Contractor Workers Compensation Indiana: What You Need to Know

Running a contracting business in Indiana means understanding your legal obligations around worker protection. Contractor workers compensation isn’t optional-it’s a requirement that protects both you and your team when injuries happen on the job.

At Briggs Agency, Inc., we’ve seen too many contractors operate without proper coverage or with gaps that leave them exposed to serious liability. This guide walks you through what Indiana requires, what your coverage should include, and the mistakes that cost contractors money.

What Workers Compensation Actually Means for Indiana Contractors

Worker compensation in Indiana is a mandatory insurance system that pays medical bills and lost wages when someone gets injured on the job, regardless of who caused the accident. Indiana Code Title 22, Article 3 requires most employers-including contractors-to carry this coverage. The system operates as a trade-off: employees give up their right to sue their employer for negligence, and in return they receive guaranteed benefits without having to prove the employer was at fault. This matters because construction and contracting work carries real injury risk. According to the Bureau of Labor Statistics, construction workers experience injuries at rates significantly higher than the national average, with roughly 1 in 10 construction workers experiencing a work-related injury annually. For contractors in Indiana, this isn’t theoretical. The law treats you as responsible for your workers the moment they start their shift, and penalties for operating without coverage run steep-Indiana Department of Labor enforcement has resulted in substantial fines for employers who misclassify workers or skip coverage entirely.

