Restaurant Insurance Indiana: Tailored Protection for Restaurants

Running a restaurant in Indiana means managing countless moving parts-from food safety to staffing to equipment maintenance. One critical element many owners overlook is having the right insurance coverage in place.

At Briggs Agency, Inc., we work with restaurant owners across Indiana who face unique risks that standard business policies simply don’t address. Restaurant insurance Indiana protects your business, your employees, and your customers when accidents or unexpected events happen.

What Coverage Do Indiana Restaurant Owners Actually Need?

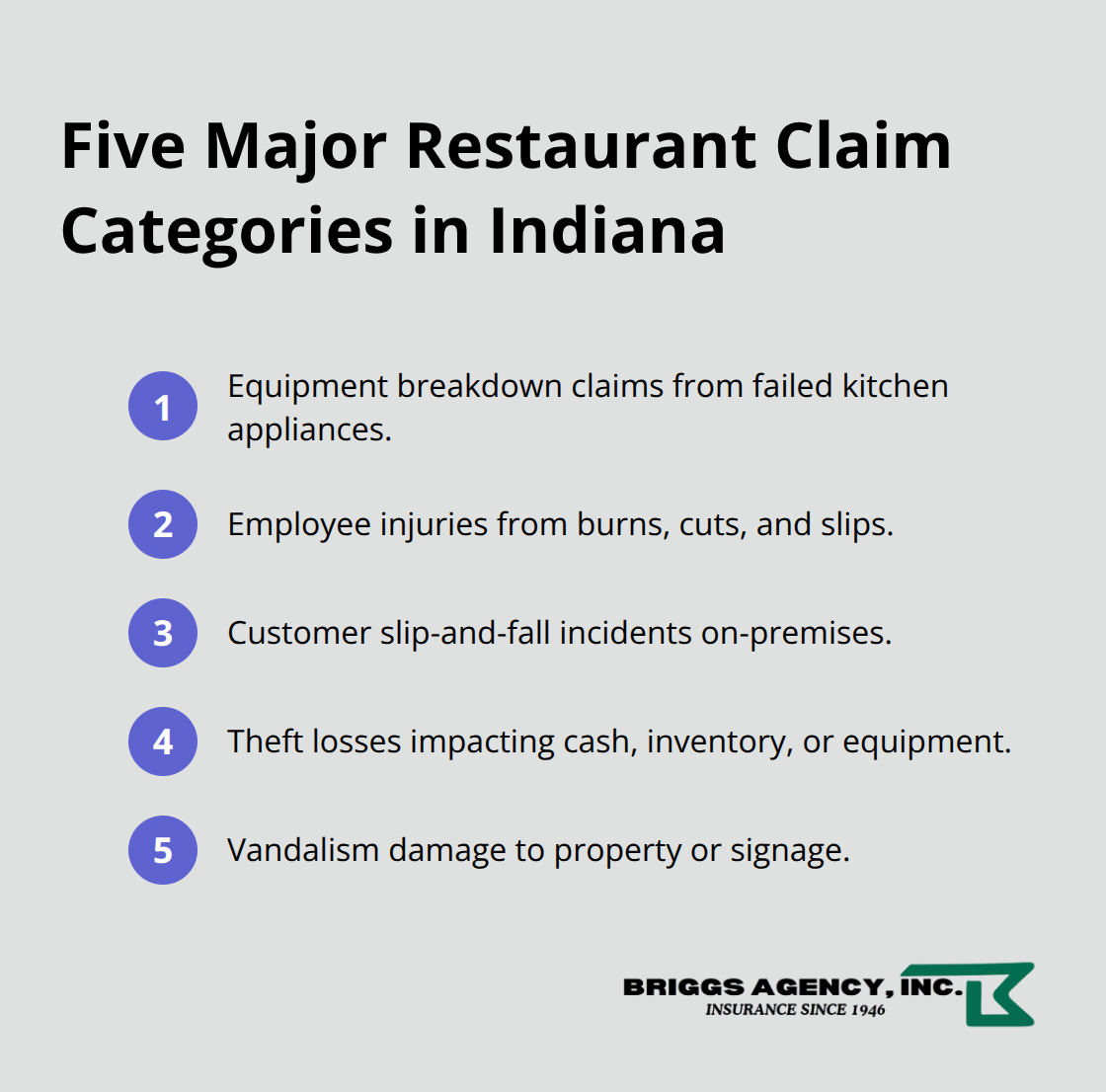

Restaurant owners in Indiana face five major claim categories that shape coverage decisions: equipment breakdown, employee injuries, slip-and-falls, theft, and vandalism. General liability insurance covers customer-facing risks-medical costs when someone gets hurt on your premises, plus advertising injuries like copyright claims. This protection typically includes limits of $1 million per occurrence and $2 million aggregate, which costs Indiana restaurant owners around $107 per month on average according to MoneyGeek data from 2026. Property insurance protects your building, equipment, and inventory from fires, natural disasters, and theft, and most landlords require it whether you own or lease your space.

