Contractor Insurance Coverage Indiana: Policy Keys for Builders

Running a contracting business in Indiana means navigating specific insurance requirements that protect both your operation and your team. Contractor insurance coverage in Indiana isn’t one-size-fits-all, and missing the right policies can expose you to serious financial and legal risks.

We at Briggs Agency, Inc. have helped countless builders understand exactly what coverage they need and how to avoid overpaying for it. This guide walks you through Indiana’s requirements, the essential policies every contractor should carry, and practical ways to reduce your premiums.

What Indiana Actually Requires From Contractors

State-Mandated Coverage You Cannot Ignore

Indiana doesn’t mandate general liability insurance for all contractors, which surprises many builders who assume it’s a legal requirement. However, the state does require workers’ compensation insurance if you have even one employee-and that includes yourself if you operate as a sole proprietor with employees. The Indiana Department of Labor enforces this strictly, with penalties reaching $10,000 per violation for non-compliance.

If you bid on public construction projects, Indiana’s prevailing wage law applies, and many government entities require proof of workers’ compensation before awarding contracts. Additionally, if your contracting work involves driving commercial vehicles, Indiana requires minimum liability coverage of $25,000 for bodily injury per person and $50,000 per accident, plus $25,000 for property damage-these are among the lowest thresholds in the Midwest, but they’re non-negotiable.

The General Liability Gap That Costs Contractors

The real protection gap appears when contractors operate without general liability coverage. Indiana courts have consistently upheld homeowner lawsuits against contractors for property damage and bodily injury, with jury awards averaging $150,000 to $400,000 for serious incidents according to Indiana Trial Lawyers Association data. Most commercial contracts and bonding requirements demand general liability as a condition of doing business, making it practically mandatory even where state law doesn’t require it.

How Indiana Differs From Neighboring States

Indiana’s regulatory environment differs significantly from neighboring states like Ohio and Illinois-Indiana has no state licensing board for general contractors, which means less oversight but also less consumer protection for your clients. Your insurance credentials become even more important to build trust with property owners and project managers.

