Logistics Fleet Insurance: Keeping Your Deliveries on Track

Your delivery fleet faces real risks every day. Vehicle accidents, cargo damage, and unexpected downtime can drain your budget fast. At Briggs Agency, Inc., we help logistics companies protect their operations with the right fleet insurance coverage.

This guide walks you through what you need to know to keep your business running smoothly.

What Fleet Insurance Covers and Why It Matters

Core Coverage Types for Logistics Operations

Fleet insurance protects your delivery operation from the financial devastation that accidents, cargo loss, and vehicle downtime create. Unlike standard commercial auto policies, fleet coverage bundles liability, physical damage, cargo protection, and workers’ compensation into one package designed for the realities of logistics work. Commercial auto liability covers third-party injuries and property damage when your driver is at fault-this is mandatory for interstate operations under Federal Motor Carrier Safety Administration rules, with minimum requirements varying depending on entity type and operating authority. Physical damage coverage pays for repairs or replacement of your vehicles after collision or comprehensive losses like theft or weather damage. Cargo insurance protects the goods you’re transporting from loss or damage in transit, which becomes critical when you’re hauling electronics, perishables, or time-sensitive medical shipments.

Additional Protections Your Fleet Needs

Workers’ compensation covers your employees’ medical expenses and lost wages if they suffer injury on the job, and it’s legally required in nearly every state. Many logistics operations also need hired and non-owned auto coverage when contractors use personal vehicles for deliveries, and general liability protects against slip-and-fall claims at delivery locations. These protections work together to shield your business from multiple angles of exposure that standard policies simply don’t address.

The Real Cost of Inadequate Coverage

A single accident involving your delivery vehicle can result in a lawsuit exceeding $25 million in median damages, according to nuclear verdict data showing awards have risen roughly 33% over the past decade. Fleet insurance premiums have climbed approximately 40% over the last decade, with current trucking insurance averaging over $10 per mile in 2024. Downtime from vehicle repairs drains revenue immediately-a truck sitting idle costs far more than the repair bill itself when you factor in missed deliveries and lost customer trust.

Regulatory Consequences of Operating Uninsured

Regulatory violations compound the problem; operating without proper coverage can suspend your FMCSA authority within 24 to 48 hours, shutting down your entire operation. This isn’t a minor inconvenience-it’s a complete halt to your business. The stakes demand that you understand your insurance to match your coverage to your actual operations, not guess at what you might need.

Finding the Right Coverage for Your Operation

An independent agent who understands logistics operations can compare quotes from multiple carriers and help you right-size coverage to match your specific routes, vehicle types, and cargo risks, ensuring you’re protected without overpaying for unnecessary limits. The next section explores how to evaluate providers and make this critical decision with confidence.

Essential Coverage for Your Delivery Operation

Commercial Auto Liability and Physical Damage

Commercial auto liability is non-negotiable for any logistics business operating across state lines. The Federal Motor Carrier Safety Administration requires minimum liability coverage that varies depending on your entity type and operating classification. Physical damage coverage protects your vehicles from collision and comprehensive losses, but here’s what matters operationally: a single repair bill for a delivery truck can easily reach $5,000 to $15,000, and that’s before you account for the revenue lost while the vehicle sits in the shop.

