Indiana Trucking Insurance: Finding the Right Coverage for Your Fleet

Running a trucking fleet in Indiana means navigating insurance requirements that go far beyond standard commercial auto policies. The liability limits, cargo protections, and specialized coverage your operation needs are substantial and legally mandated.

At Briggs Agency, Inc., we work with fleet operators across Indiana who need Indiana trucking insurance that actually fits their business. This guide walks you through the coverage types that matter, how to evaluate providers, and what to look for when protecting your fleet.

Why Trucking Insurance Costs More Than Standard Commercial Auto

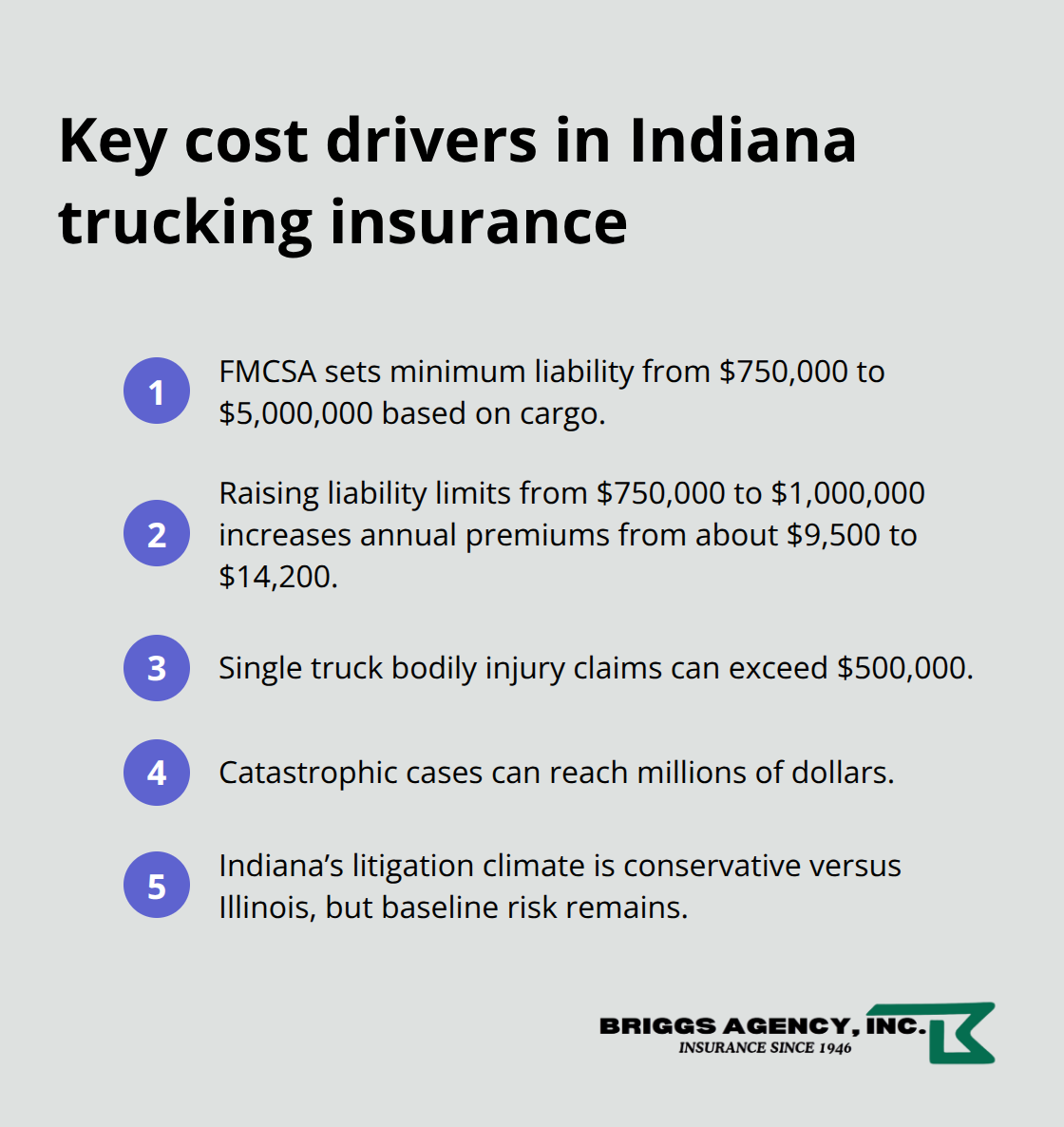

Trucking insurance operates in a different risk universe than standard commercial auto policies, which is why Indiana carriers face significantly higher premiums and stricter coverage requirements. The Federal Motor Carrier Safety Administration mandates minimum liability of $750,000 for non-hazardous freight and up to $5,000,000 for hazmat shipments, depending on cargo type. These aren’t suggestions-they’re legal floors that protect you from catastrophic exposure. A semi-truck operator in Indiana with $750,000 liability coverage pays roughly $9,500 annually, but increase that to $1,000,000 in liability limits and the cost rises to approximately $14,200 per year. The reason is straightforward: trucking claims are expensive. A single bodily injury incident involving a commercial truck can easily exceed $500,000, and catastrophic cases push into the millions.

Indiana’s litigation environment is relatively conservative compared to neighboring Illinois, which helps keep premiums lower than some regions, but the baseline costs still reflect genuine risk.

Cargo Type and Specialized Endorsements Drive Premium Increases

Your cargo matters significantly. Hauling steel coils introduces load-shifting risks that many standard policies exclude entirely. In Northwest Indiana, where coil shipments are common, carriers often require a dedicated metal coil endorsement on your cargo policy-sometimes adding $500 to $1,500 annually depending on your operation’s volume and history. Without this endorsement, a claim involving coil cargo could be denied outright, wiping out your entire profit margin on that load. High-value or temperature-sensitive loads require higher limits and careful alignment with actual cargo risk. Many shippers now demand $1,000,000 in liability and $100,000 in cargo coverage as a baseline for coil shipments and specialized freight.

Bobtail Coverage Fills a Critical Gap in Your Protection

Most trucking liability policies contain a critical gap: they exclude coverage when you drive without a dispatch load. This non-trucking use-moving between loads, heading to maintenance, or running personal errands-leaves you exposed to six-figure claims if you cause an accident. Primary liability insurance often excludes these situations entirely, meaning you could face a judgment with zero policy protection. Bobtail coverage fills this gap and should be non-negotiable in your policy. The cost is modest, typically running between $1,000 to $3,000 annually, but the protection is essential. Indiana’s winter weather, jackknifes on high-traffic corridors around Indianapolis and Gary, and congested routes create real bodily injury and property damage risk even when you’re not under dispatch.

