Restaurant Liquor Liability Insurance: What It Covers and Why It Matters

Running a restaurant means managing countless risks, and alcohol service creates exposure that many owners underestimate. A single incident-whether it’s a patron injured after overservice or a drunk driving accident-can result in lawsuits that threaten your business.

Restaurant liquor liability insurance protects you from these financial and legal consequences. At Briggs Agency, Inc., we help restaurant owners understand exactly what this coverage includes and why it’s not optional in most states.

What Restaurant Liquor Liability Insurance Covers

Restaurant liquor liability insurance protects you from the financial fallout when a patron you served alcohol causes injury or property damage to someone else. This distinction matters: the policy protects you from third-party claims, not claims from the customer who drank at your establishment. If a patron leaves your restaurant intoxicated and causes a car accident, injuring another driver, that injured driver can sue your business under dram shop laws that hold bars, restaurants, and other alcohol-serving establishments legally liable for injuries caused by intoxicated patrons. Your liquor liability policy covers the medical bills for that injured third party, property damage to their vehicle, and your legal defense costs-which can easily reach tens of thousands of dollars before any settlement is paid.

Assault, Battery, and On-Premises Incidents

The policy also covers assault and battery claims when an intoxicated customer injures someone on your premises or nearby. A fight that breaks out between patrons, or an intoxicated customer who becomes aggressive toward staff or other guests, creates direct liability exposure. Your coverage pays for the injured party’s medical expenses, the cost of defending yourself in court, and any settlement or judgment awarded against your business. Additionally, the policy covers property damage caused by intoxicated patrons, such as breaking furniture, damaging fixtures, or destroying other customers’ belongings during an incident.

How Defense Costs Work

Legal defense costs are covered separately from settlement amounts, which matters significantly. If someone sues your restaurant over an alcohol-related incident, your insurer typically pays your attorney fees and court expenses as the claim progresses, regardless of whether you ultimately win or lose. This protection is essential because defense costs alone often exceed $10,000 to $50,000 for straightforward cases, and complex litigation can push that figure much higher. Many restaurant owners don’t realize that without liquor liability coverage, they personally fund these legal expenses upfront while the claim is investigated and litigated.

Coverage Limits and Risk Assessment

With coverage in place, your insurer handles the defense cost obligation, protecting your cash flow during what can be a lengthy process. Coverage limits matter here too-typical policies offer $1 million per occurrence and $2 million aggregate, though limits vary based on your risk profile. Higher-risk establishments with significant alcohol revenue should consider limits at the $2 million or $5 million level to account for potential catastrophic incidents. Understanding your specific exposure helps you select limits that actually match your operation rather than settling for a standard policy that leaves gaps.