Understanding Indiana’s Classification Rules

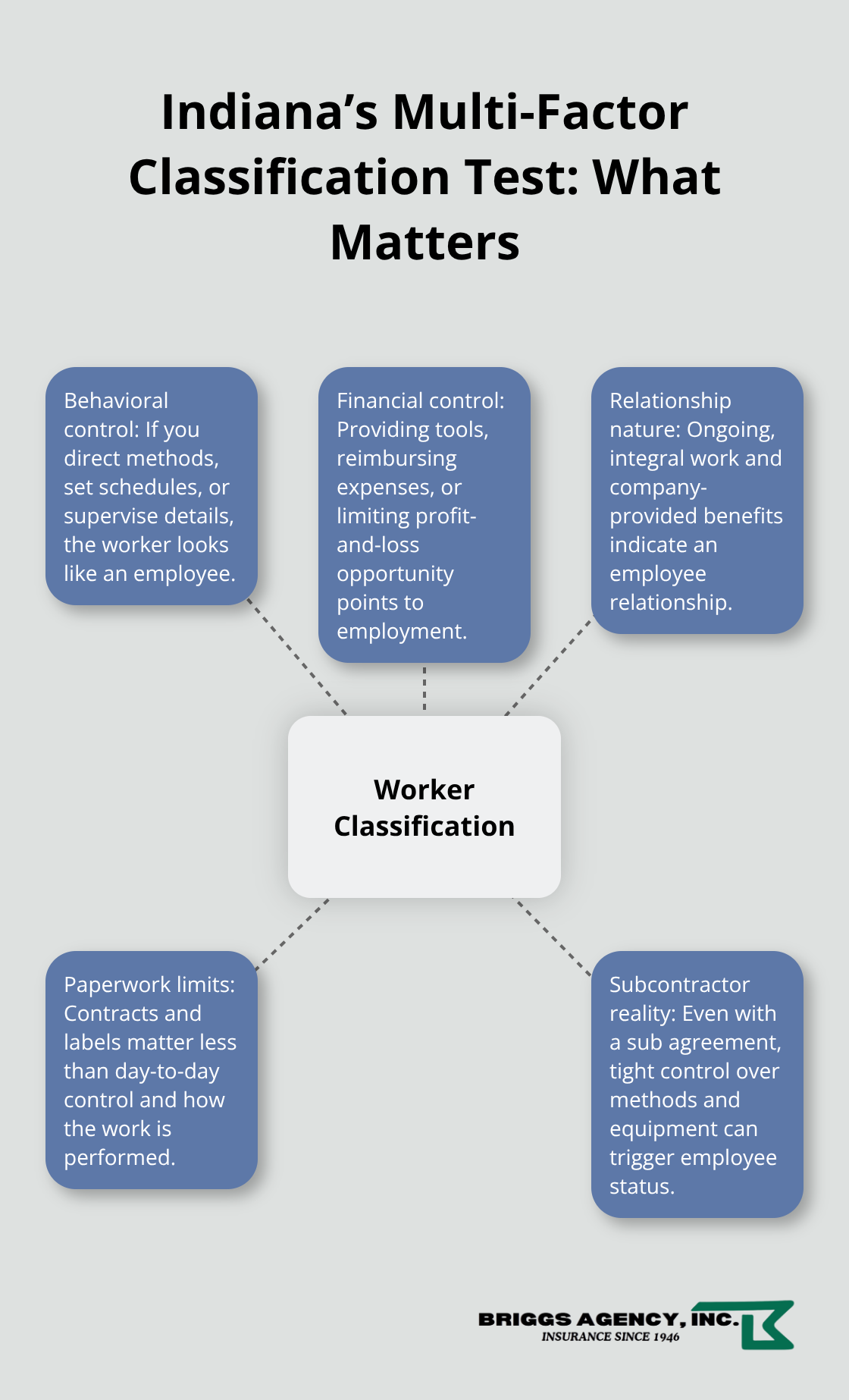

Indiana uses what’s called a multi-factor common-law agency test to decide whether someone counts as an employee or independent contractor-and this distinction directly affects your coverage obligations. The test examines behavioral control, financial control, and the relationship itself. No single factor wins the decision. A general contractor who tells a subcontractor exactly how to perform tasks, provides equipment, and maintains an ongoing relationship will likely be classified as the subcontractor’s employer, regardless of what the contract says.

This is where many Indiana contractors stumble.

The Clearance Certificate Process

Senate Enrolled Act 576 created a clearance certificate process that allows independent contractors to document their status with the Indiana Department of Revenue. The certificate only protects you if the relationship genuinely qualifies under the test-slapping a certificate on an employee relationship won’t shield you from liability. If an injury occurs and a worker challenges their classification, the Indiana Workers’ Compensation Board examines the actual working relationship at the time of injury, not just paperwork. Sole proprietors and partners can elect coverage as employees if they choose, but that election requires written notice to your carrier.

What Happens When Classification Gets Challenged

When a worker files an injury claim and disputes their classification status, the Board doesn’t rely on contract labels or certificates alone. Instead, investigators look at how the relationship actually functioned on the job-the instructions given, the tools provided, the payment structure, and the nature of the work itself. A contractor who maintains tight control over work methods and schedules faces a much harder time proving independent contractor status, even with paperwork in place. The consequences of misclassification extend beyond the injured worker’s claim. If the Board determines you misclassified an employee, your company becomes liable for all workers’ compensation benefits, and if you failed to carry insurance, you may face additional remedies and penalties from the state.

Moving Forward With Proper Classification

Getting your worker classification right from the start protects your business and your team. The next section covers the specific coverage options available to Indiana contractors and what protection each type actually provides when injuries happen.

