Small Garage Insurance Indiana: Scalability for Growing Shops

Running a garage in Indiana means managing more than just vehicles and tools. Your insurance needs change as your business grows, and a basic commercial policy often leaves you exposed.

At Briggs Agency, Inc., we’ve helped countless shop owners find small garage insurance in Indiana that actually keeps pace with their expansion. This guide walks you through the coverage gaps most garages face and how to build protection that scales with your success.

What Coverage Your Indiana Garage Actually Needs

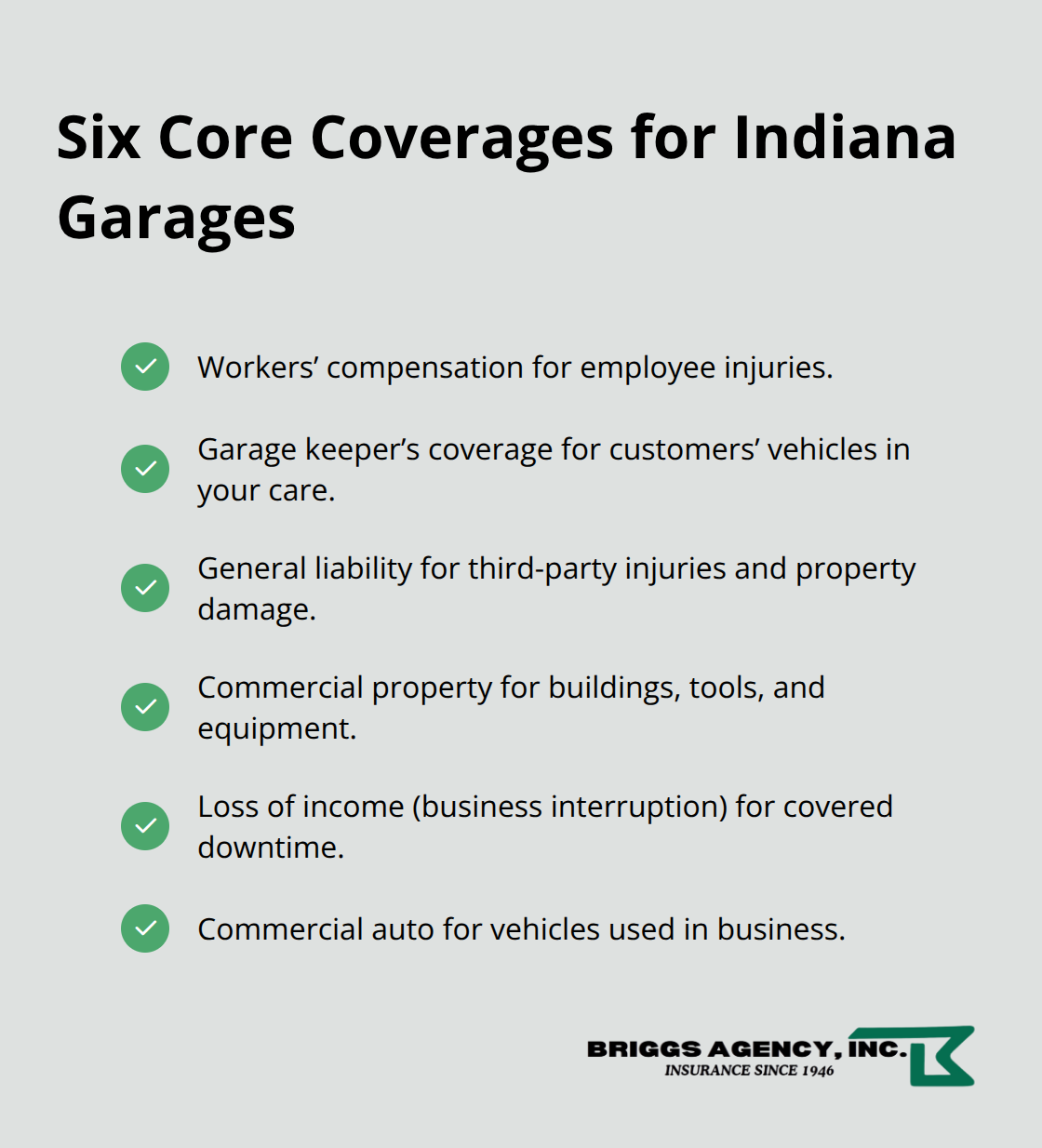

The Six Coverages That Protect Your Shop

Most garage owners in Indiana start with a standard commercial policy, then discover months later that it doesn’t cover the specific risks they face daily. Workers’ compensation protects your team-the U.S. Bureau of Labor Statistics recorded over 9,900 nonfatal injuries and illnesses in 2020 across the private automotive service sector, and your technicians face real exposure to burns, cuts, and back injuries. Garage keeper’s insurance is equally vital because it covers customer vehicles in your care from damage due to fire, theft, or accidents during service. Without it, a mechanic’s test drive that ends in a fender bender or a vehicle damaged by a shop fire leaves you personally liable. General liability covers the third-party claims you might face-if a customer slips in your shop or if your work causes property damage to someone else’s vehicle. Commercial property insurance protects your physical assets, tools, and equipment from fire, storms, theft, and vandalism. Loss of income insurance keeps your business afloat if a covered event like a fire temporarily shuts you down, covering payroll, taxes, and mortgage payments while you rebuild. Commercial auto insurance is mandatory if you own or use vehicles for business purposes, since personal auto policies explicitly exclude business use. These six coverages form the foundation that keeps your shop protected, and skipping any one of them creates exposure that grows exponentially as your business expands.