Why Your Restaurant Needs This Coverage

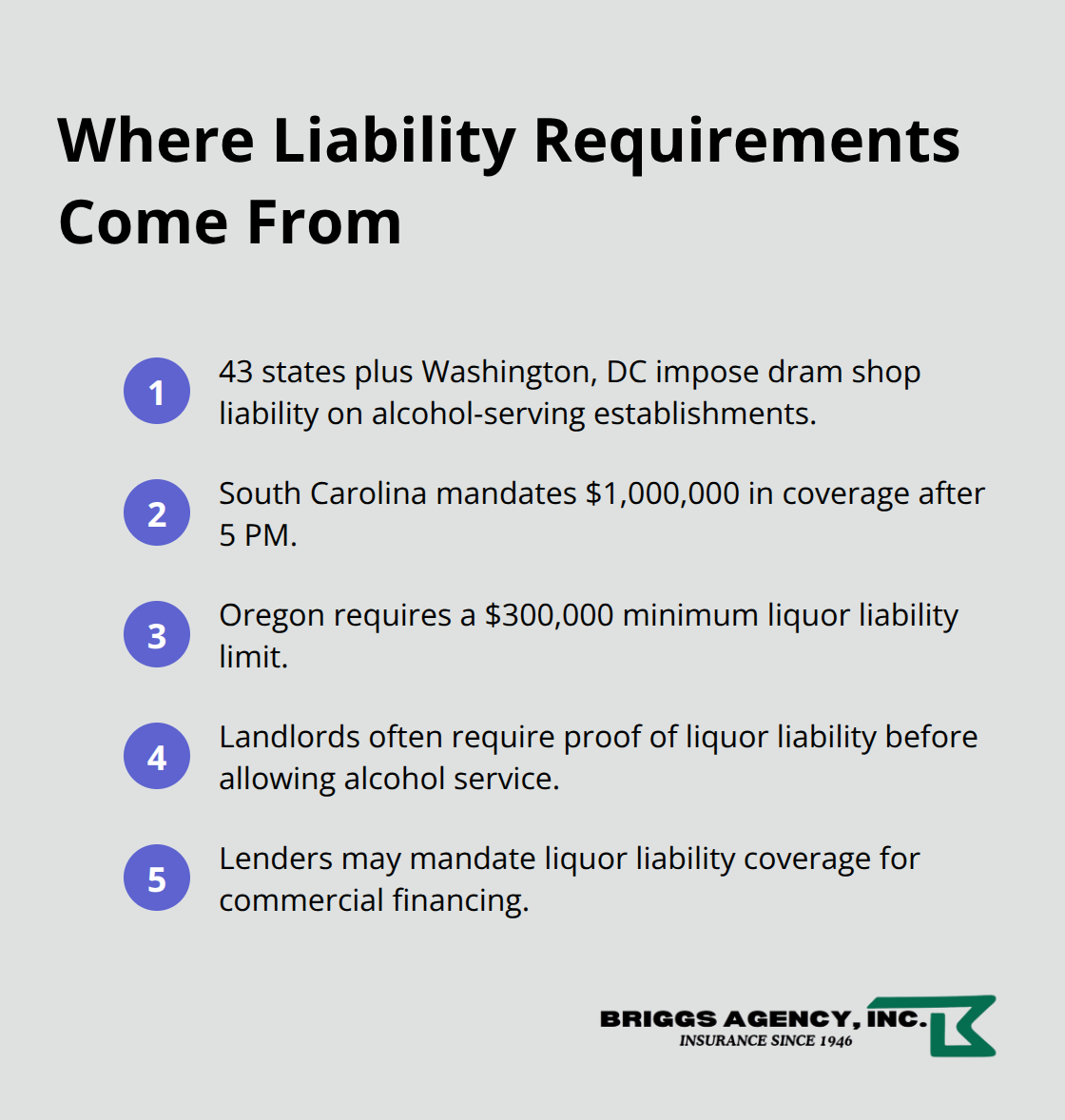

Legal Liability in 43 States Plus DC

Dram shop laws in 43 states plus Washington DC create direct legal liability for restaurants that serve alcohol, making liquor liability coverage a compliance requirement, not a luxury. In states like South Carolina, regulations mandate $1 million in coverage after 5 PM, while Oregon requires a $300,000 minimum. Even in states without statutory minimums, landlords and lenders frequently require proof of liquor liability before allowing alcohol service or approving commercial loans.

Without coverage, your restaurant operates in violation of lease terms or financing agreements, risking eviction or foreclosure regardless of whether a claim ever materializes. The National Conference of State Legislatures documents that dram shop statutes hold establishments liable when they serve visibly intoxicated individuals or minors, with liability extending to third-party injuries-meaning an intoxicated patron who causes a car accident can trigger a lawsuit against your business.

The True Cost of a Single Incident

The financial exposure from a single incident justifies coverage immediately. Defense costs for alcohol-related litigation typically range from $25,000 to $100,000 before any settlement is considered, and major incidents routinely exceed $500,000 when settlements, medical expenses, and reputational damage combine. A patron served at your bar who causes a multi-car accident involving serious injuries generates catastrophic liability-medical bills, lost wages, pain and suffering claims, and punitive damages in some states can easily reach $2 million or higher. Without coverage, your personal assets, business bank accounts, and future earnings become targets for judgment collection.