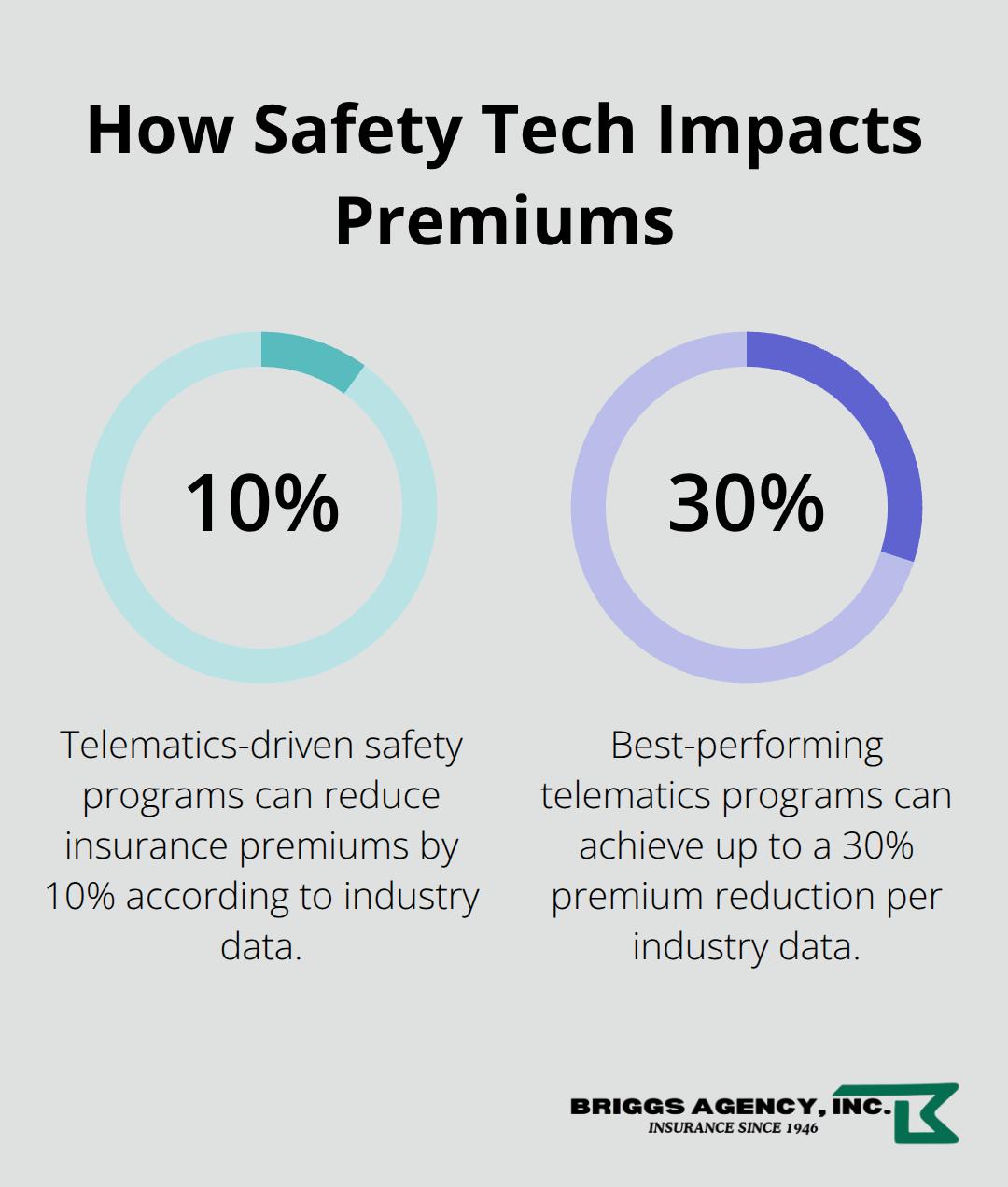

Telematics systems that monitor hard braking, rapid acceleration, and following distance can reduce your insurance premiums by 10% to 30% according to industry data, so insurers now actively reward fleets that implement these safety tools. These systems give you real-time visibility into driver behavior and vehicle health, which translates directly into lower claims and better rates.

Workers’ Compensation and Contractor Coverage

Workers’ compensation is mandatory in nearly every state and covers employee medical expenses and lost wages from job-related injuries. The coverage becomes especially important when your team handles heavy packages or works in challenging weather conditions that increase accident risk. Hired and non-owned auto coverage protects you when contractors or employees use their personal vehicles for deliveries, which is common in last-mile operations where independent drivers handle final-leg delivery to customer doors.

This coverage fills a critical gap because your standard commercial policy typically excludes vehicles you don’t own, leaving you exposed if a contractor’s vehicle is involved in an accident while making a delivery on your behalf. Without this protection, a single incident can create significant liability exposure.

Cargo and General Liability Protection

Cargo insurance protects the actual goods in transit from loss, damage, or theft, and becomes essential when you move high-value electronics, temperature-sensitive perishables, or time-critical medical shipments. General liability rounds out your protection by covering slip-and-fall claims at delivery locations, property damage to customer facilities, and third-party bodily injury claims that fall outside vehicle-related incidents.

