Contractor General Liability Insurance: Why It Matters for Indiana Pros

Running a contracting business in Indiana means managing real risks every single day. One accident on a job site or property damage claim can threaten everything you’ve built.

Contractor general liability insurance protects you from these financial disasters. At Briggs Agency, Inc., we’ve helped countless Indiana contractors understand why this coverage isn’t optional-it’s essential.

What Your Coverage Actually Protects

Three Core Coverage Categories

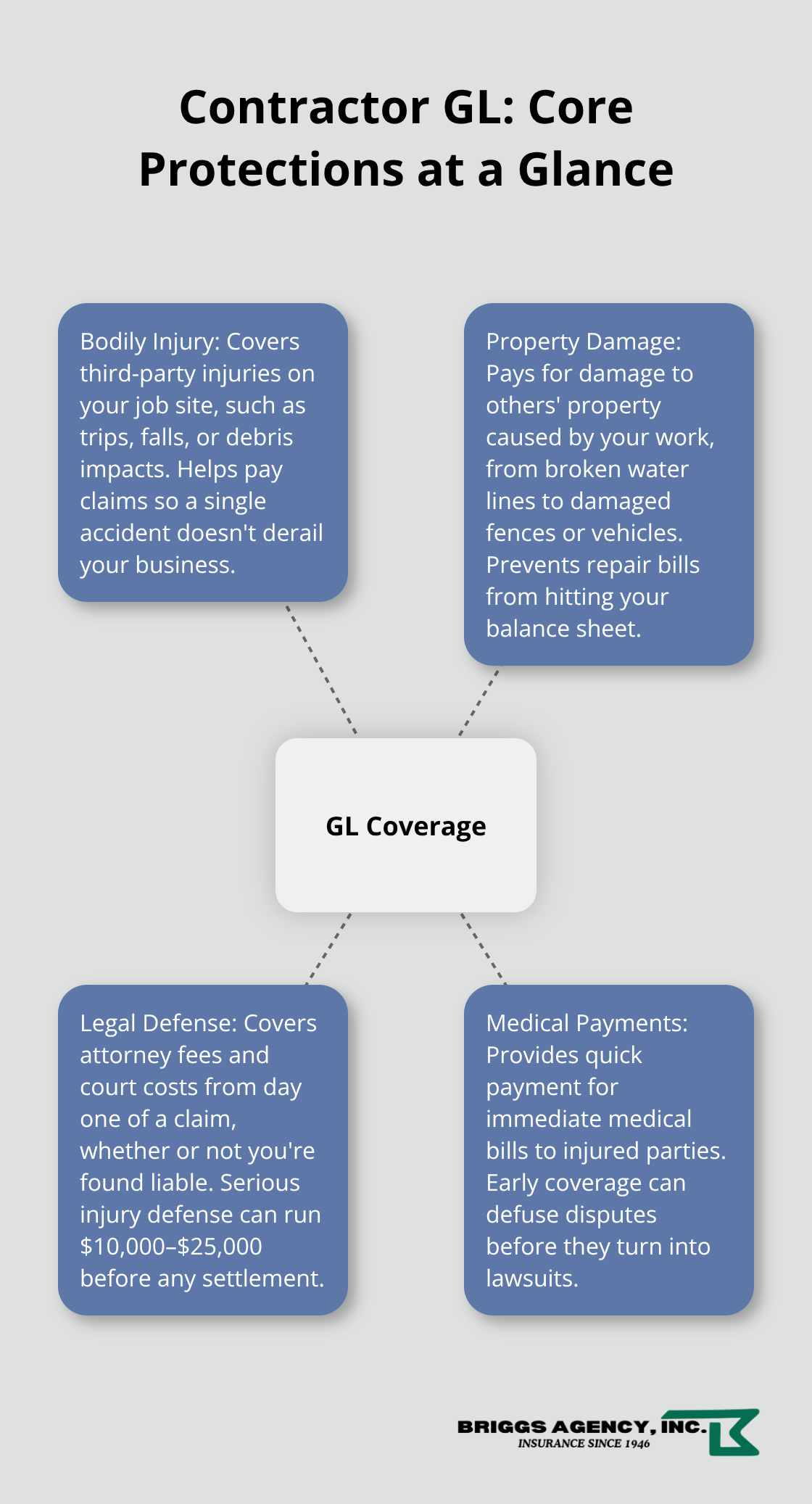

General liability insurance for contractors covers three categories of expenses that can sink your business if left uninsured. First, bodily injury claims arise when someone gets hurt on your job site-a worker steps on a nail, a client trips over your equipment, or a passerby is struck by debris. Property damage claims happen when your work damages something that isn’t yours-you accidentally drill through a water line, your crew damages a neighbor’s fence, or materials from your project damage a parked car. Second, your policy pays for legal defense costs the moment a claim is filed, regardless of whether you’re found liable. A serious injury lawsuit can cost $10,000 to $25,000 just in defense expenses, and that’s before any settlement or judgment. Third, medical payments coverage steps in quickly to cover immediate medical bills for injured parties, even if fault hasn’t been determined.

This small gesture often prevents minor incidents from becoming lawsuits.

Understanding Your Policy Limits

The limits you carry directly determine your financial exposure. Indiana public works projects mandate a minimum of $1,000,000 per occurrence and $2,000,000 in general aggregate coverage for all contractors on the job. For private projects, you’ll typically find that $1 million per occurrence is the baseline, though many commercial clients and larger projects require $2 million per occurrence with $4 million aggregate. A roofing mistake or improper demolition can easily exceed $50,000 in property damage repair costs, and serious bodily injury claims regularly reach six figures or more. Your policy covers both the damages awarded and the defense costs, but only up to your limits-exceeding them means paying out of pocket.

