Garage Insurance Coverage Options: Choosing the Right Policy for Your Shop

Running a garage means managing more than just vehicles and tools-you also need to protect your business from unexpected liability and property risks.

At Briggs Agency, Inc., we’ve helped countless shop owners navigate garage insurance coverage options and find policies that actually match their operations. The right coverage can be the difference between a manageable claim and a business-threatening loss.

What Coverage Types Does Your Shop Actually Need

Understanding Commercial General Liability

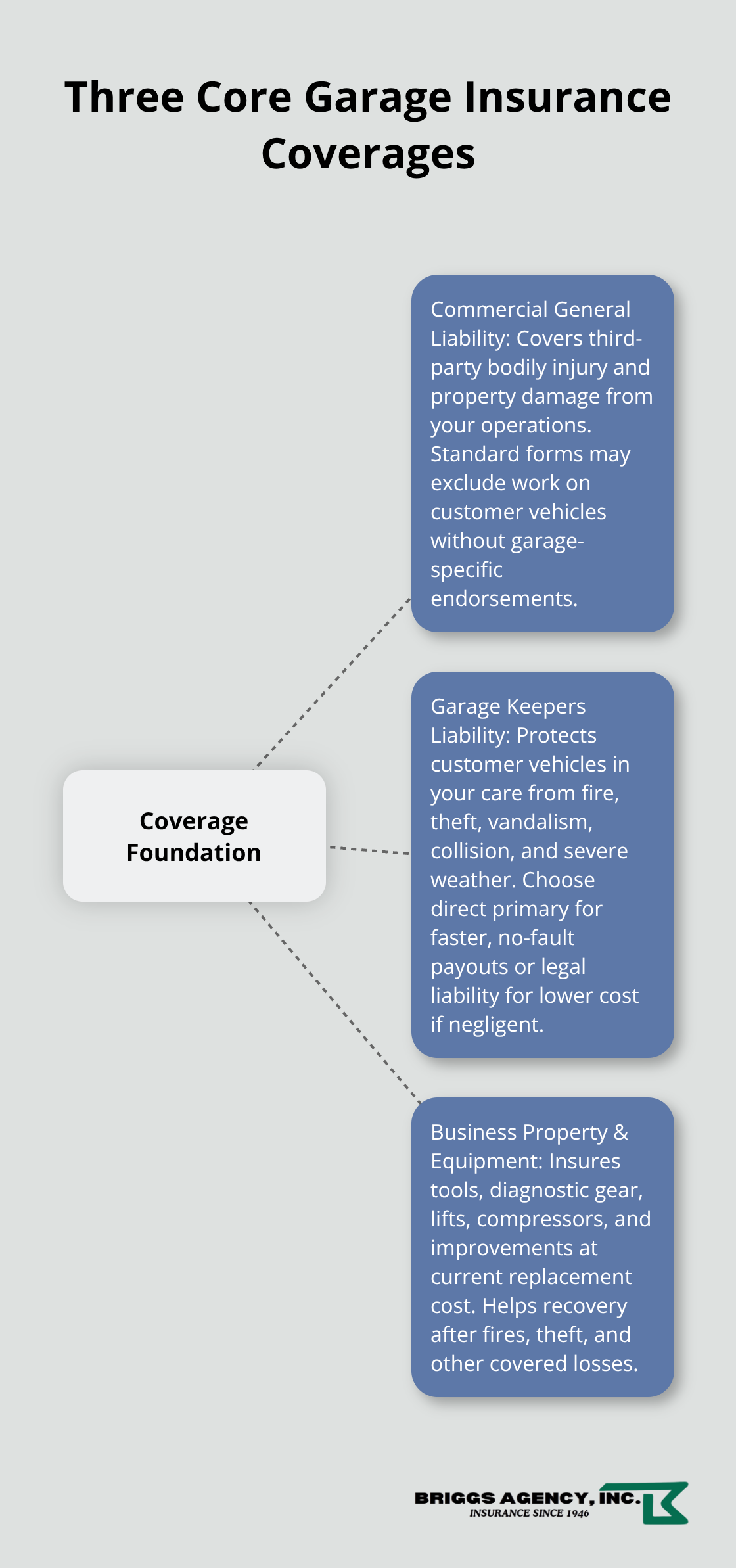

Garage insurance isn’t one-size-fits-all, and many shop owners discover coverage gaps only after a claim happens. Commercial general liability covers third-party bodily injury and property damage claims that arise from your operations-a customer slips in your waiting area, or an employee damages a client’s personal property. However, standard general liability policies often exclude work performed on customer vehicles, which is why garage-specific liability matters. This coverage protects you when faulty workmanship, a loose drain plug, or a misinstalled part causes damage after the vehicle leaves your shop. Making it more important than ever to have precise coverage that matches your actual exposures rather than overpaying for protection you don’t need.

Garage Keepers Liability: Protecting Vehicles in Your Care

Garage keepers liability forms the second essential layer of protection. This coverage protects customer vehicles while they remain in your care, custody, or control-whether parked in your bay, on your lot, or during a test drive. It covers fire, theft, vandalism, collision, and severe weather damage regardless of whether your shop is legally at fault. You’ll choose between direct primary coverage, which pays claims regardless of fault and speeds settlement, or legal liability coverage, which pays only if your shop is negligent and typically costs less. Direct primary is the stronger choice for most shops because it removes disputes with customer insurance companies and builds customer trust.

Business Property and Equipment Insurance

Business property and equipment insurance protects your own tools, diagnostic equipment, lifts, compressors, and building improvements. Many shop owners underestimate this exposure; a single bay fire or theft can eliminate thousands in specialized equipment. Set your coverage limits based on a current inventory of your shop’s assets, not on what you paid years ago (equipment values change). Annual policy reviews catch gaps as your services expand or equipment ages.

Moving Forward With Your Coverage Strategy

The right combination of these three coverage types creates a foundation that addresses the major risks your shop faces daily. Each layer addresses a different exposure, and gaps in any one area can leave your business vulnerable. Your next step involves evaluating your specific operation to determine which coverage options fit your situation best.