Protecting Your Liquor License and Operations

Insurance also protects your liquor license itself; many states suspend or revoke licenses following uninsured alcohol-related incidents, effectively shutting down your revenue stream. Licensing investigations consume months and legal fees totaling six figures, even when coverage would have resolved the claim in weeks. The cost of a liquor liability policy-typically $25 to $200 monthly depending on alcohol sales volume and location-is negligible compared to the financial and operational destruction a single uninsured claim creates. This protection extends beyond the immediate incident; it safeguards your ability to continue operating and serving your community.

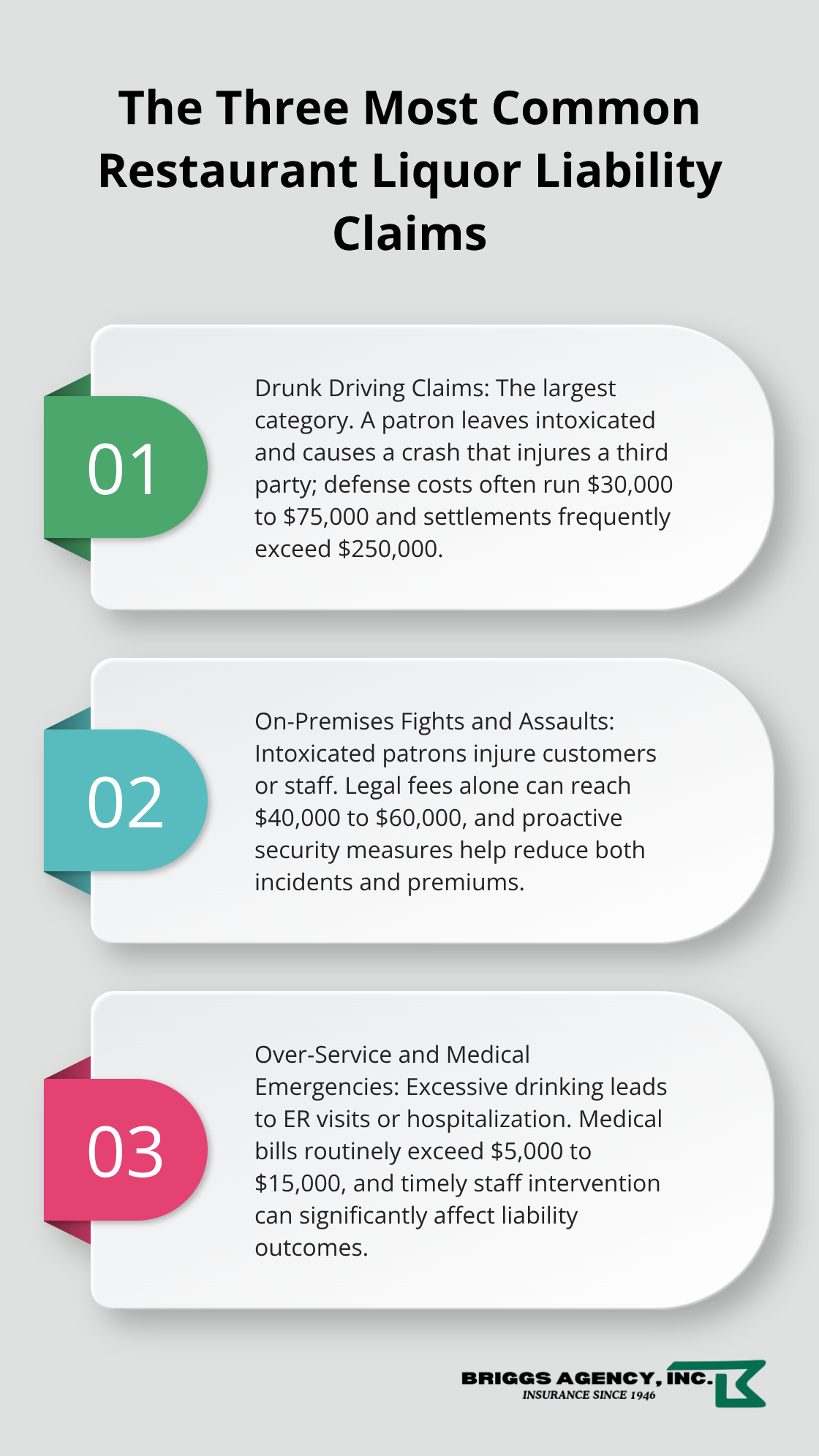

What Claims Actually Happen at Restaurants

Alcohol-related incidents at restaurants follow predictable patterns, and understanding them helps you recognize your actual exposure. These incidents fall into three categories that liquor liability claims address directly, and each demands different operational responses from your team.