Physical Damage Coverage and Deductible Strategy

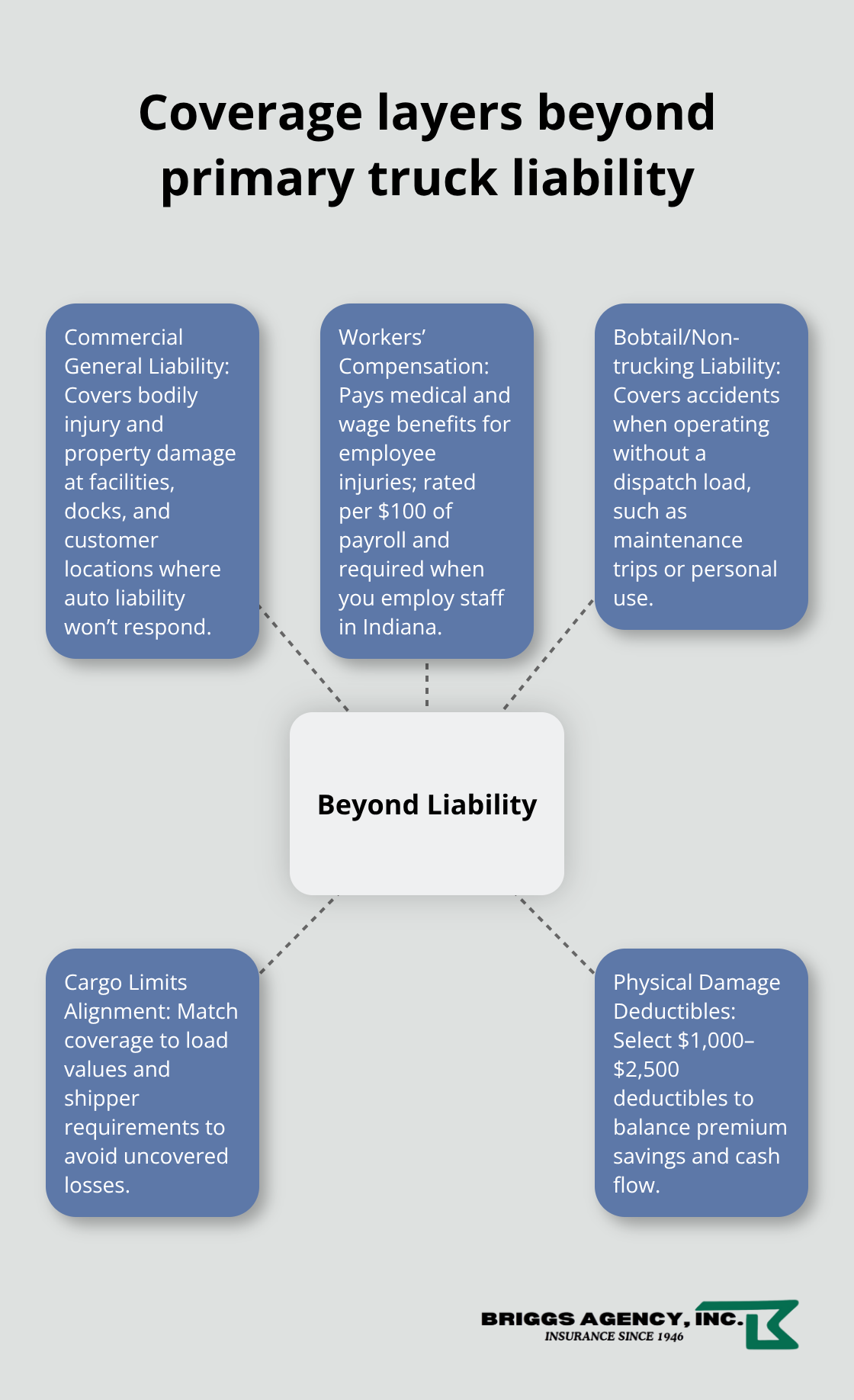

Physical damage coverage for your truck and trailers requires careful attention to deductibles. A $1,000 to $2,500 deductible range balances premium savings with your ability to cover repairs without destroying cash flow. Deductibles above $2,500 force you to self-fund major repairs, which can cripple operations if you face multiple claims in a season. Your trailer cargo coverage must scale with actual shipment values-set limits at roughly 120 percent of your typical load value to protect against spikes without overpaying for coverage you won’t use. Coordinate these limits closely with your shipper’s requirements, since many now demand specific coverage thresholds as a condition of doing business.

Understanding these cost drivers helps you see why Indiana trucking insurance demands more than a standard commercial auto quote. The next step is identifying which specific coverage types your operation actually needs to stay compliant and protected.

Essential Coverage Beyond Liability

Your trucking operation needs three additional coverage layers that protect your assets, employees, and bottom line beyond the baseline liability limits Indiana law requires. Commercial General Liability insurance, Workers’ Compensation for your team, and Bobtail coverage each fill specific gaps that your primary truck liability policy leaves open. Understanding what each covers and why it matters helps you build a protection strategy that actually matches your operation.

Commercial General Liability Protects Your Facilities and Operations

Commercial General Liability insurance covers bodily injury and property damage claims that occur at your facilities, loading docks, or customer locations-situations where your primary truck liability policy won’t respond. A $1,000,000 CGL limit typically costs $300 to $500 annually and becomes essential the moment you lease yard space, employ staff, or operate from a fixed facility. This coverage protects against third-party claims unrelated to active driving, such as someone injured on your property or damage to a customer’s dock during loading operations.

Many carriers overlook CGL entirely because they focus exclusively on vehicle liability, then face gaps when claims arise outside the truck itself. Your operation exposes you to liability beyond the road, and CGL fills that exposure directly.

Workers’ Compensation Protects Your Employees and Your Business

Workers’ compensation insurance is mandatory in Indiana if you employ drivers or warehouse staff. Your insurer charges a rate per $100 of payroll based on your industry classification and claims history. On average, trucking companies in Indiana can expect to pay between $0.75 to $2.00 per $100 of payroll for workers’ compensation insurance. This coverage protects your operation from catastrophic exposure: a driver with a back injury or a loading dock employee with a crushed foot generates $50,000 to $250,000 in medical and wage-replacement costs. Without workers’ compensation, you face personal liability for these expenses plus potential regulatory penalties that can shut down your operation.