Equipment Theft and Workers’ Compensation Costs

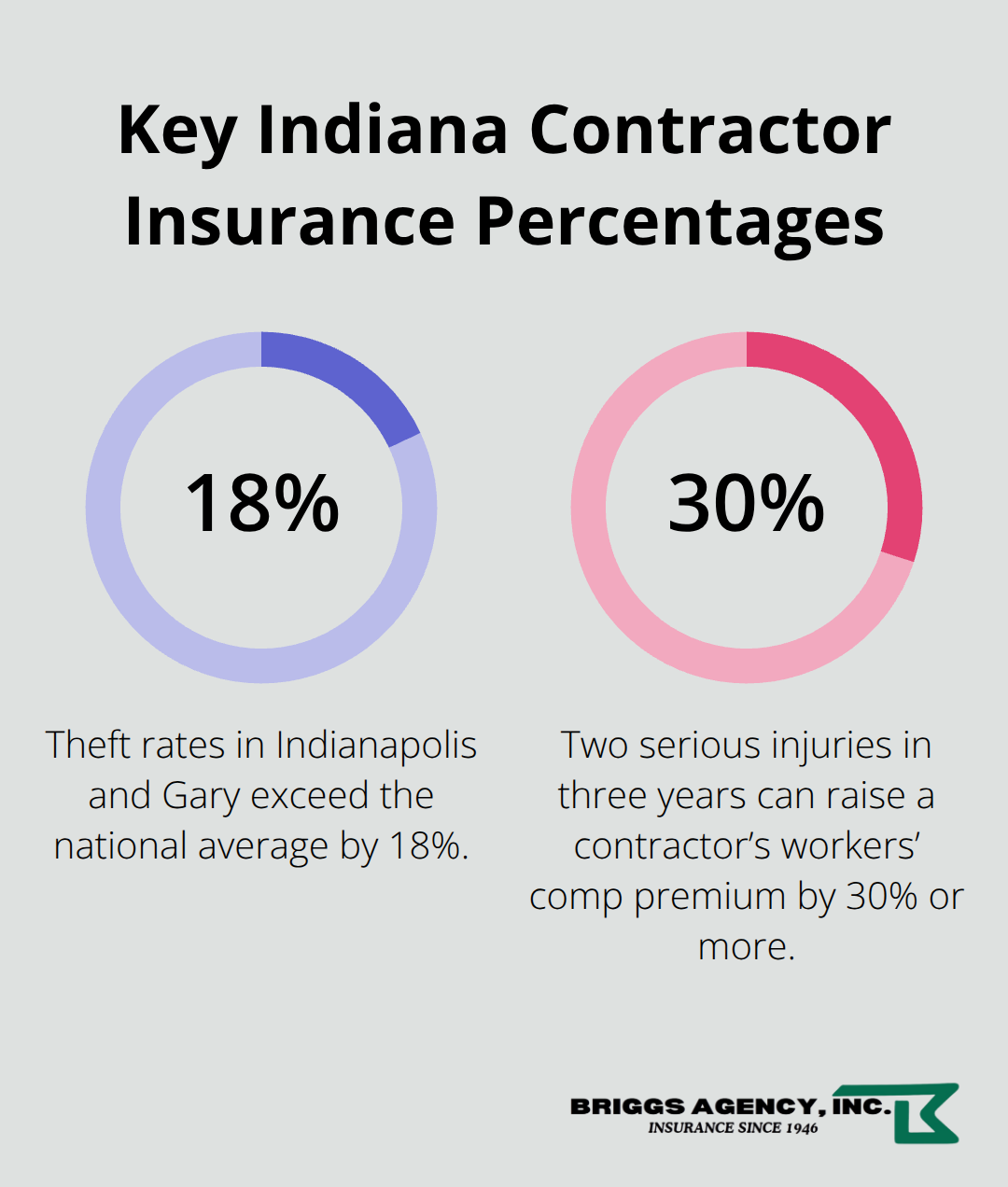

Tools and equipment theft is particularly common in Indiana’s construction sector, especially in the Indianapolis and Gary regions where theft rates exceed the national average by 18 percent, according to the National Equipment Register. Workers’ compensation rates in Indiana average 1.5 to 2.2 percent of payroll depending on your trade classification, making it essential to accurately report your crew size and job types to avoid audit surprises later.

Understanding these state-specific requirements sets the foundation for protecting your business, but knowing what coverage exists is only half the battle. The next section covers the essential policies that actually shield your operation from the financial damage that state minimums alone cannot prevent.