Drunk Driving Claims and Third-Party Injuries

Drunk driving claims represent the largest category of liquor liability lawsuits against restaurants. A patron drinks at your establishment, leaves intoxicated, and causes a traffic accident that injures another driver or passenger. That injured third party sues your restaurant under dram shop law, claiming you overserved or failed to recognize visible intoxication before allowing the customer to leave. Defense costs for these cases range from $30,000 to $75,000 for straightforward accidents, and settlements frequently exceed $250,000 when injuries are moderate to severe.

Your staff’s ability to recognize impairment matters legally. If your server failed to observe obvious signs like slurred speech, unsteady movement, or repeated ordering of strong drinks, liability becomes harder to defend. Training programs like TIPS alcohol service certification directly reduce your risk profile. Staff who complete this training learn to identify intoxication early and intervene before a customer reaches dangerous levels of impairment.

On-Premises Fights and Assault Claims

On-premises fights and assaults create immediate, visible liability that many restaurant owners underestimate. An intoxicated patron becomes aggressive toward another customer, staff member, or both, resulting in injuries that require medical treatment or hospitalization. Your business faces claims not just for the injured party’s medical bills but also for the cost of defending yourself against assault allegations, which can reach $40,000 to $60,000 in legal fees alone.

Security measures directly impact these claims. Restaurants with trained security staff, visible camera systems, and clear protocols for removing disruptive patrons experience fewer incidents and lower insurance costs. These investments signal to your insurer that you take risk seriously, and many carriers reward proactive establishments with premium reductions. The presence of security also deters aggressive behavior before it escalates into costly incidents.

Over-Service and Medical Emergencies

Over-service that leads to medical emergencies represents the third major claim category. A customer drinks excessively at your restaurant and experiences alcohol poisoning, seizures, or other health crises requiring emergency room treatment or hospitalization. While these claims sometimes involve the customer themselves rather than third parties, they still trigger significant liability exposure and defense costs. Medical bills for alcohol-related emergency room visits and hospitalizations routinely exceed $5,000 to $15,000 per incident, and your establishment’s liability depends on whether staff recognized the customer needed help.

Your server’s decision to cut someone off, provide water and food, or call emergency services directly influences claim outcomes and demonstrates reasonable care under dram shop laws. Staff who notice warning signs-extreme drowsiness, difficulty standing, or slurred speech-and respond appropriately protect both the customer and your business from catastrophic outcomes. This intervention also shows regulators and insurers that your team prioritizes safety over additional drink sales.

Final Thoughts

Restaurant liquor liability insurance protects your business from the financial devastation that follows alcohol-related incidents. Whether a drunk driving claim, an on-premises fight, or an over-service emergency occurs, the coverage pays for defense costs, settlements, and medical expenses that would otherwise drain your business bank account or force you into personal liability. The cost of this protection-typically $25 to $200 monthly-is insignificant compared to the six-figure exposure a single incident creates.

The real value extends beyond claim payments. Liquor liability coverage keeps your liquor license intact, maintains your ability to operate, and demonstrates to landlords and lenders that you take risk seriously. In 43 states plus DC, dram shop laws make this coverage a legal and practical necessity, not an optional add-on. Your staff’s training, your security measures, and your responsible service policies all work together with insurance to create a complete risk management strategy.

At Briggs Agency, Inc., we help restaurant owners understand their actual exposure and select coverage that matches their operation. Contact us to discuss your restaurant’s liquor liability needs and receive a customized quote-we’ll walk you through coverage options, explain what your restaurant liquor liability insurance covers, and help you implement risk management practices that reduce claims and lower premiums.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.