workers compensation all work together to create a safety net that reflects your actual operational exposures rather than regulatory minimums alone. Lake County’s heavy truck traffic, winter weather patterns, and warehouse district concentrations create specific risks that national carriers miss entirely.

An independent agent representing multiple A-rated carriers can compare coverage structures side-by-side, identify gaps that standard policies leave open, and tailor protection that matches what your operation genuinely needs. This process takes time and detailed discovery, but it prevents the costly mistakes that emerge when claims exceed your limits or coverage gaps leave you exposed. Crown Point trucking insurance isn’t generic-local expertise matters because your risks differ from operations in other markets.

Contact Briggs Agency, Inc. to discuss your specific operation and receive quotes that reflect your actual exposures. We’ll conduct thorough discovery, shop your risk across carriers, and help you build a policy that keeps your fleet protected and compliant. Your business deserves protection tailored to Crown Point’s unique transportation landscape, not national averages that miss what matters in your market.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.