Motor Carrier Insurance Indiana: From Compliance to Peace of Mind

Running a motor carrier operation in Indiana means navigating federal and state regulations that can feel overwhelming. The right motor carrier insurance Indiana protects your fleet, your drivers, and your business from costly gaps in coverage.

At Briggs Agency, Inc., we’ve helped countless carriers move from simply checking compliance boxes to actually feeling confident about their protection. This guide walks you through what you need to know.

What Compliance Actually Costs Motor Carriers in Indiana

Federal Minimums vs. Real-World Protection

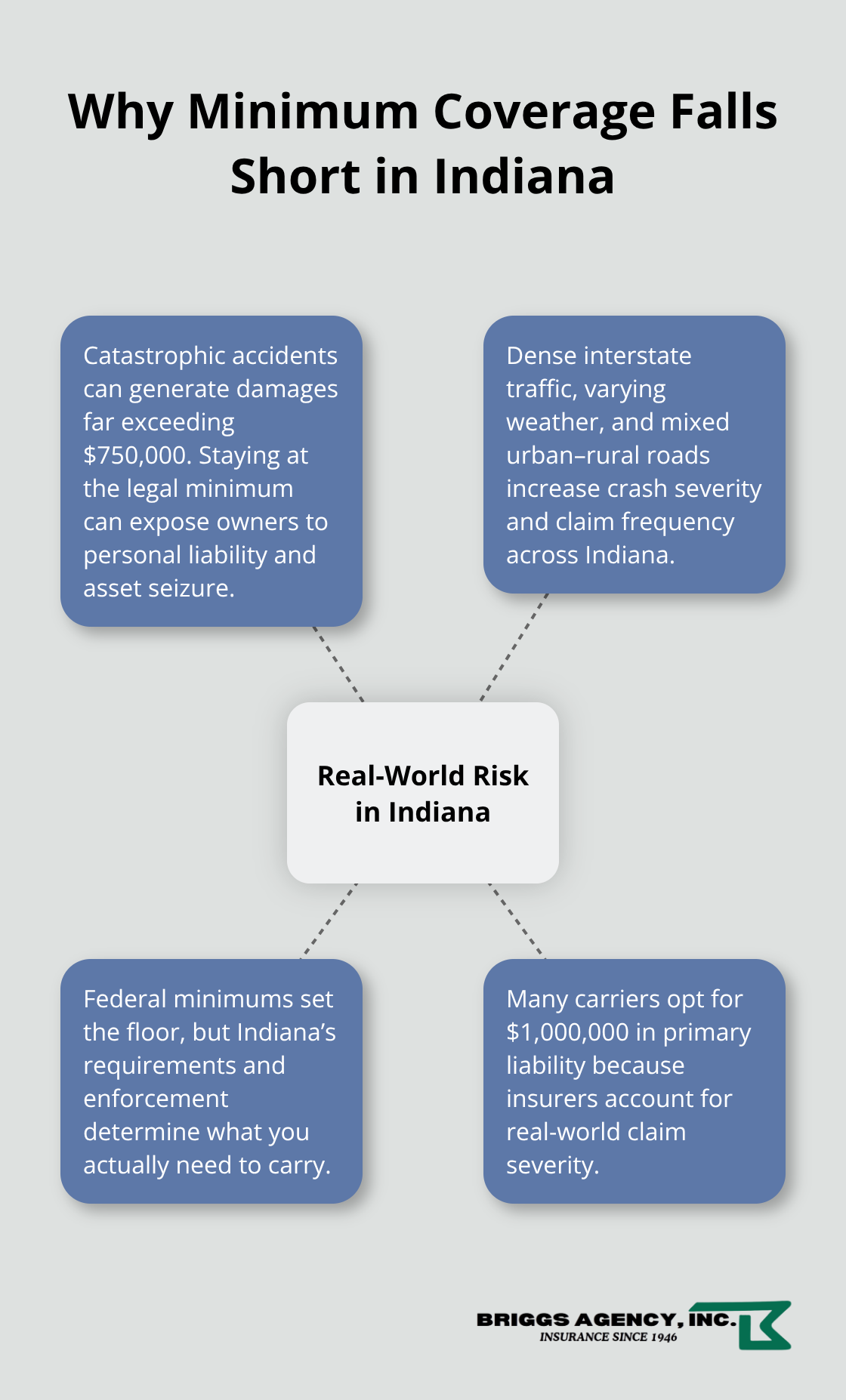

Federal regulations set the floor for motor carrier insurance, but Indiana’s specific requirements and enforcement practices determine what you actually need to carry. The Federal Motor Carrier Safety Administration requires a minimum of $750,000 in liability insurance for most operations, though many insurers push carriers toward $1,000,000 to account for real-world claim severity. If you operate under your own authority in Indiana, primary liability insurance is non-negotiable, and if you employ drivers, workers’ compensation becomes mandatory under state regulations.

The gap between federal minimums and what carriers actually need is where most operators stumble. A single catastrophic accident involving an 80,000-pound truck can generate damages far exceeding $750,000, which means staying at the legal minimum exposes your business to personal liability and potential asset seizure. Indiana’s dense truck traffic on interstates and highways combined with varying weather conditions and mixed urban-rural roads creates hazardous driving environments that increase crash severity and claim frequency.

Financial Penalties for Coverage Gaps

Violations carry real financial consequences that most carriers underestimate. Operating without proof of insurance, filing late forms, or misrepresenting coverage results in out-of-service orders that halt your revenue immediately. The FMCSA tracks safety violations through CSA scores, and a poor score directly impacts your insurability and premium rates.