Key Factors to Consider When Selecting Garage Insurance

Size and Type of Your Operation

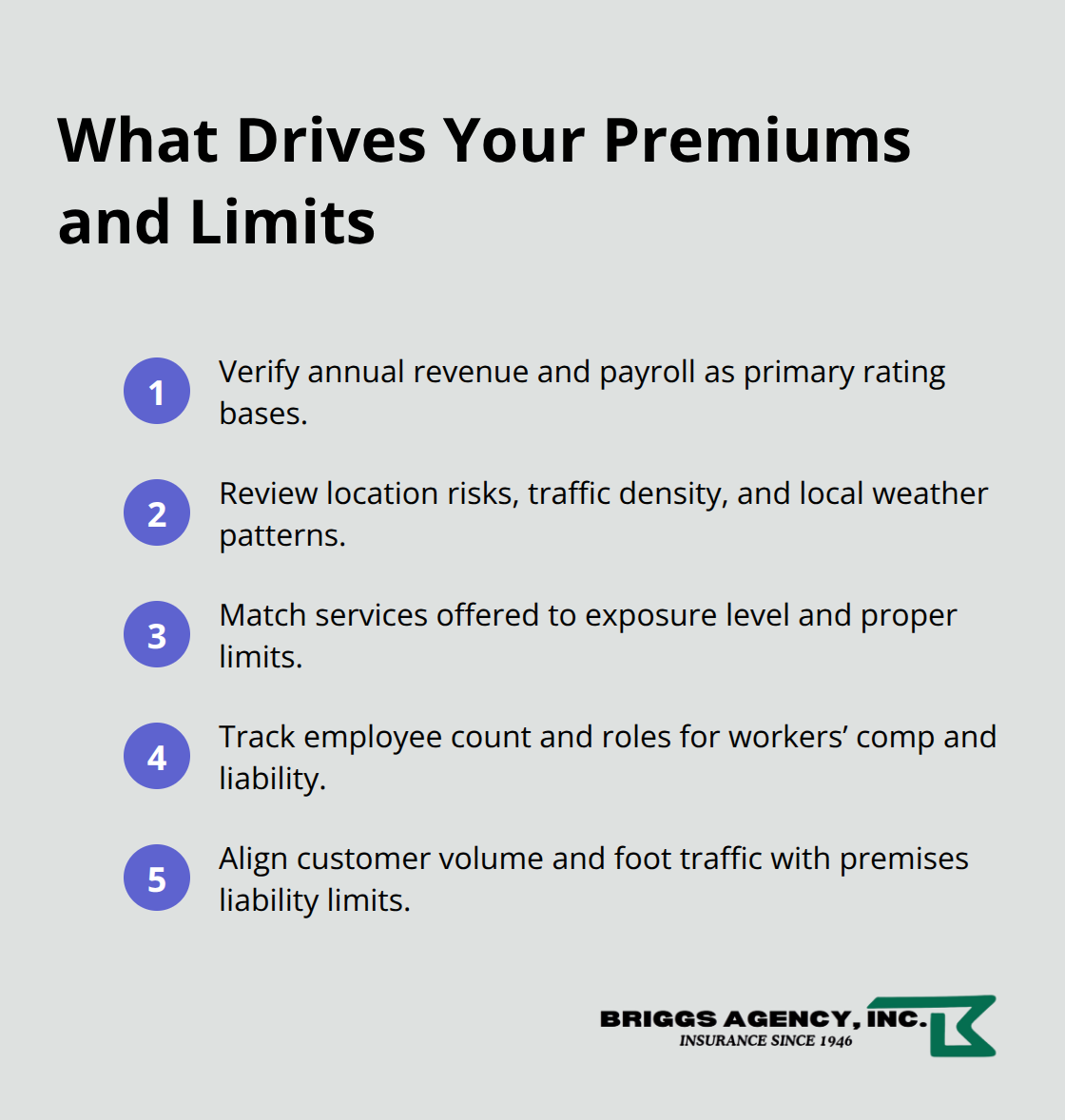

Your shop’s annual revenue, number of service bays, and employee count directly determine your coverage needs and premium costs. A solo operator running one bay faces vastly different exposures than a ten-person shop with multiple lifts and a parts inventory. Commercial lines premiums are rising, making it essential to right-size your coverage rather than overpay for unnecessary limits or underpay and create gaps.

Start with your actual annual revenue and payroll-most insurers base garage insurance premiums on these figures plus your claims history. A typical single-location repair shop pays between $4,000 and $10,000 annually for a complete program that includes garage liability, garage keepers, commercial property, and workers’ compensation, though this varies significantly by location, services offered, and risk profile.

Location matters considerably. If you operate in a high-density area like the Seattle metropolitan area where traffic congestion and severe weather increase collision and weather-related claims, you’ll pay higher premiums than shops in rural regions. The types of services you perform also matter enormously-a tire shop handling only tire sales and installation carries less exposure than a full-service transmission or engine rebuild operation where post-repair failures create significant completed operations liability.

Test Drives and Vehicle Operations

Shops that perform test drives on public roads need hired and non-owned auto coverage, which adds to your premium but is non-negotiable if employees regularly operate customer vehicles. This coverage protects you when an employee test-drives a customer’s car and causes an accident-your garage liability policy typically won’t cover this exposure without the proper endorsement. When you evaluate coverage, discuss with your insurance professional how the policy responds to your specific activities.

Number of Employees and Contractors

The number of employees and independent contractors working in your shop shapes your workers’ compensation costs and liability exposure significantly. Each additional employee increases your payroll base, which directly impacts workers’ compensation premiums in most states-this coverage is mandatory if you have employees and typically costs $1,500 to $4,000 annually depending on payroll and job classification.