Coverage Options and What They Protect

Medical Benefits Cover All Work-Related Treatment

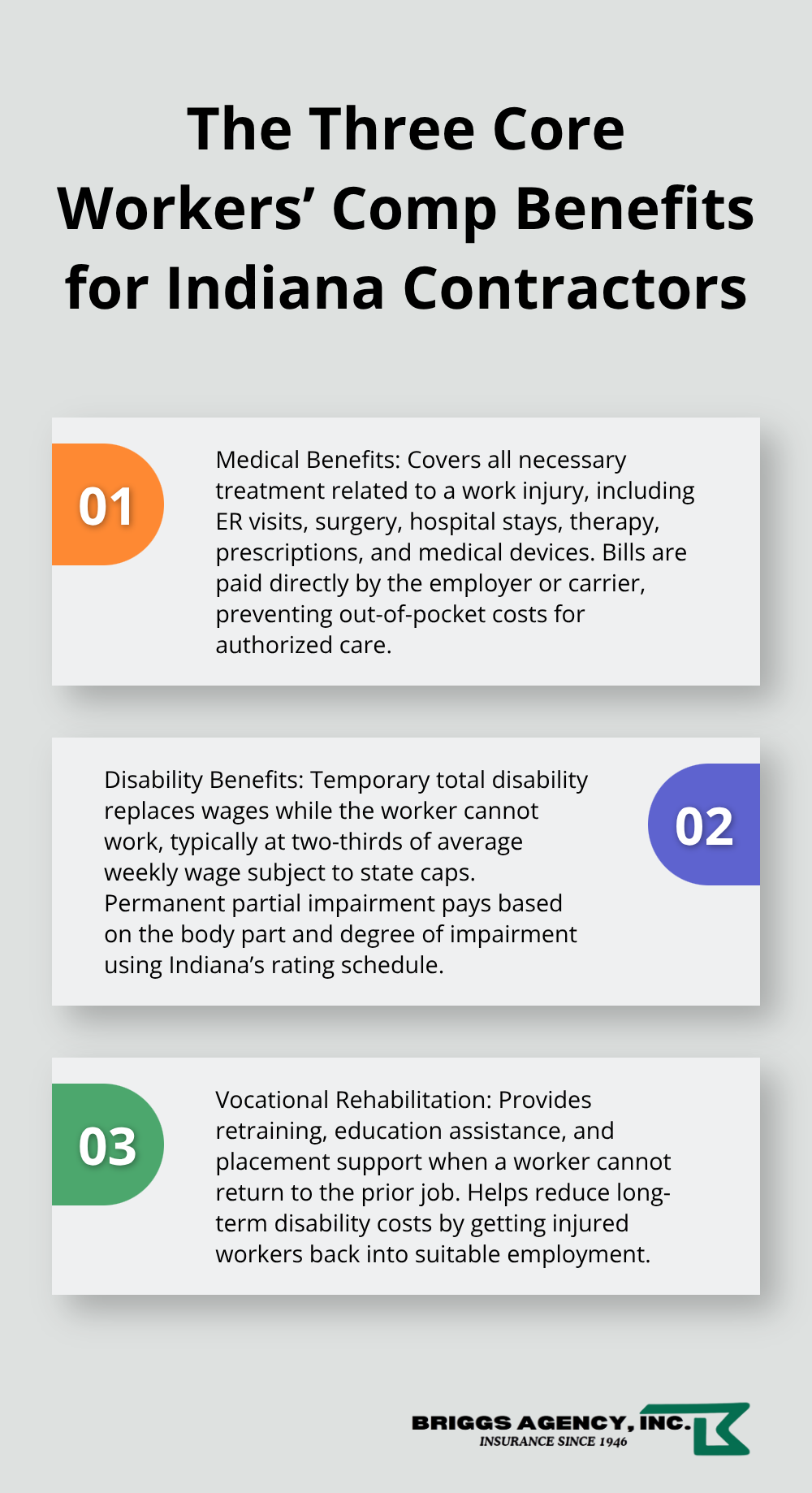

When an injury happens on a job site, workers compensation in Indiana covers three distinct areas, and understanding what each covers prevents surprises when claims get filed. Medical benefits cover all necessary treatment related to the work injury-emergency room visits, surgeries, hospital stays, physical therapy, prescription medications, and medical devices. The employer or their insurance carrier pays these bills directly to providers, and the injured worker avoids out-of-pocket costs for authorized care. Indiana law requires you to authorize treatment through a physician of your choice initially, then the insurance carrier manages ongoing care.

Temporary and Permanent Disability Benefits Replace Lost Income

Temporary total disability benefits replace lost wages while the worker recovers and cannot work. Indiana pays two-thirds of the worker’s average weekly wage, up to a maximum that adjusts annually. For 2024, that maximum sits at around 120 percent of the state’s average weekly wage, which means high-earning contractors’ workers receive partial income replacement rather than full wage replacement.

Permanent partial impairment compensation applies when a worker recovers but sustains lasting damage-a lost finger, reduced hearing, or chronic pain that affects future earning capacity. The Board calculates these payments based on the body part affected and the degree of impairment, using a formal rating schedule.

Vocational Rehabilitation Helps Workers Return to Employment

Vocational rehabilitation services step in when an injured worker cannot return to their previous job. These services include job retraining, education assistance, and placement support to help workers transition into roles they can physically perform. Indiana contractors rarely discuss this benefit, but it reduces long-term disability costs because workers move back into productive employment rather than remaining on permanent disability payments.