Adjusting Your Deductible and Coverage

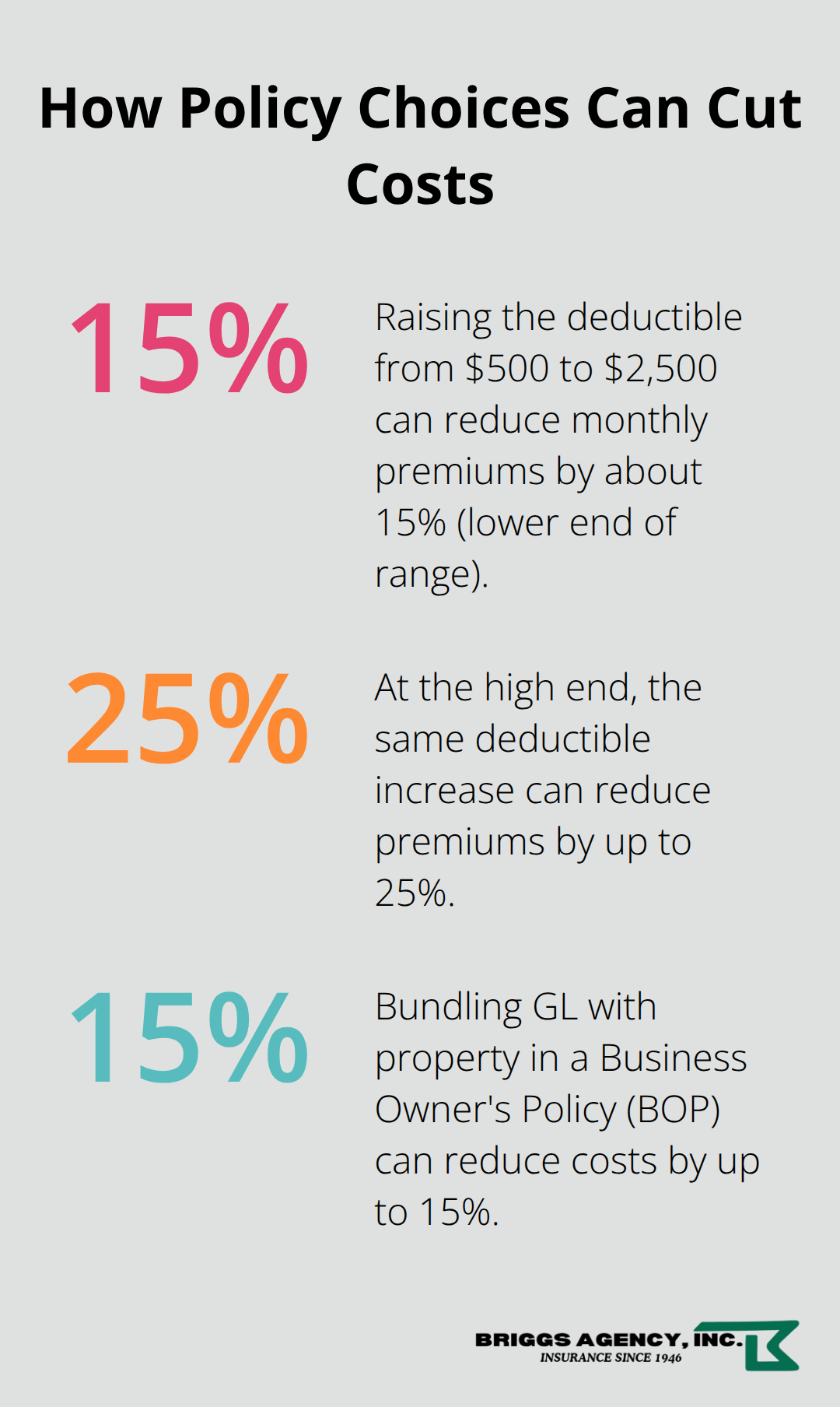

Increasing your deductible from $500 to $2,500 can reduce your monthly premium by 15 to 25 percent, but only take that step if you have adequate reserves to cover the higher out-of-pocket expense after a claim. For Indiana contractors, try starting with $1 million per occurrence and $2 million aggregate-this provides reasonable protection for most residential and light commercial work. Larger or more complex projects demand higher limits, and tailoring coverage to your specific exposure will shape what makes sense for your operation. Understanding these three coverage pillars helps you see why the right limits matter when a claim actually happens.

Why Indiana Contractors Must Carry This Coverage

Public Works Projects Demand Specific Minimums

Indiana public works projects require specific minimum coverage limits for every contractor on the job. If you bid on public work, you must provide written proof of these minimums before you can start. The state enforces these requirements uniformly across all contractor tiers, so there’s no negotiating around them. Private projects add their own demands: commercial clients commonly require $1 million per occurrence at minimum, and larger projects often demand $2 million per occurrence with $4 million aggregate. These aren’t arbitrary numbers-they reflect the real cost of serious incidents on job sites.