If you use independent contractors for specialized work like custom upfitting or bodywork, confirm whether your garage liability policy covers their work or if you need separate endorsements or contractor liability coverage. Many shop owners assume their garage policy automatically covers subcontractors, then discover a coverage gap after a claim arises.

Customer Volume and Premises Exposure

Premises liability-slip-and-falls, customer injuries on-site-becomes a real exposure as your customer volume grows. A shop with five employees handling 50 customer vehicles weekly faces different daily risk than a solo operation handling 10 vehicles, so your coverage limits should reflect your actual transaction volume and foot traffic rather than industry averages. This assessment directly influences which coverage options you’ll need and at what limits, setting the stage for evaluating the specific types of vehicles and services your shop handles.

Common Coverage Gaps That Cost Shop Owners Money

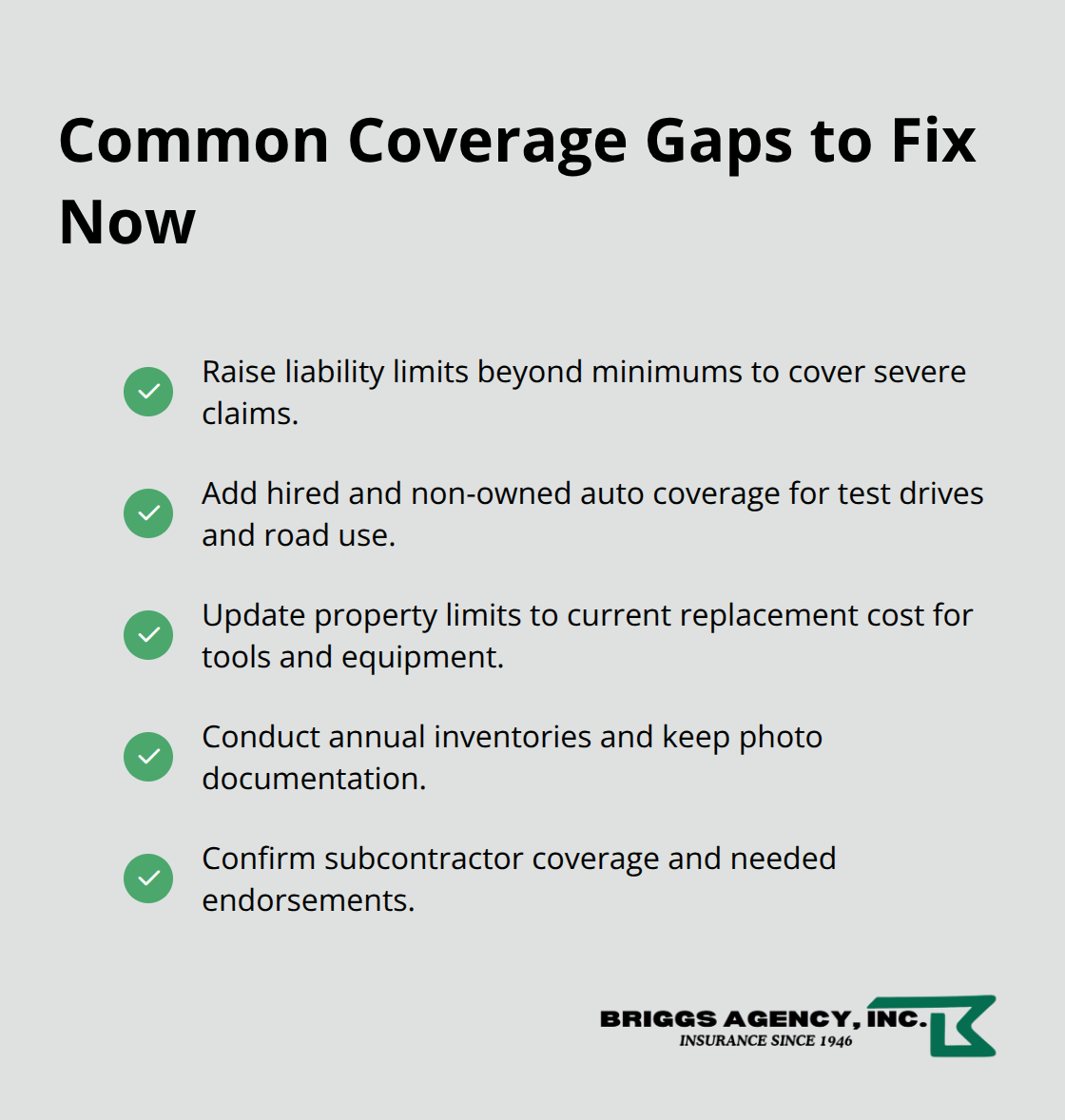

Most shop owners face their coverage shortfalls the hard way-after a claim gets denied or partially paid. The Insurance Information Institute reported that commercial lines premiums rose 7.1 percent in 2024, which means cutting coverage to save on premiums creates dangerous exposure. Inadequate liability limits rank as the most common mistake we see at shops across the region. Many shops carry minimum limits of $300,000 to $500,000 per occurrence, which sounds substantial until a serious injury or major property damage claim arrives.

Why Liability Limits Matter More Than You Think

A customer’s permanent disability from a shop accident, or a fire that spreads to an adjacent business, can easily exceed $1 million in damages. If your policy maxes out at $500,000 and the judgment is $1.2 million, you’re personally liable for the gap-potentially threatening your business and personal assets. The fix requires honest assessment of your worst-case scenario. A ten-person shop performing engine rebuilds and transmission work should carry minimum limits of $1 million per occurrence and $2 million aggregate, not the lowest available option. Calculate appropriate limits by considering your annual revenue, the types of vehicles you service, and the dollar value of potential post-repair failures.

Hired and Non-Owned Auto Coverage: A Frequently Overlooked Exposure