Many carriers discover too late that their coverage gaps leave them personally liable for settlements, medical expenses, and lost wages from injured parties. For leased owner-operators, non-trucking liability coverage and downtime expense coverage address blind spots that basic policies miss entirely.

Beyond Standard Commercial Policies

Cargo coverage, including bulk commodity options for specialized shipments, protects against losses that standard auto policies ignore completely. Equipment coverage, trailer interchange, and motor carrier reimbursement coverage exist because standard commercial policies were never designed for trucking operations.

The practical reality is that compliance means more than filing paperwork with the state; it means having the right coverage structure in place before something goes wrong. Reviewing your current policy against your actual operation takes a few hours and prevents months of financial and legal headache down the road. Once you understand what your operation truly requires, the next step is identifying which specific coverage options actually protect your fleet and your bottom line.

Coverage Options That Protect Your Fleet

Liability Insurance: Your First Line of Defense

Liability insurance forms the foundation of any motor carrier operation, and the federal minimum is genuinely insufficient for most Indiana operations. A single serious accident involving your truck generates medical bills, lost wages, and pain-and-suffering awards that easily exceed that threshold. Many carriers operate with $1,000,000 in primary liability coverage because they’ve learned from claims that the federal floor leaves them personally exposed.

If you lease owner-operators or operate under your own authority, primary liability protects you against third-party claims-meaning it covers injuries or property damage your truck causes to someone else. The practical reality is that moving to higher coverage limits costs far less than the gap between what your minimum policy covers and what a catastrophic accident actually costs.