Vehicle Coverage for Delivery Operations

If you deliver food or operate vehicles for business purposes, your personal auto policy won’t cover those activities, so commercial auto insurance becomes mandatory. You need coverage for hired and non-owned vehicles if you rely on third-party delivery services. This gap catches many restaurant owners off guard when a delivery driver causes an accident-your business faces liability exposure that standard policies explicitly exclude.

Workers’ Compensation and Incident Documentation

Workers’ compensation is required for any Indiana restaurant with employees and covers medical expenses, lost wages, and death benefits for dependents. Indiana law gives you two years from the injury date to file a claim, so accurate incident documentation matters immediately after an accident occurs. This window is tighter than many owners realize, making prompt reporting and detailed records essential for protecting both your employees and your business.

Equipment Breakdown and Business Interruption Protection

Equipment breakdown coverage specifically protects expensive kitchen appliances from costly repairs or replacements when refrigeration fails or power outages ruin perishable inventory. This isn’t included in basic property policies, yet it ranks among the top five claim drivers for restaurants. Business interruption coverage reimburses lost revenue when a covered event forces temporary closure-critical protection when a fire or equipment failure shuts down operations for days or weeks.

Liquor Liability and Additional Coverages

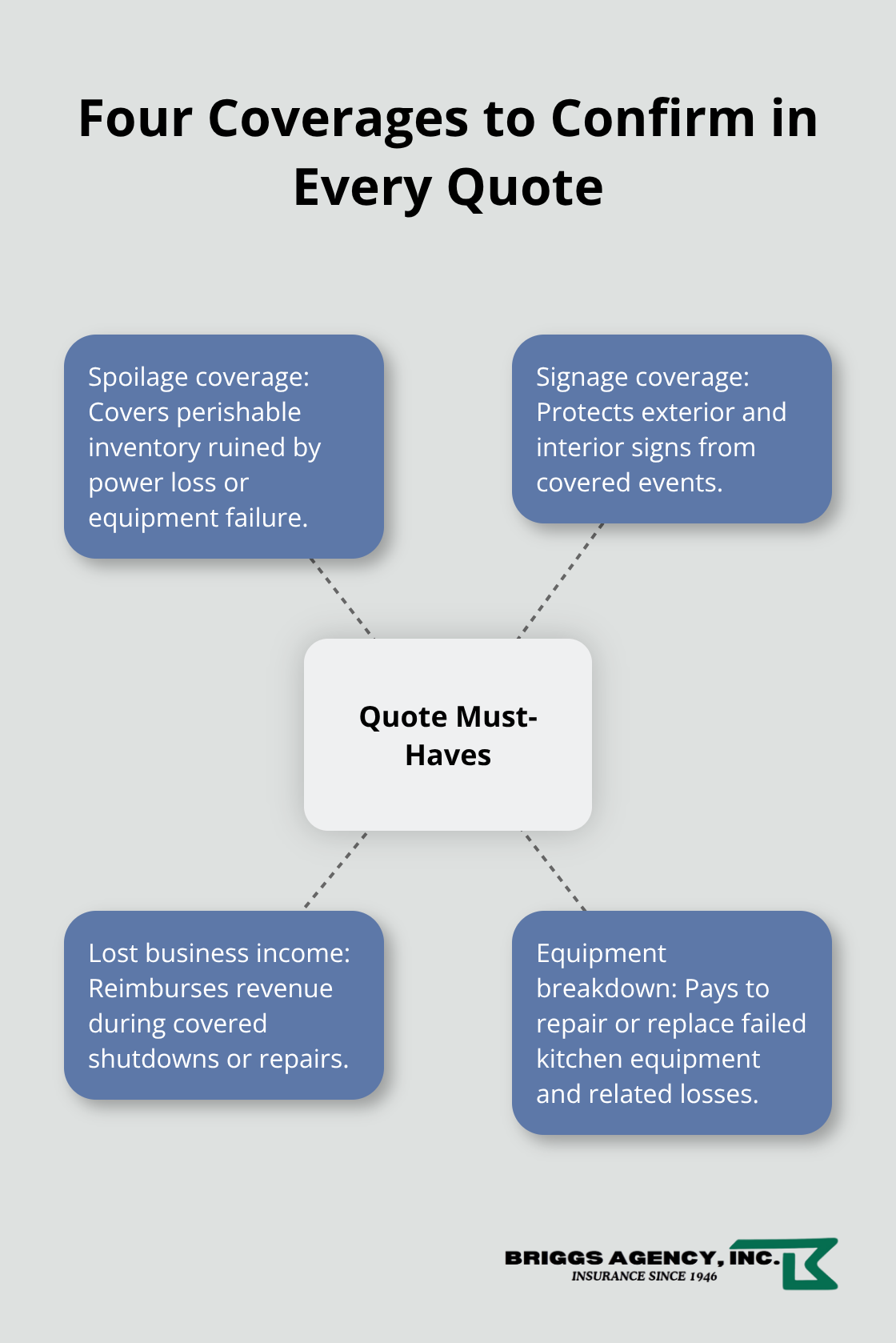

If your restaurant serves alcohol, liquor liability insurance is essential and now mandatory in Indiana with a $500,000 minimum requirement that took effect July 1, 2024. This coverage protects against claims from intoxicated patrons and covers legal defense costs, which matters because Indiana operates under Dram Shop laws that increase lawsuit likelihood. A Business Owners Policy (BOP) bundles property, general liability, and business interruption into one cost-effective package, often saving money compared to purchasing policies separately. Many Indiana restaurants also benefit from cyber liability coverage to protect customer payment data and online ordering systems, plus signage coverage for damaged exterior or interior signs after covered events.

With these core coverages in place, you’ve addressed the major risks that threaten restaurant operations. The next step involves identifying which provider can deliver the right combination of protection and local expertise for your specific situation.

What Puts Your Indiana Restaurant at Real Financial Risk