Essential Coverage Types for Contractors

General Liability Insurance Protects Against Common Claims

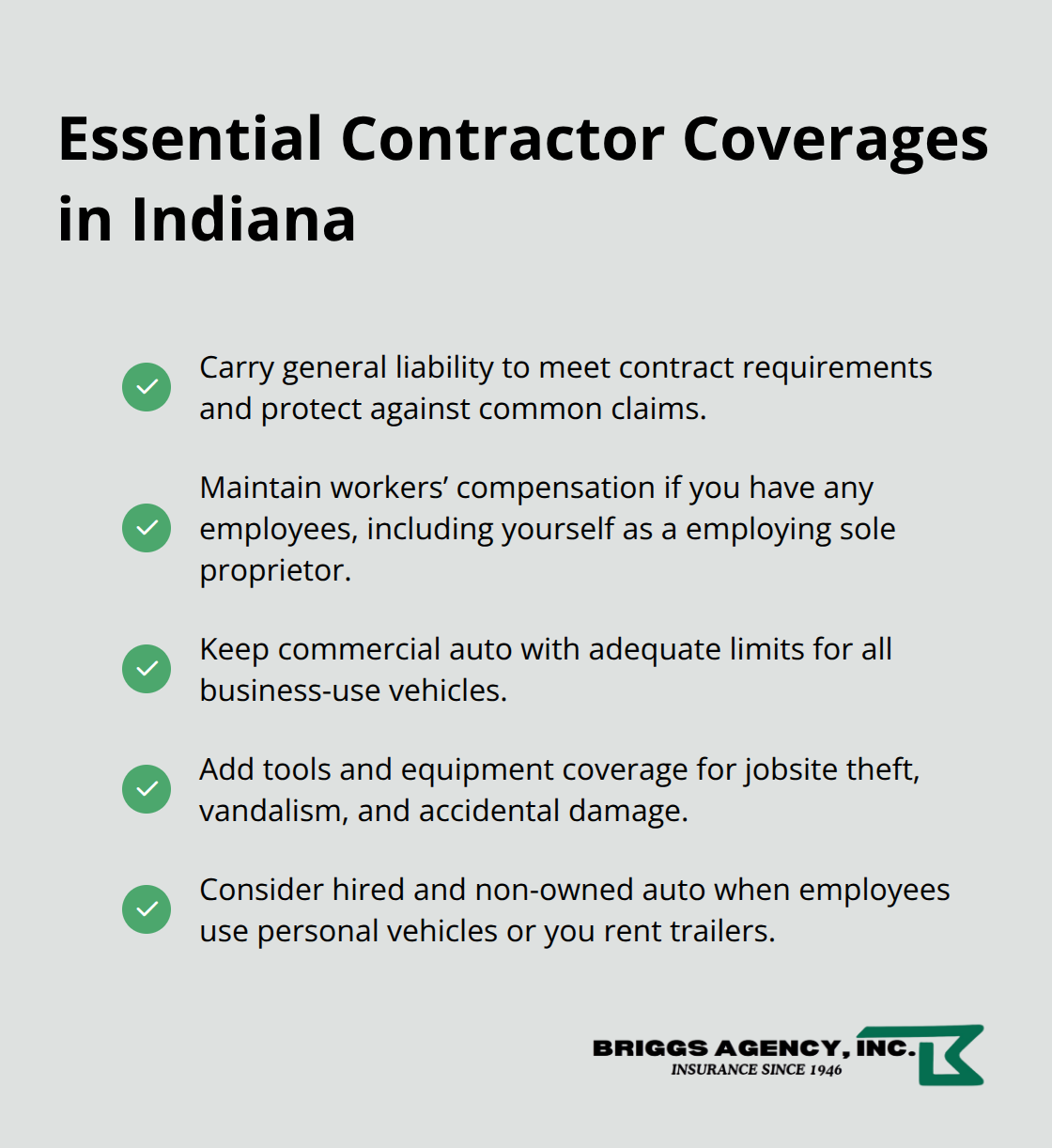

General liability insurance covers property damage and bodily injury claims that arise from your work, and Indiana courts award damages aggressively when contractors fall short. A roofing contractor who damages a homeowner’s gutters, a concrete finisher whose equipment injures a bystander, or a carpenter whose negligence causes water damage to adjacent properties all face claims that easily exceed $50,000. Your policy limit should match your project scope-contractors handling residential work typically need $1 million per occurrence and $2 million aggregate, while commercial projects often demand $2 million or higher. Many Indiana general contractors carry only $300,000 limits thinking it’s sufficient, then face uninsured exposure when actual damages run higher. Verify your limits against your signed contracts; clients increasingly require proof of specific coverage amounts before work begins.

Workers’ Compensation Covers Employee Injuries

Workers’ compensation becomes your largest controllable insurance expense once you hire employees. Indiana’s classification system assigns rates based on your specific trade and work type, meaning a framing contractor pays substantially more than a general superintendent because framers face higher injury risk. The state’s Workers’ Compensation Board publishes rates ranging from 0.8 percent of payroll for office staff to 4.5 percent or higher for heavy demolition work, and misclassifying your crew as lower-risk trades triggers audits that cost far more than the premium difference. If you run a crew of five carpenters, your annual premium runs roughly $35,000 to $55,000 depending on your safety record and experience modification rate. Your claims history directly affects this rate-two serious injuries in three years can increase your premium by 30 percent or more, making workplace safety programs financially mandatory, not optional.

Commercial Auto Insurance for Vehicle-Related Incidents

Commercial auto insurance differs sharply from personal auto policies and many Indiana contractors mistakenly use personal coverage for work vehicles, which voids claims. Indiana’s minimum requirement of $25,000 bodily injury per person provides almost no real protection-a single serious injury claim from a pedestrian struck by your work truck easily exceeds that limit. Try maintaining at least $100,000 per person and $300,000 per accident as standard practice, particularly if you operate multiple vehicles or transport employees. If your work involves hauling equipment or materials, add hired and non-owned auto coverage to protect yourself when employees drive their personal vehicles for business purposes or when you rent equipment trailers.