Bobtail Coverage Protects Non-Dispatch Driving

Bobtail and non-trucking liability coverage rounds out this protection layer by covering accidents that occur when your truck operates without a dispatch load. Most primary policies exclude coverage when you drive without revenue cargo-moving between loads, heading to maintenance, or running personal errands. The annual cost runs $1,000 to $3,000 depending on your vehicle type and driving record, but this modest expense prevents six-figure exposure during personal use, maintenance runs, or repositioning between loads. Indiana’s winter conditions and congested corridors around Indianapolis and Gary create genuine accident risk even without revenue cargo, making bobtail coverage a practical necessity rather than an optional add-on.

Layering Coverage Creates Complete Protection

These three coverage types cost between $4,000 and $7,000 annually for a typical owner-operator but prevent catastrophic gaps that eliminate years of profit from a single claim. Each layer addresses a specific exposure your primary liability policy leaves uncovered. The question shifts now from what coverage you need to how you identify a provider who understands Indiana’s trucking landscape well enough to build the right combination for your specific operation.

Finding the Right Indiana Trucking Insurance Provider

Choosing a trucking insurance provider in Indiana requires more than comparing price quotes side by side. You need a carrier or agent who understands the specific risks your operation faces, can navigate state compliance requirements accurately, and responds quickly when claims arise. The difference between a provider who simply sells a policy and one who builds customized protection for your fleet often surfaces in claim time or when you discover coverage gaps during an incident.