Slip-and-Fall Accidents: Your Most Preventable Threat

Slip-and-fall accidents represent the most preventable yet expensive threat to Indiana restaurants, and they happen far more often than owners expect. A wet floor in your dining room, grease near the kitchen line, or unsecured equipment creates immediate liability exposure-and customers pursue claims aggressively when they’re injured. General liability claims from slip-and-fall accidents typically fall within a $10,000 to $50,000+ range, which is why maintaining clear walkways, dry floors, and visible warning signage protects your bottom line. Kitchen hazards compound this risk because your staff faces constant exposure to burns, cuts, and slip hazards in tight spaces with high-pressure operations. Keeping walkways clear, floors dry, and signage visible prevents most incidents before they start, but general liability coverage catches what prevention misses.

Equipment Breakdown and Spoilage: Hidden Financial Drains

Equipment breakdown sits alongside slip-and-falls as a top-five claim driver for Indiana restaurants, and the financial impact strikes immediately and severely. When a refrigerator fails during summer heat or a power outage strikes, spoiled inventory and lost revenue total thousands of dollars within hours. Standard property policies exclude perishable inventory losses-a gap that catches owners off guard when they’re already scrambling to reopen. Equipment breakdown claims often cost more than the repair itself because you lose business income while equipment sits idle, making business interruption coverage equally important for restaurants that depend on continuous operations to stay profitable. Spoilage coverage protects against losses from refrigeration failures or power outages that ruin perishable inventory, addressing a risk that most basic policies ignore.

Food Contamination: Regulatory and Legal Exposure

Food contamination and foodborne illness claims carry different but equally serious financial exposure because they involve regulatory investigation, potential customer litigation, and reputational damage that extends beyond insurance payouts. A single outbreak traced to your kitchen triggers health department action, mandatory closure, and lawsuits from affected customers that take months or years to resolve. Your general liability policy covers some of this exposure, but the real protection comes from maintaining strict food safety protocols, training staff on proper handling and storage temperatures, and keeping detailed records of ingredient sourcing and preparation times. These practices reduce incident likelihood and demonstrate due diligence to regulators and insurers alike.