Tools and Equipment Coverage Prevents Financial Loss

Tools and equipment theft in Indiana costs contractors an average of $2,500 to $8,000 per incident according to National Equipment Register data, with Indianapolis and northwest Indiana experiencing particularly high theft rates. Standard commercial property policies exclude tools and equipment left at job sites, meaning a stolen $15,000 compressor or stolen power tools leave you absorbing the full loss unless you carry specialized coverage. Equipment floaters and contractors’ tools coverage run approximately 3 to 5 percent of the equipment value annually and typically include theft, vandalism, and accidental damage. Contractors who maintain detailed equipment inventories with serial numbers and photos reduce claim processing time from weeks to days when theft occurs. Understanding what each policy covers sets the stage for the next critical step: calculating what these policies actually cost and identifying where you can reduce premiums without sacrificing protection.

Cost Factors and How to Get Competitive Rates

What Affects Your Contractor Insurance Premium

Your contractor insurance premium hinges on five concrete factors that you can measure and control. Experience modification rate, or EMR, sits at the top of this list-Indiana’s Workers’ Compensation Board calculates your EMR based on your actual claims history compared to contractors in your classification, and a single serious claim can spike your rate by 15 to 40 percent for three years running. A clean safety record maintained over five years drops your EMR below 1.0, meaning you pay less than the standard rate for your trade. Revenue and payroll size matter directly because workers’ compensation premiums scale with total payroll dollars, so misreporting your crew size or deliberately underclassifying workers to reduce premiums triggers audits that cost thousands in back premiums plus penalties. Payroll audits for Indiana contractors frequently uncover thousands in owed premiums when crews were underreported.

Your specific trade classification determines your base rate-a masonry contractor pays roughly double what a general superintendent pays per payroll dollar because masons face higher injury risk. Loss history for general liability matters equally; two property damage claims in three years signals elevated risk to underwriters, and your next quote jumps 20 to 35 percent even if claims were minor. Finally, the amount of coverage you request affects pricing-requesting $5 million in aggregate limits costs substantially more than $2 million, but many contractors request inadequate limits then face uninsured exposure.

Common Mistakes That Drive Up Your Costs

Contractors frequently sabotage their own premiums through avoidable mistakes that inflate costs unnecessarily. Failing to report all employees and misclassifying workers stands as the costliest error-classifying a carpenter as a laborer saves perhaps $3,000 annually but triggers audit penalties exceeding $15,000 when discovered, and Indiana’s Department of Labor actively pursues these cases. Carrying duplicate coverage creates waste; many contractors maintain both a commercial general liability policy and a contractors’ liability policy simultaneously, paying for overlapping protection when one policy suffices.

Requesting inflated coverage limits you’ll never use adds 10 to 20 percent to your premium-a small residential remodeler requesting $5 million aggregate limits pays substantially more than one requesting $1 million when the actual risk profile demands the lower amount. Ignoring safety program investments means missing premium discounts of 5 to 15 percent that carriers offer for documented safety training, incident-free years, and written safety protocols. Comparing quotes from only two carriers leaves you blind to rate variations that commonly exceed 40 percent for identical coverage across different insurers.