The cost of these coverages varies based on your fleet size, vehicle types, delivery routes, driver safety records, and cargo value. An independent agent who understands logistics operations allows you to right-size coverage to your actual risk profile rather than paying for unnecessary limits or discovering gaps when a claim occurs.

Navigating State-Specific Requirements

State-specific requirements add complexity to your coverage strategy. California imposes stricter workers’ compensation mandates, Texas requires specific intrastate cargo coverage, and New York mandates supplementary uninsured motorist protection. If your deliveries cross state lines, multi-state coverage strategies matter significantly to your compliance and protection.

An agent experienced in logistics can ensure your policy meets all applicable FMCSA filings and state regulations while positioning your coverage to support growth without constant policy adjustments. The next section explores how to evaluate insurance providers and select a partner who understands your operation’s specific needs.

Selecting a Fleet Insurance Partner Who Understands Logistics

Why Logistics Expertise Matters in Your Insurance Choice

Picking the right insurance provider matters more than most logistics owners realize. A general commercial agent who handles restaurants and contractors won’t understand the specific exposures in last-mile delivery, the impact of telematics on your rates, or how state-by-state regulations affect your coverage strategy. You need an agent who grasps that a 10-minute pre-trip inspection can keep trucks off the DOT roadside inspection list, where nearly one in five trucks face pulls, and who knows how cargo securement violations under 49 CFR 393 create both regulatory and insurance risk. The difference between a generalist and a specialist appears immediately: a specialist asks about your specific routes, vehicle types, driver experience, and loss history before recommending coverage limits, while a generalist plugs numbers into a form and sends you a quote.

Comparing Quotes Across Multiple Carriers

An independent agent representing multiple top-rated carriers can compare quotes across different underwriters, but not all agents possess equal expertise in logistics. This matters because a fleet transporting temperature-sensitive pharmaceuticals faces entirely different cargo risks than one delivering packages, and your coverage should reflect that distinction. When you request quotes, ask each agent whether they understand FMCSA filing requirements and can confirm that your BMC-91 certificate posts within 24 to 48 hours of binding coverage, since gaps in authority suspension can halt your entire operation.

Evaluating Claims Support and Responsiveness

The claims experience separates adequate providers from true partners in your business. When a driver causes an accident involving a $25 million nuclear verdict scenario, you need responsive guidance and advocacy, not a claims line that takes three days to return calls. Request references from current logistics clients and ask specifically how quickly the agent responded when a claim occurred and whether the carrier’s adjuster worked collaboratively to resolve the situation. Fleet insurance premiums have surged over the past decade, so cost matters, but the cheapest quote often comes from carriers with weak claims support or limited willingness to work with specialized logistics operations.

Risk Management Resources and Long-Term Value

Ask whether any provider you consider offers risk management resources like fleet assessments, driver training recommendations, or telematics guidance, since these services demonstrate a commitment to reducing your losses rather than just collecting premiums. A provider who actively helps you implement safety programs and driver monitoring can reduce accidents by 20 to 40 percent according to industry data, which translates directly into better renewal rates and lower long-term costs. An independent agent with logistics experience can tailor policies to your actual operation rather than applying a one-size-fits-all approach, ensuring you’re protected without overpaying for unnecessary limits.

Final Thoughts

Proper logistics fleet insurance protects your operation from the financial devastation that accidents, cargo loss, and vehicle downtime create. Nuclear verdicts averaging $25 million and premiums that have climbed 40% over the past decade show why getting coverage right matters to your bottom line. Working with a local agent who understands logistics operations ensures you avoid coverage gaps that turn into catastrophic losses while preventing overpayment for limits you don’t need.

An independent broker representing multiple carriers compares quotes across underwriters, confirms your FMCSA filings post correctly, and helps you implement telematics and safety programs that reduce premiums by 10% to 30%. This expertise translates into competitive pricing, proper protection, and responsive claims support when incidents occur. A generalist agent won’t ask the right questions about your routes, cargo types, or driver experience, leaving you exposed to gaps or unnecessary costs.

At Briggs Agency, Inc., we’ve served Crown Point and surrounding communities since 1946 as a family-owned independent agency representing multiple top-rated carriers. Our experienced local agents compare options and tailor logistics fleet insurance policies to your specific needs rather than applying a one-size-fits-all approach. Contact us today to discuss your fleet’s specific risks and get a customized quote that protects your business.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.