Documentation Determines Whether Claims Process Smoothly

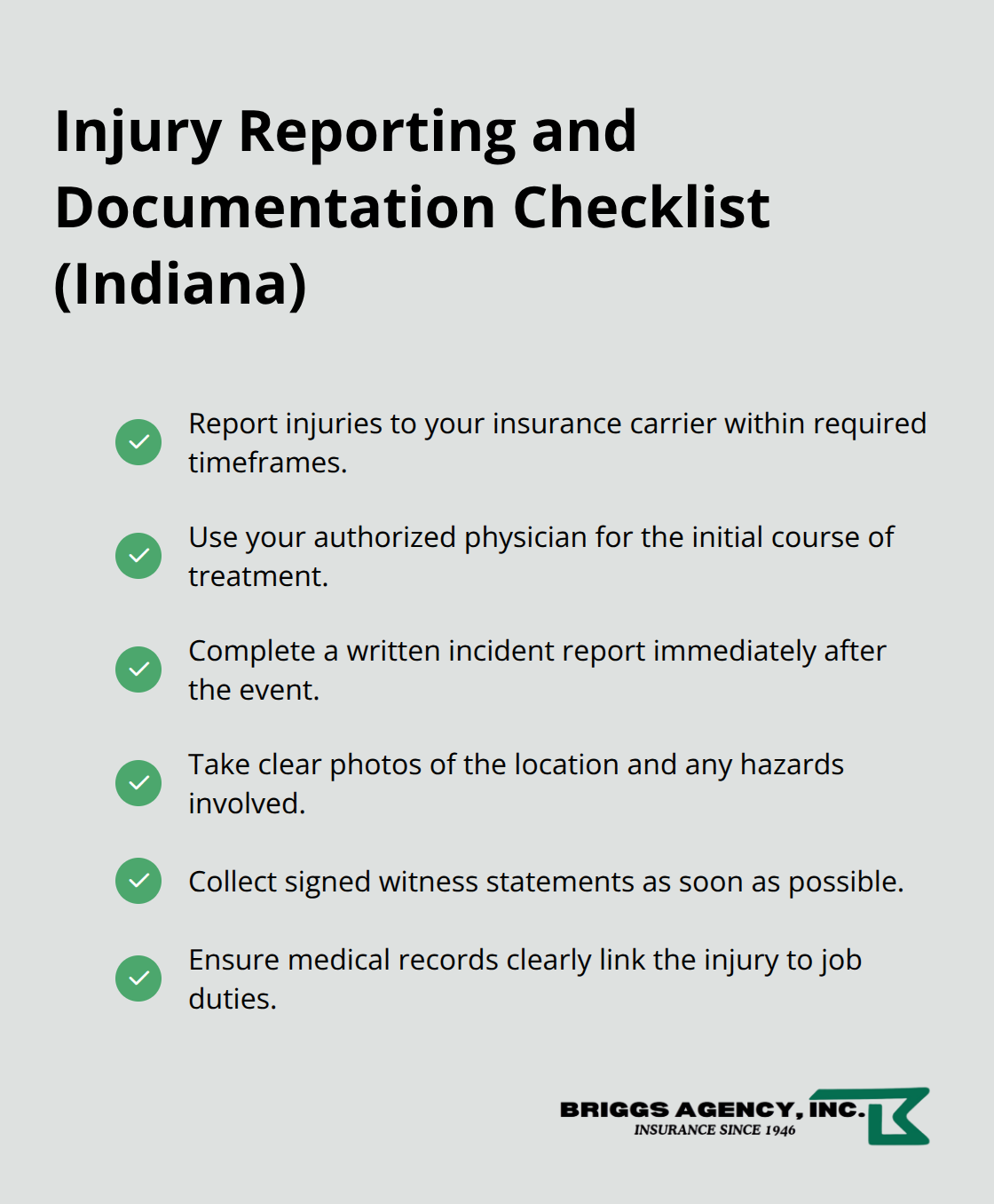

The National Council on Compensation Insurance, which sets the framework for workers comp premiums and coverage, emphasizes that proper claim documentation determines whether benefits get paid smoothly or face delays and disputes. When your worker gets injured, immediate notification to your insurance carrier matters enormously-most Indiana policies require notice within 24 hours of a serious injury or within a reasonable timeframe for minor injuries. Delays in reporting give insurers legitimate reasons to question claim validity.

Medical records must clearly link the injury to job duties; vague descriptions like general back pain without documentation of how the injury occurred create friction during claims processing.

Subcontractor Coverage Gaps Create Liability for General Contractors

Subcontractors complicate coverage because general contractors remain liable for coverage gaps when subs lack proper insurance or clearance certificates. The Basic Manual used by insurers requires satisfactory evidence of subcontractor coverage before work begins-a Certificate of Insurance, Certificate of Exemption, or the sub’s workers compensation policy. Missing documentation means your policy’s premium includes charges for uninsured workers, and audits within three years of the policy period can reveal gaps that trigger additional premium assessments. Establishing a simple injury reporting protocol before problems happen protects both the worker’s claim and your company’s coverage-a written form employees complete immediately, photographs of the incident location, and statements from witnesses all strengthen your position when claims arise. These documentation practices also matter when disputes over worker classification emerge, which happens more often than most contractors expect.