The Care, Custody, and Control Problem

A basic commercial policy typically excludes property damage to vehicles in your care, custody, or control-exactly what you need coverage for. This exclusion exists because standard policies assume you’re not handling customer property, but garages do nothing but handle customer property. Garage keeper’s coverage fills this gap by protecting customer vehicles regardless of whether your shop was at fault, though you can choose between legal liability coverage (which only pays if you’re negligent) or direct primary coverage (which pays regardless of fault).

What Indiana Garages Actually Pay for Insurance

The monthly cost for a small auto repair shop in Indiana ranges from about $39 to $89 depending on coverage type and risk profile, according to Nationwide. Many shop owners try to save money by choosing the lowest-cost option, only to face a $15,000 claim on a customer’s vehicle that their policy doesn’t cover. Indiana doesn’t mandate specific garage insurance under consumer protection law the way California does, but that doesn’t mean you can operate without proper coverage-it means you need to be proactive about protecting yourself.

Why Your Agent Matters More Than You Think

The difference between adequate coverage and inadequate coverage often comes down to whether you work with an agent who understands automotive operations or someone who just sells generic policies. An agent familiar with garage operations knows which exclusions create real exposure and which coverage options actually fit your daily work. When you’re ready to build a plan that scales with your growth, working with someone who speaks your language makes all the difference.