Local Licensing Authorities Set Their Own Rules

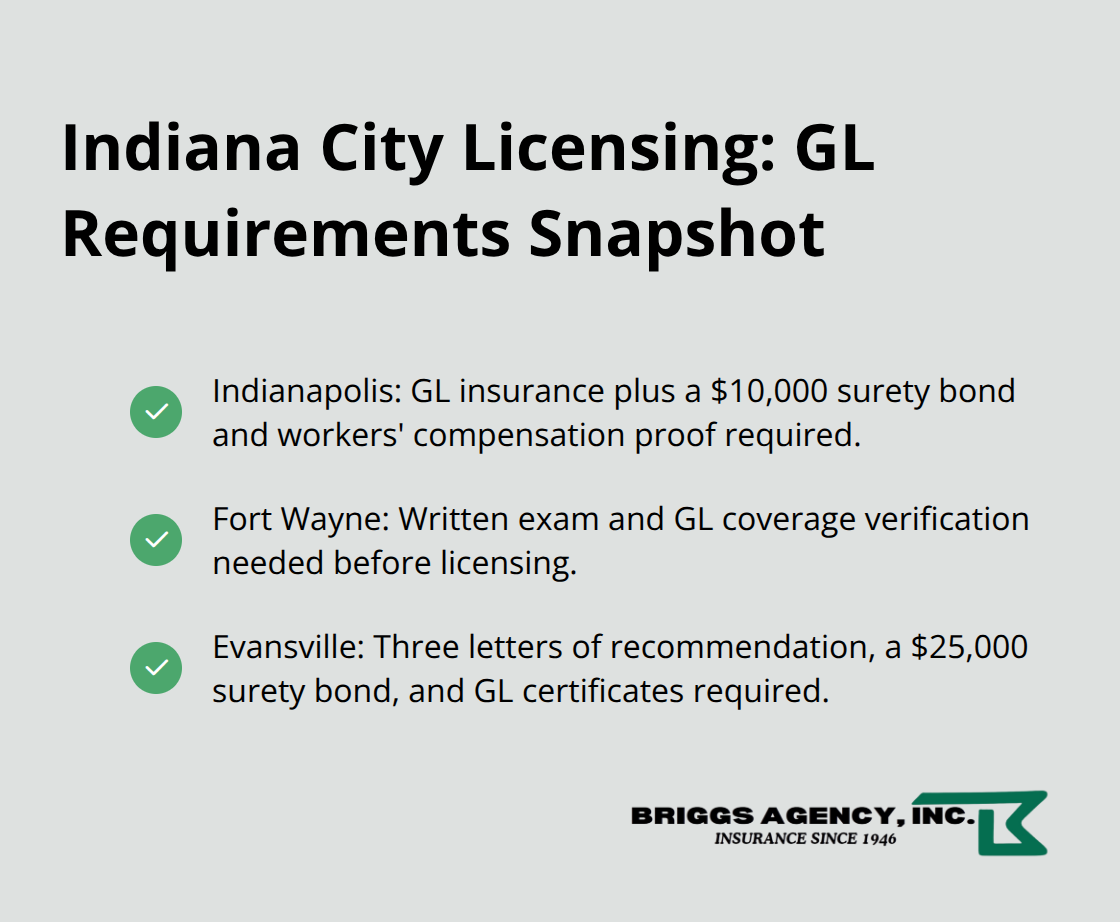

Each Indiana city controls its own contractor licensing process, and general liability insurance plays a central role in all of them. Indianapolis requires general liability insurance as part of your contractor license application, along with a $10,000 surety bond and workers’ compensation proof. Fort Wayne mandates a written exam and GL coverage verification before you receive your license. Evansville demands three letters of recommendation, a $25,000 surety bond, and GL certificates before you get licensed. These aren’t suggestions-they’re gatekeepers to legal work in your city.

You cannot operate without satisfying your local authority’s specific requirements.

Claims and Liability Exposure in Indiana

A serious bodily injury claim can easily exceed $100,000, and property damage from a single mistake routinely hits $50,000 or more. Without adequate limits, you pay personally for anything above your policy cap. Construction defect lawsuits in Indiana have a 10-year exposure window due to how state courts interpret faulty workmanship claims, meaning liability can follow you years after a project closes. That extended timeline makes higher limits essential-they cap your financial exposure at a specific number instead of leaving you vulnerable to six-figure judgments that arrive long after the work is done.

What Clients and Contracts Require

Your clients won’t hire you without proof of coverage. Most commercial leases, client contracts, and permit applications require a Certificate of Insurance listing your GL coverage before work starts. General contractors in Indiana typically carry $1 million per occurrence for residential and light commercial work, jumping to $2 million or higher for complex projects. If you provide design input, safety oversight, or construction consulting, you need professional liability coverage on top of general liability-defense costs alone for those claims run $10,000 to $25,000. Your coverage limits must match what your clients expect and what your actual work demands.