Where Contractors Go Wrong with Workers Comp

Misclassifying Workers Costs You Everything

Misclassification of workers as independent contractors in Indiana stands out as the single most costly mistake Indiana contractors make, and it’s not always accidental. The Indiana Department of Labor treats misclassification seriously because it directly undermines worker protections and shifts liability costs to your business. When an injured worker challenges their classification, the Workers’ Compensation Board examines the actual working relationship at the time of injury, regardless of what paperwork says. If you control how someone performs their work, provide their tools and equipment, maintain an ongoing relationship, and the work is central to your business, that person is almost certainly an employee under Indiana law. The multi-factor test doesn’t care about contract language or job titles.

One contractor in the construction sector might argue a framing crew consists of independent contractors, but if those framers work exclusively for that contractor, show up at scheduled times, use company equipment, and follow detailed instructions on how to frame walls, the Board will classify them as employees. The financial consequences run severe. Once misclassification is proven, your company becomes responsible for all workers’ compensation benefits retroactively, plus potential penalties from the state. If you failed to carry insurance during that period, you face additional liability and remedies against your business.

The Clearance Certificate Doesn’t Protect Bad Classifications

The Indiana Department of Revenue processes clearance certificates under Senate Enrolled Act 576, but the certificate only protects you if the relationship genuinely qualifies. Sole proprietors can elect coverage as employees with written notice, but that election must happen before an injury occurs to provide any protection. Contractors sometimes treat the clearance certificate as a shield against misclassification claims, but it functions only as documentation of status-not as a legal safe harbor. If the actual working relationship contradicts the certificate, the Board disregards the paperwork and examines how the relationship functioned on the job.

Underreporting Payroll Triggers Audits and Recalculations

Underreporting payroll creates a different but equally serious problem because workers’ compensation premiums and benefit calculations depend on accurate wage reporting. Your insurer audits payroll within the first 90 days of your policy and again at renewal, comparing your reported figures to actual payroll records. If the audit reveals underreported wages, your carrier adjusts your premium upward, sometimes substantially, and can assess additional charges for the underreported period.

More importantly, if an injured worker later discovers their benefits were calculated on artificially low wages, they can challenge the benefit amount and potentially recover the difference plus interest. Some contractors underreport thinking it reduces their premium, but the audit process catches these discrepancies consistently. Accurate payroll documentation protects both your premium calculations and your workers’ benefit eligibility.

Delayed Injury Reporting Weakens Your Position

Failing to report workplace injuries promptly creates the third major vulnerability. Most Indiana policies require notice within 24 hours of a serious injury or within a reasonable timeframe for minor incidents. Delayed reporting gives your insurance carrier legitimate grounds to question claim validity, and in some cases to deny coverage entirely. Beyond the policy requirement, prompt reporting protects your worker’s right to benefits.

Indiana generally allows two years from the injury date to file a claim, but delays in initial reporting often complicate medical documentation and weaken the connection between the injury and the job duties. Establish a written injury reporting protocol before problems happen-this protects both your worker and your company. A simple form employees complete immediately after an incident, photographs of the location, and witness statements all strengthen your position when claims are processed.

Final Thoughts

Contractor workers compensation in Indiana protects your business from liability, ensures your team receives proper benefits when injuries happen, and keeps you compliant with state law. Misclassification, underreported payroll, and delayed injury reporting create financial exposure that can damage or destroy a contracting business. The good news is that avoiding these mistakes comes down to understanding three core principles: classify your workers correctly based on how the relationship actually functions, report payroll accurately, and notify your insurance carrier immediately when injuries occur.

Start by reviewing your current worker classifications against Indiana’s multi-factor common-law agency test. Document everything-keep contracts, pay records, company handbooks, and communications that show how your working relationships actually operate. This documentation becomes invaluable if classification disputes arise, and accurate payroll reporting prevents audit surprises while protecting your workers’ benefit calculations.

We at Briggs Agency, Inc. understand the specific insurance challenges Indiana contractors face. Contact Briggs Agency, Inc. for a review of your current coverage and guidance on getting properly protected.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.