How Your Insurance Needs Change as Your Garage Grows

Your Coverage Shifts With Every Business Change

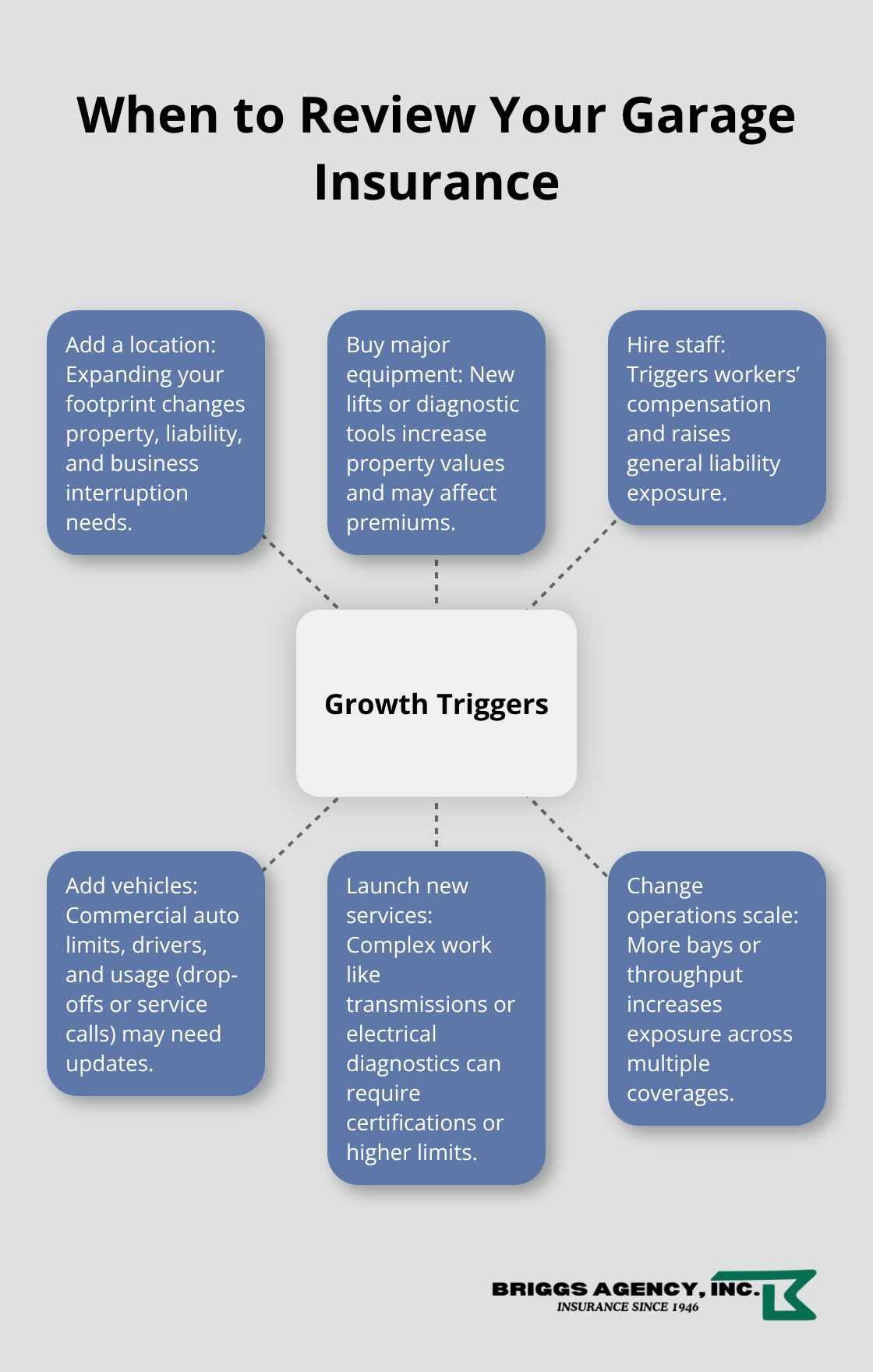

Your insurance costs and coverage requirements shift dramatically as you add vehicles, hire staff, and expand services. A shop with two technicians and a basic service menu faces entirely different risks than one with eight employees offering diagnostics, transmission work, and tire services. Premiums rise based on your coverage type, past claims history, total assets insured, and the number of employees and equipment at risk, according to Nationwide. When you add a second service bay or hire your first full-time technician, your exposure to workers’ compensation claims increases immediately-that’s not theoretical risk, that’s a direct line item in your policy. More equipment means higher commercial property insurance costs. More vehicles in your care means higher garage keeper’s exposure. More employees means higher general liability exposure when someone gets hurt or your work causes damage.

The Cost of Ignoring Growth

Most shop owners keep the same policy they bought two years ago while their business has fundamentally changed. Your insurance should reflect your actual operation, not your old one. This gap between your policy and your reality creates serious exposure that compounds with each expansion.