Physical Damage and Equipment Protection

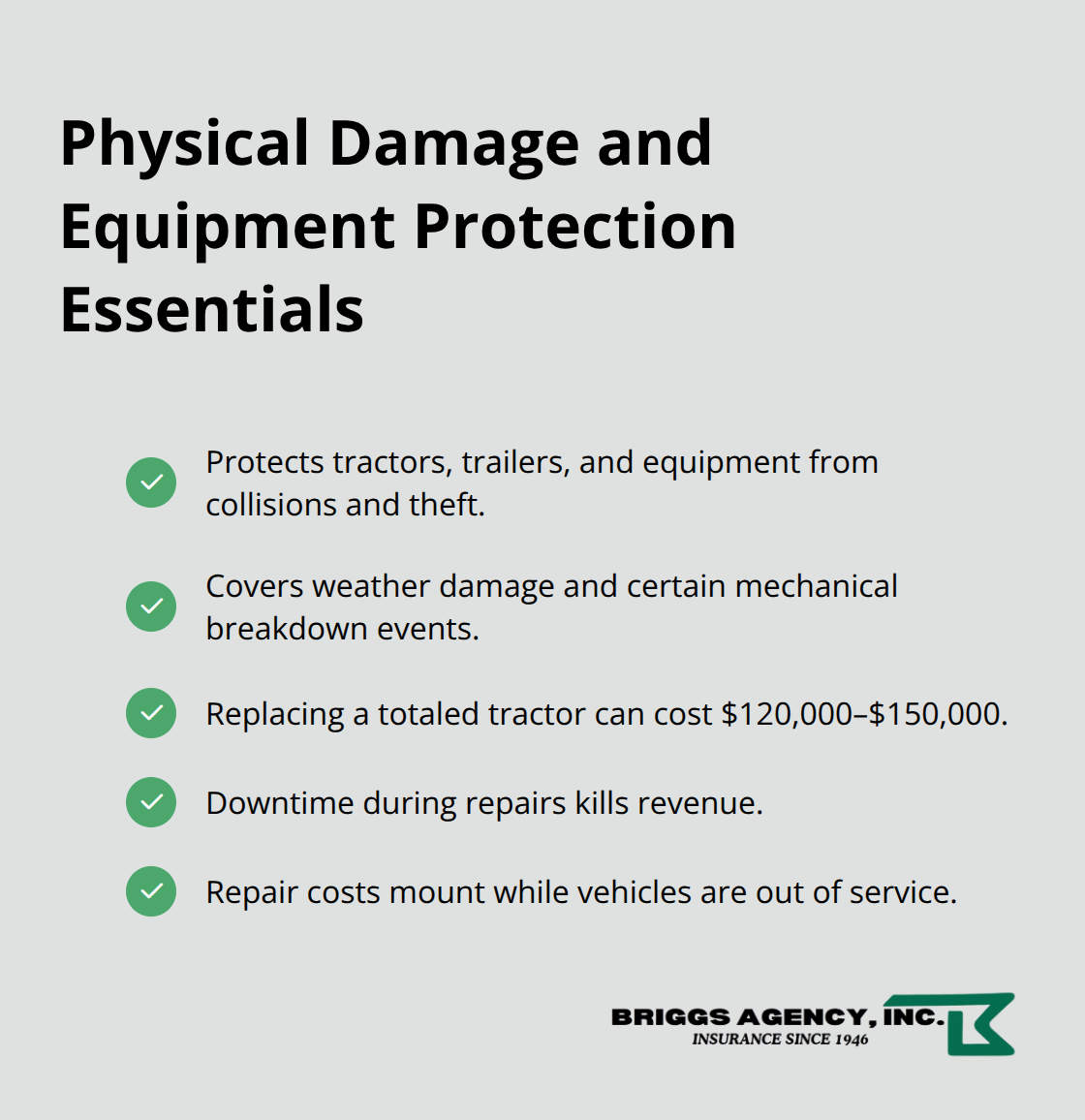

Physical damage coverage protects your vehicles themselves-your trailers, trucks, and equipment-from collisions, theft, weather, and mechanical breakdown. This matters more than many carriers realize because a single totaled tractor runs $120,000 to $150,000 to replace, and downtime during repairs kills your revenue while repair costs mount.

Equipment coverage extends protection to specialized attachments and tools, while lease value and financed value coverage specifically protect asset values for equipment you don’t own outright. These layers work together to keep your operation moving when accidents happen.

Cargo Coverage and Specialized Freight Protection

Cargo coverage is where most Indiana carriers discover they have dangerous gaps in their protection. Standard commercial policies don’t cover cargo loss, which means if your load shifts, spoils, or gets damaged in transit, you absorb the full cost and potentially face liability claims from your shipper.