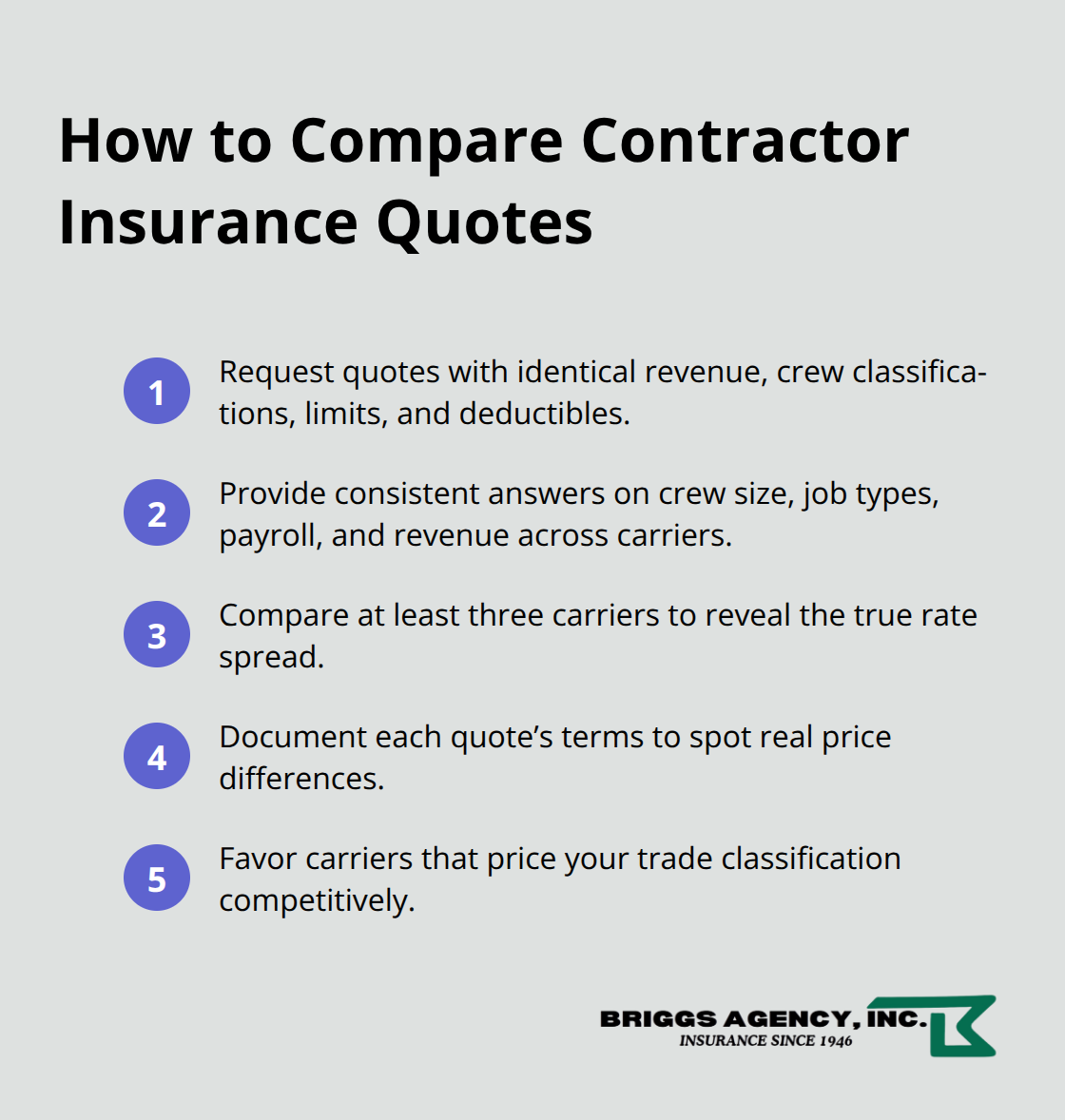

How to Compare Quotes from Multiple Carriers

Indiana contractors often pay 30 to 50 percent more than necessary simply because they accepted the first quote without shopping competitively. Accurate quotes require consistent information across all carriers-different answers about crew size, job types, or revenue between quotes invalidates comparisons and produces misleading pricing. Request quotes using identical specifications: same revenue figure, same crew classifications, same coverage limits, same deductibles. This approach reveals true rate differences and exposes which carriers view your risk profile favorably versus those that price aggressively for your trade.

Final Thoughts

Contractor insurance coverage in Indiana protects your team, your clients, and your ability to secure future projects. Verify that your current policies meet Indiana’s legal minimums for workers’ compensation and commercial auto coverage, then confirm your general liability limits match your actual project scope and contract requirements. Audit your crew classifications and payroll reporting to eliminate the audit risk that catches many contractors off guard.

The contractors who pay the least for insurance maintain clean safety records, accurately report their operations, and compare rates systematically across multiple carriers. Request quotes from at least three insurers using identical specifications for revenue, crew size, and coverage limits-this step commonly reveals 30 to 50 percent pricing differences for identical protection. A documented safety program and incident-free years qualify you for discounts that reduce your annual premium by thousands of dollars while lowering your actual risk profile.

We at Briggs Agency, Inc. help Indiana contractors identify coverage gaps, eliminate waste, and secure competitive rates from top-rated carriers. Contact us to review your current contractor insurance coverage Indiana and explore where you might be overpaying or underprotected.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.