Request Detailed Quotes from Multiple Carriers

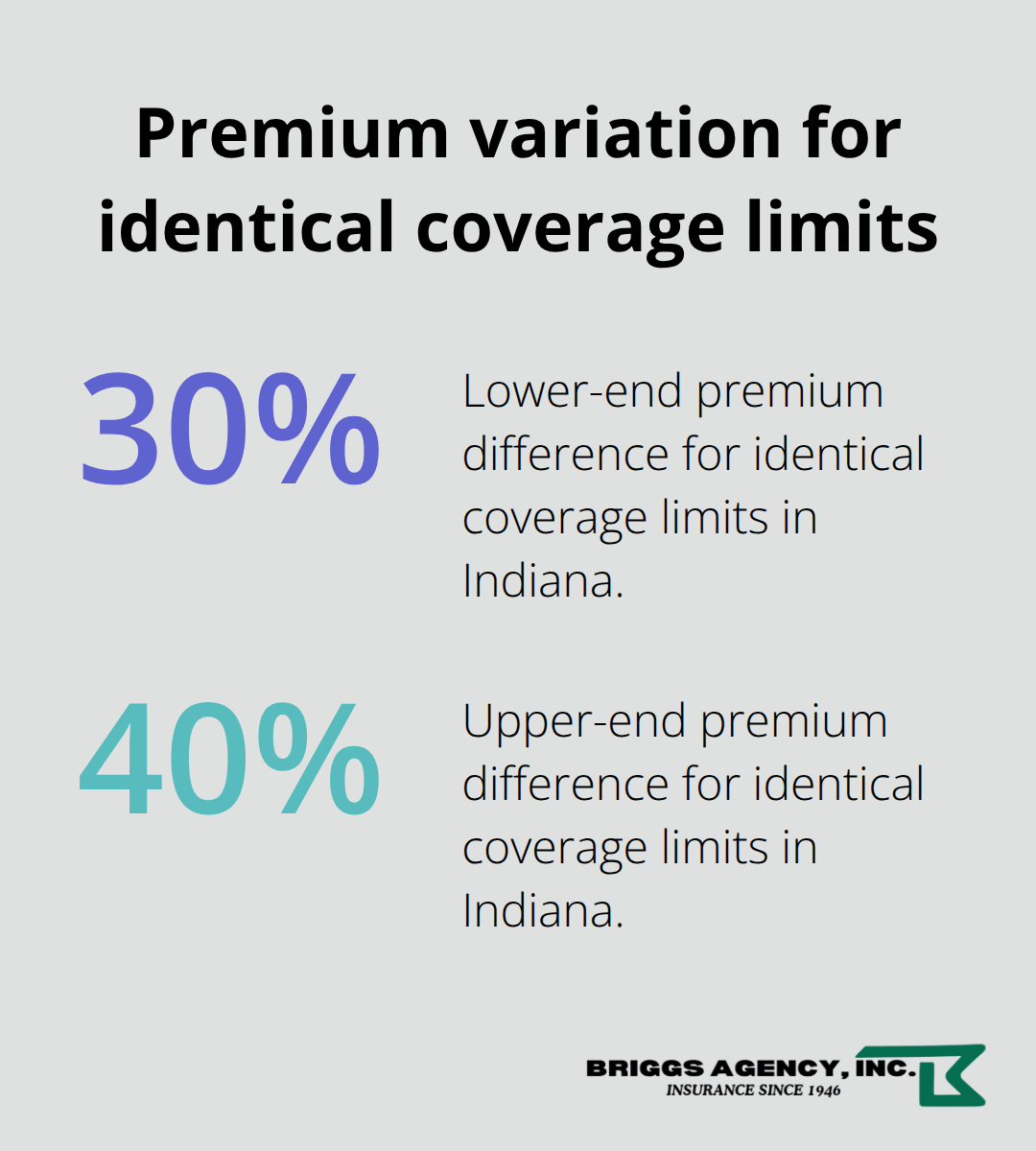

Start by requesting quotes from at least three carriers or independent agents who specialize in Indiana trucking operations. Identical coverage limits can carry 30 to 40 percent premium differences depending on how each carrier prices your specific operation, so comparing multiple options reveals whether you’re paying a fair rate. When you request quotes, provide detailed information about your actual operation: what cargo you haul, where you operate geographically, how often you drive without dispatch loads, your average and maximum load values, and your annual mileage in high-density corridors. Vague information produces vague quotes that don’t reflect your real risk profile.

Progressive, for example, has over 40 years of experience with Indiana commercial truck insurance and was named the number one truck insurer in America in 2024 by S&P Global Market Intelligence based on national written premium data. That national ranking, however, doesn’t automatically mean their local Indiana pricing matches your operation’s needs.

Evaluate Trucking-Specific Experience

Experience with trucking operations matters far more than general commercial insurance knowledge. Ask potential providers how many owner-operators and small fleets they currently serve in Indiana, whether they handle IOA-1 intrastate filings and Form E submissions directly, and whether they audit cargo policies for exclusions like coil gaps that could deny claims on your typical loads. A provider unfamiliar with metal coil endorsements or bobtail coverage gaps will miss critical protections your operation requires.

Local knowledge becomes essential when winter weather or high-traffic corridors around Indianapolis and Gary drive up your bodily injury exposure, or when you haul specialized cargo that demands specific endorsements. Ask how they handle claims: whether you can file and track claims online, how quickly they respond to roadside incidents, and whether they provide heavy truck roadside assistance beyond standard coverage.

Partner with Agents Who Understand Your Routes