Bulk commodity coverage addresses the specific risks of hauling specialized freight. Bobtail coverage (also called non-trucking liability) protects you when you operate outside standard trucking duties or deadhead without a load. Indiana’s mixed urban and rural roads, combined with winter weather and dense interstate traffic, create conditions where cargo shifts and accidents happen more frequently than carriers expect.

Additional Coverages That Close the Gaps

Trailer interchange coverage handles situations where you use someone else’s trailer, protecting you if that equipment causes damage. Motor carrier reimbursement coverage reimburses you for certain expenses when claims occur. These coverages exist because standard commercial policies were never designed for trucking operations.

The carriers we work with typically recommend layering these coverages rather than picking and choosing, because a single accident scenario often triggers multiple coverage needs simultaneously. Understanding what each coverage actually does and what gaps exist in your current policy reveals which risk management strategies reduce your claims frequency and keep your operation running smoothly.

Risk Management Strategies That Lower Your Insurance Costs

Driver Training Prevents the Accidents That Generate Claims

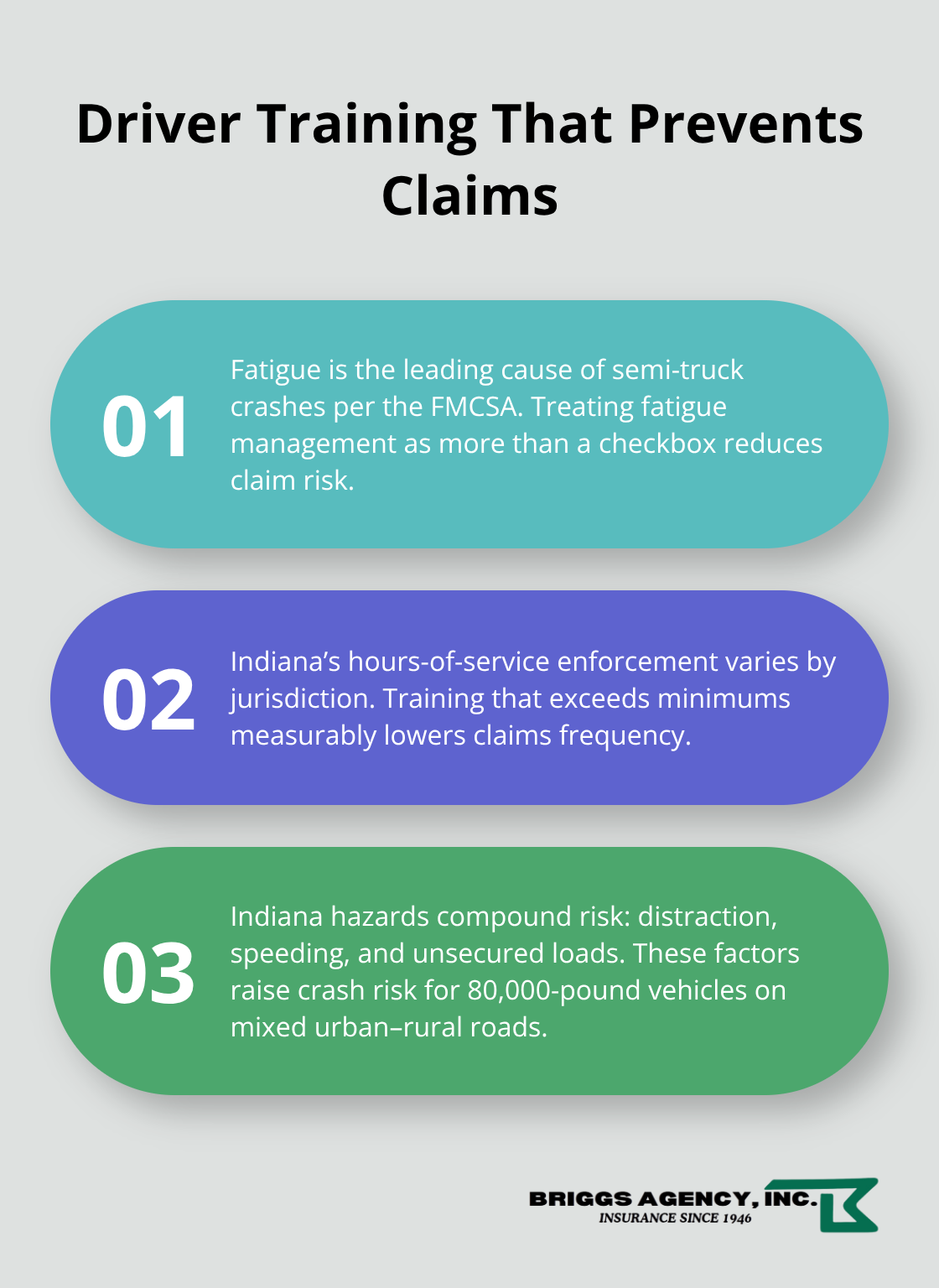

Driver fatigue remains the leading cause of semi-truck crashes according to the Federal Motor Carrier Safety Administration, yet most carriers treat fatigue management as a compliance checkbox rather than a cost-reduction strategy. Indiana’s enforcement of hours-of-service regulations varies across jurisdictions, which means carriers who invest in training programs that exceed minimum legal requirements see measurable reductions in claims frequency. A carrier operating tractor-trailers on Indiana interstates faces concrete hazards: distracted driving increases crash risk substantially when you’re piloting an 80,000-pound vehicle, speeding reduces reaction time on mixed urban-rural roads, and improperly secured cargo destabilizes trailers during the heavy truck traffic common on Indiana highways.

Structured driver safety programs directly lower your CSA scores, which insurers use to calculate premiums. Mandatory training on Indiana-specific road hazards, winter weather response, and load securement prevents the accidents that generate claims in the first place.

Vehicle Maintenance Creates Safer Operations and Lower Premiums

Mechanical failures in brakes, tires, and other components cause crashes that expose your operation to liability claims and out-of-service orders that halt revenue immediately. Regular inspection schedules that document maintenance create both safer operations and evidence of due diligence if a claim occurs.