Fire Risk in Commercial Kitchens

Indiana tourism brought 83 million visitors to the state in 2024 with $16.9 billion in spending, which means your restaurant likely serves travelers and locals unfamiliar with your operations-increasing slip-and-fall risk from visitors who don’t know your layout. Fire risk in commercial kitchens demands serious attention because grease buildup, open flames, and high-heat cooking create conditions where fires spread rapidly and cause total loss of both building and equipment. Regular hood cleaning, functional fire suppression systems, and staff training on fire response reduce incident likelihood, but property insurance with adequate building and equipment limits remains your financial backstop when prevention fails. Understanding these specific risks shapes the coverage decisions you need to make next.

Selecting an Insurance Partner Who Gets Your Restaurant

Indiana’s insurance market includes 1,753 domestic and licensed foreign insurers, but most lack restaurant-specific expertise and underwriting knowledge. This abundance of options creates a practical problem: comparing quotes from generic business insurers wastes time because they misclassify your operation, miss industry-specific risks, and often decline coverage altogether when they realize you operate a kitchen with liquor service and delivery operations. You need an agency that understands the difference between dine-in revenue, takeout margins, and delivery risk exposure-distinctions that directly affect your premium and coverage adequacy.

Why Restaurant-Specific Expertise Matters

When you contact three insurers for quotes, insist on speaking with someone who has placed restaurant policies within the past twelve months, not a generalist who handles all small business types equally. Briggs Agency, Inc., a family-owned independent agency in Crown Point serving businesses since 1946, represents multiple top-rated carriers and compares options to tailor policies for Indiana restaurants. An agent with restaurant experience knows exactly which carriers specialize in food service, how underwriters evaluate spoilage risk, and which coverage gaps show up repeatedly in claims.

Comparing Quotes Across Multiple Carriers

The comparison process itself matters more than the initial quote price. Expect 30 to 50 percent price variation for identical coverage among different carriers according to MoneyGeek data, which means comparing only two quotes leaves you overpaying or underinsured. Request detailed quotes that specify coverage limits, deductibles, exclusions, and what’s included in any bundled Business Owners Policy versus standalone policies. Ask each carrier whether they cover spoilage, signage, lost business income, and equipment breakdown-the four coverages that separate adequate protection from inadequate policies.

Providing Accurate Information Upfront

Provide accurate information upfront: precise square footage, exact employee count broken down by role, annual revenue, whether you own or lease, specific cuisine type, delivery methods used, and alcohol service details. Misclassification kills deals during underwriting and delays coverage when you need it most. Clean underwriting information with precise details avoids the 30 to 50 percent price variation that results from carriers making different assumptions about your operation.

Calculating True Cost and Coverage Trade-Offs

Once you receive quotes, calculate the true cost per month including any monthly billing fees, because paying annually upfront saves 5 to 10 percent according to MoneyGeek, and raising your deductible from $500 to $2,500 cuts premiums by 15 to 25 percent if your business reserves can absorb a larger claim. The lowest price rarely delivers the best protection, so prioritize coverage that matches your actual risk profile over premium savings that leave you exposed. A policy that costs $20 less per month but excludes spoilage coverage exposes you to thousands in losses when equipment fails during peak season.

Final Thoughts

Restaurant insurance Indiana protects your business, your employees, and your customers when accidents or unexpected events disrupt operations. The coverage decisions you make today determine whether a slip-and-fall accident, equipment breakdown, or food contamination claim becomes a manageable loss or a financial catastrophe that threatens your restaurant’s survival. You now understand the five major claim categories that shape coverage decisions, the specific risks that hit Indiana restaurants hardest, and how to evaluate insurance providers who actually understand your operation.

We at Briggs Agency, Inc. have served Indiana businesses since 1946, and we specialize in restaurant insurance because we understand the unique risks you face. As a family-owned independent agency in Crown Point, we represent multiple top-rated carriers and compare options to deliver competitive pricing and the right protection tailored to your specific operation. Our experienced local agents know which carriers specialize in food service, how underwriters evaluate spoilage risk, and which coverage gaps show up repeatedly in claims.

Contact Briggs Agency, Inc. today to discuss your restaurant’s insurance needs with an agent who has placed restaurant policies within the past twelve months. Bring your square footage, employee count, annual revenue, and details about your service model-dine-in, takeout, delivery, or alcohol service-so we can request quotes from multiple carriers and compare coverage limits and deductibles. Three years of clean claims can yield meaningful reductions in renewal rates, potentially up to 20 percent, so the investment you make in proper coverage today pays dividends through lower premiums as your loss profile improves.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.