Hired and non-owned auto coverage represents the second major gap, particularly for shops that perform test drives or road tests. Your garage liability policy does not automatically cover accidents when employees operate customer vehicles on public roads. If an employee test-drives a customer’s car and causes a collision, injuring another motorist, your garage policy likely denies the claim. You need a specific endorsement or separate hired and non-owned auto coverage, which typically costs $300 to $800 annually depending on your vehicle volume and employee count. Many shop owners skip this coverage thinking it’s included, then face a six-figure claim with no protection.

Equipment and Tools: The Hidden Asset Gap

The third gap involves underinsuring tools, diagnostic equipment, and shop improvements. Shops accumulate expensive assets over time-alignment machines, tire machines, diagnostic computers, lifts-yet many owners never adjust their property insurance limits to match current replacement costs. A single electrical fire can destroy $50,000 in equipment, but if your property policy only covers $20,000, you absorb the loss. Conduct a physical inventory of your equipment at least annually, photograph it, and confirm your property coverage matches current replacement value, not what you paid five years ago. This simple step prevents thousands in uninsured losses when disaster strikes.

Final Thoughts

Selecting the right garage insurance coverage options requires understanding how commercial general liability, garage keepers liability, and business property insurance work together to protect your shop. Each coverage type addresses a distinct risk, and gaps in any area expose your business to significant financial loss. The most common mistakes happen when shop owners underestimate liability limits, skip hired and non-owned auto coverage for test drives, or fail to update property insurance as equipment values change.

Your garage insurance needs shift as your business grows, adds services, or changes operations. Annual policy reviews catch these shifts before they become problems, and rising commercial premiums make this process even more important. Review your limits against your worst-case scenarios, confirm that all your actual activities are covered, and adjust your deductibles based on what your shop can realistically absorb out-of-pocket.

Finding the right garage insurance provider means working with someone who understands your specific operation, not just selling you a standard package. Contact us at Briggs Agency, Inc. to discuss your garage insurance needs and get a quote that reflects your actual business-our experienced local agents take time to understand your services, your employee count, your location, and your risk profile, then build a program that addresses your real needs.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.