Carriers reducing their insurance costs most aggressively treat maintenance as an investment that pays for itself through lower premiums and fewer downtime incidents. A single catastrophic accident involving your fleet doesn’t just generate immediate claim costs; it damages your safety profile for years, triggering premium increases across your entire operation.

How Loss Control Connects to Your Bottom Line

Carriers with strong safety records and documented maintenance programs qualify for better premium rates because insurers recognize reduced risk. The relationship between loss control and your insurance costs works in both directions-your operational practices directly influence what you pay for coverage.

Risk management becomes the bridge between your coverage structure and your actual costs. Implementing these strategies before you need them positions your operation to absorb unexpected incidents without derailing your business financially. Carriers operating most efficiently in Indiana understand that insurance isn’t just about compliance or coverage limits; it’s about building operational practices that prevent claims from happening in the first place.

Final Thoughts

Proper motor carrier insurance in Indiana protects your business when accidents happen in dense traffic and variable weather conditions. Coverage limits of $1,000,000 combined with cargo protection and equipment coverage mean a catastrophic accident doesn’t force you to liquidate assets or declare bankruptcy. Your drivers trained on Indiana-specific hazards and your fleet maintained on schedule prevent claims in the first place, which keeps your premiums lower and your CSA scores stronger.

Peace of mind comes from knowing exactly what your operation requires and having that protection in place before you need it. Review your current policy against your actual operation and compare your coverage limits against the real costs of accidents in your industry. Identify which specialized coverages you’re missing-cargo protection, equipment coverage, non-trucking liability-and understand what those gaps could cost you (a single totaled tractor runs $120,000 to $150,000 to replace, and downtime during repairs kills your revenue while repair costs mount).

Finding the right partner matters because motor carrier insurance requires someone who understands Indiana’s specific regulatory environment and the coverage structures that actually protect your business. Contact Briggs Agency, Inc. to review your current coverage and strengthen your protection with experienced local agents who work with motor carriers to build policies tailored to your actual needs.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.