When to Review Your Coverage

The practical approach is reviewing your coverage every time you make a significant business change: adding a location, purchasing a lift or diagnostic equipment, hiring new staff, or launching a new service line. When you add vehicles to your fleet, your commercial auto insurance needs adjustment-especially if those vehicles are used for customer drop-offs or service calls. When you hire your first employee, workers’ compensation becomes non-negotiable in Indiana, and your general liability exposure jumps because you’re now liable for their actions and safety.

When you expand into services like transmission rebuilds or electrical diagnostics, some carriers may require additional training certifications or charge higher premiums due to increased complexity and potential liability.

Getting the Right Rate for Your Expanded Shop

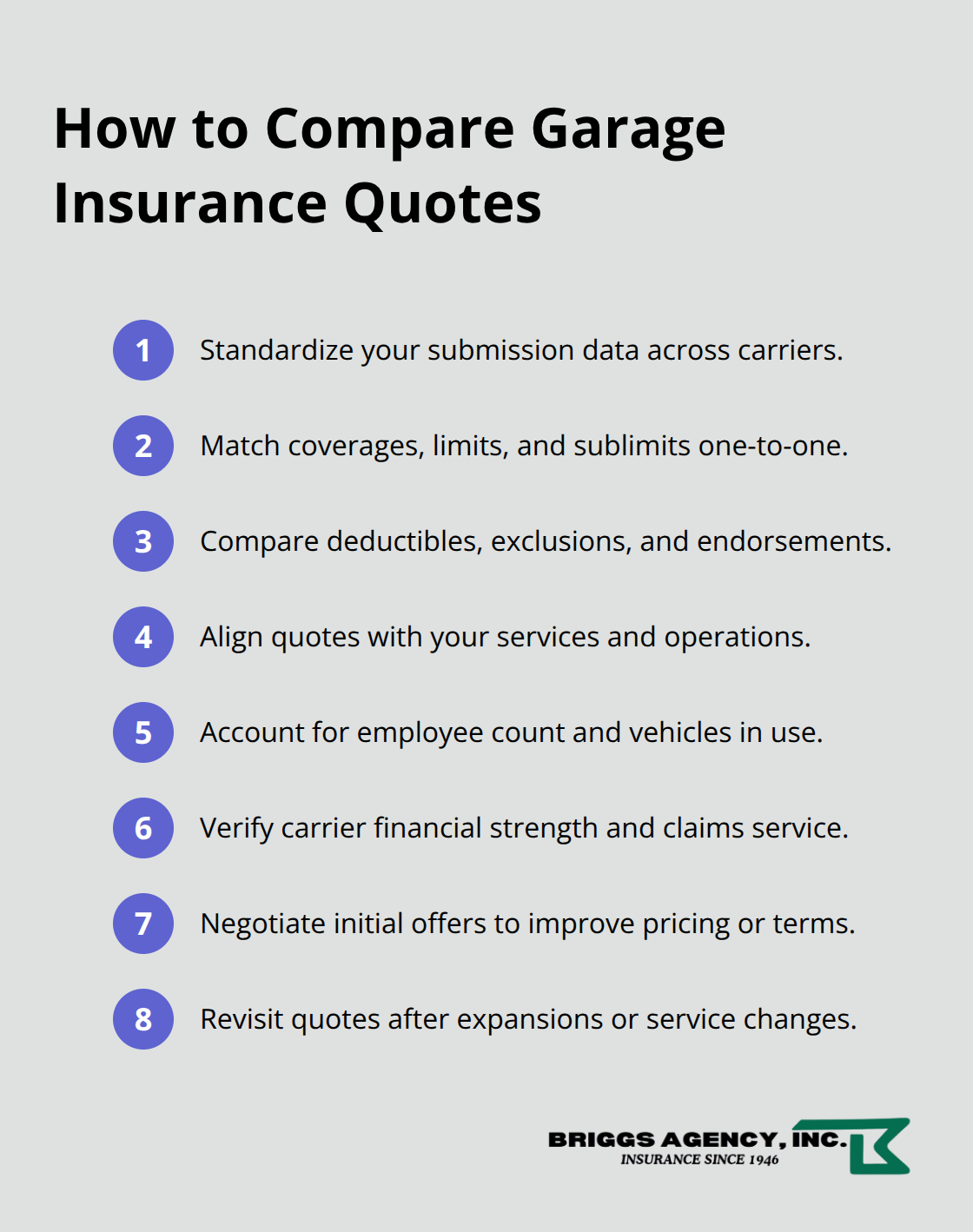

Getting multiple quotes when your business changes is critical because rates vary significantly between carriers and coverage tiers. Don’t settle for the first quote after an expansion-shop around to ensure you’re not overpaying for coverage you’ve outgrown or underpaying for protection you actually need. As your shop grows, more comprehensive policies become necessary to reflect your increased exposure from more vehicles, staff, and assets.

The question isn’t whether your coverage needs adjustment-it’s whether you’ll catch those gaps before they cost you thousands. Finding an insurance partner who understands automotive operations and stays proactive about your changing needs separates shops that grow safely from those that face unexpected exposure.

Finding the Right Insurance Partner for Your Garage

What to Look for in an Insurance Agent

The agent you choose matters more than the carrier you select. A good agent catches gaps in your coverage before they become expensive problems; a mediocre one sells you a policy and disappears. When you evaluate potential insurance partners, look for someone with direct experience in automotive operations, not someone who treats your garage like any other small business. An agent who understands garage operations knows that a test drive creates different liability exposure than regular shop work, knows which coverage exclusions actually matter to you, and knows that your insurance needs shift fundamentally when you add a second location or hire your tenth employee.

Ask potential agents specific questions about garage keeper’s coverage options, workers’ compensation requirements for Indiana shops, and how they handle coverage adjustments during expansion. If an agent cannot explain the difference between legal liability and direct primary garage keeper’s coverage without reading from a script, they don’t understand your business well enough to protect it effectively.

Getting Multiple Quotes and Comparing Them