Pricing and Coverage Strategy

Monthly premiums for construction contractors in Indiana average around $281 according to MoneyGeek, though your actual rate depends on business size, claims history, and the specific services you offer. A solopreneur pays roughly $58 per month, but adding a fifth employee can boost premiums by 166 percent. Bundling general liability with property coverage into a Business Owner’s Policy can reduce costs by 10 to 15 percent and simplify management. The practical move: map your actual job-site exposure over the past three years, distinguish between residential and commercial work, note heavy equipment use and any design or safety responsibilities, then obtain quotes from at least three carriers familiar with Indiana’s statutes and local licensing rules.

The right coverage protects your business, satisfies your clients, and meets your city’s legal requirements-all at a price that fits your operation.

What Actually Happens When Claims Hit Your Job Sites

Immediate Job-Site Incidents and Medical Costs

The moment a serious incident occurs on your job site, your general liability policy becomes your financial lifeline. Slip-and-fall accidents happen constantly in Indiana construction-a worker steps into an unmarked hole, a subcontractor’s crew leaves equipment blocking a walkway, or a client visits the site and trips on exposed wiring. Medical bills pile up immediately: an ambulance call runs $500 to $2,000, emergency room treatment easily exceeds $5,000, and if surgery is needed, costs climb into the tens of thousands. Your medical payments coverage handles these bills without waiting for fault determination, which prevents minor incidents from escalating into lawsuits.

Property Damage Claims and Repair Costs

Property damage claims arrive just as fast and often cause more financial damage than bodily injury. A roofing crew accidentally punctures a water line during installation, causing $15,000 in foundation water damage to the home below. An improper demolition method damages the structural support of an adjacent building, triggering $75,000 in repairs and a third-party lawsuit. Your general liability policy covers the full cost of repairs, plus legal defense, but only up to your policy limits-which is why Indiana contractors carrying just $1 million per occurrence face serious exposure on larger commercial projects where a single mistake can cost $100,000 or more to fix.

Construction Defect Claims and Long-Tail Exposure

The real danger emerges years after a project closes. Indiana law gives property owners a 10-year window to file construction defect claims, meaning a faulty roof installation you completed in 2026 can result in a lawsuit hitting your door in 2036. These long-tail claims are expensive to defend because courts have expanded what counts as unintentional faulty workmanship, making it harder to avoid liability even when you followed standard practices. A completed operations claim for water intrusion or structural settling can cost $20,000 to $50,000 just to investigate and defend, and if the property owner wins, damages can exceed $200,000 for a residential project or $500,000 for commercial work. This extended exposure is precisely why higher limits matter-they protect you from personal liability for incidents that surface years later.

Professional Liability and Design Exposure

If you provide design input, safety consulting, or construction oversight, professional liability claims add another layer of risk that general liability alone does not cover. A contractor who recommends a structural approach that later causes settlement or cracking faces defense costs of $10,000 to $25,000 and potential damages far exceeding general liability limits. The combination of immediate job-site exposure and delayed construction defect risk makes adequate coverage non-negotiable for Indiana contractors serious about protecting their business.

Final Thoughts

Contractor general liability insurance stands as the foundation that protects your business when accidents strike. The incidents covered in this post-job-site injuries, property damage claims, and construction defect lawsuits-happen to Indiana contractors every year, and they cost real money. Without adequate coverage, a single serious claim wipes out years of profit or forces you to close your doors.

The financial stakes demand your attention. A $50,000 property damage claim, a $100,000 bodily injury lawsuit, or a $200,000 construction defect suit arriving years after project completion represents the claims that hit Indiana contractors regularly. Your general liability policy caps your personal exposure at a specific number instead of leaving you vulnerable to judgments that exceed your ability to pay. That protection matters far more than the monthly premium you’ll spend.

Review your current coverage limits against the actual exposure on your job sites, map your past three years of projects, and identify any design or safety responsibilities that might require professional liability coverage. Contact a local agent who understands Indiana’s specific requirements and can compare quotes from multiple carriers. We at Briggs Agency, Inc. have guided Indiana contractors since 1946, and our experienced local agents can help you find the right contractor general liability insurance at a competitive price.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.