The provider who invests time understanding your routes, cargo types, and non-dispatch usage patterns will identify coverage gaps and adjust your policy accordingly, preventing the costly discovery of excluded exposures during a claim. Briggs Agency, Inc. represents multiple top-rated carriers, which allows local agents to compare options and tailor policies that deliver both competitive pricing and the right protection for your specific fleet.

Final Thoughts

Protecting your Indiana trucking fleet requires layered coverage that extends well beyond minimum legal liability. Your operation needs commercial general liability for facility-based exposures, workers’ compensation for your team, bobtail protection for non-dispatch driving, and cargo coverage scaled to your actual shipment values. Physical damage deductibles between $1,000 and $2,500 balance premium savings with your ability to absorb repairs without destroying cash flow, while these combined layers cost $4,000 to $7,000 annually but prevent catastrophic gaps that eliminate years of profit from a single claim.

The provider you select matters as much as the coverage itself. A carrier or agent who understands Indiana’s specific risks-winter weather, congested corridors around Indianapolis and Gary, specialized cargo like steel coils-will build protection that matches your actual operation rather than a generic template. They handle IOA-1 filings, audit your cargo policy for exclusions, and respond quickly when claims arise, so comparing quotes from at least three carriers reveals whether you pay a fair rate (identical coverage often carries 30 to 40 percent premium differences).

Briggs Agency, Inc. represents multiple top-rated carriers and can compare options to deliver competitive pricing and the right Indiana trucking insurance protection for your fleet. Our experienced local agents understand the routes, cargo types, and non-dispatch usage patterns that shape your actual risk, then tailor policies accordingly. Contact us to discuss your fleet’s specific needs and secure a customized quote that protects what you’ve built.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.