Rates for garage insurance vary dramatically between carriers based on coverage type, claims history, total assets, and employee count, so accepting the first quote leaves money on the table. When you request quotes, provide identical information to each carrier so you can make accurate comparisons-don’t let one agent quote you basic coverage while another quotes comprehensive protection.

After you receive quotes, negotiate. Insurance companies build negotiating room into their initial offers, and an agent who won’t push back on pricing isn’t advocating for your business. As your shop expands into new service lines or adds locations, your coverage should expand too, which means revisiting quotes periodically rather than assuming your current rates remain competitive.

Staying Proactive as Your Business Changes

Your coverage needs shift with your operation, so your insurance partnership must shift with them. An agent who understands this reality stays in touch as your shop grows and proactively suggests coverage adjustments before you face exposure. When you add equipment, hire staff, or launch new services, your agent should flag the coverage implications and help you adjust your policy accordingly.

Working with a local agent who understands Indiana’s specific business environment and regulatory landscape ensures your coverage aligns with state requirements and local market conditions rather than generic national standards that may not apply to your operation. An independent agency that represents multiple top-rated carriers can compare your actual options and find coverage that fits both your risk profile and your budget without settling for inadequate protection.

Final Thoughts

Your garage’s insurance needs shift as you hire staff, add equipment, and expand service offerings. The shops that grow sustainably treat small garage insurance in Indiana as a living part of their business strategy, not a checkbox they completed years ago. Workers’ compensation, garage keeper’s, general liability, commercial property, loss of income, and commercial auto coverage form the baseline protection every Indiana garage needs, but baseline protection falls short once your operation expands.

An agent who understands automotive operations catches coverage gaps before they become expensive problems. They know that adding a second location changes your commercial property exposure, that hiring your first employee makes workers’ compensation non-negotiable, and that launching electrical diagnostics services may require coverage adjustments or carrier approval. They stay proactive rather than reactive, flagging coverage implications before you face exposure.

When you’re ready to review your coverage or build a plan for your expanding operation, reach out to our experienced local agents who understand what it takes to protect a growing garage.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.