Restaurant Property Insurance: Protecting Your Dining Establishment

Your restaurant faces unique risks that standard business insurance won’t cover. From kitchen equipment worth thousands to inventory that spoils overnight, the financial exposure is real and often underestimated.

Restaurant property insurance protects the physical assets that keep your doors open. At Briggs Agency, Inc., we’ve helped dozens of local restaurant owners understand exactly what they need to safeguard their establishments against fire, weather, theft, and unexpected closures.

What Your Property Insurance Actually Covers

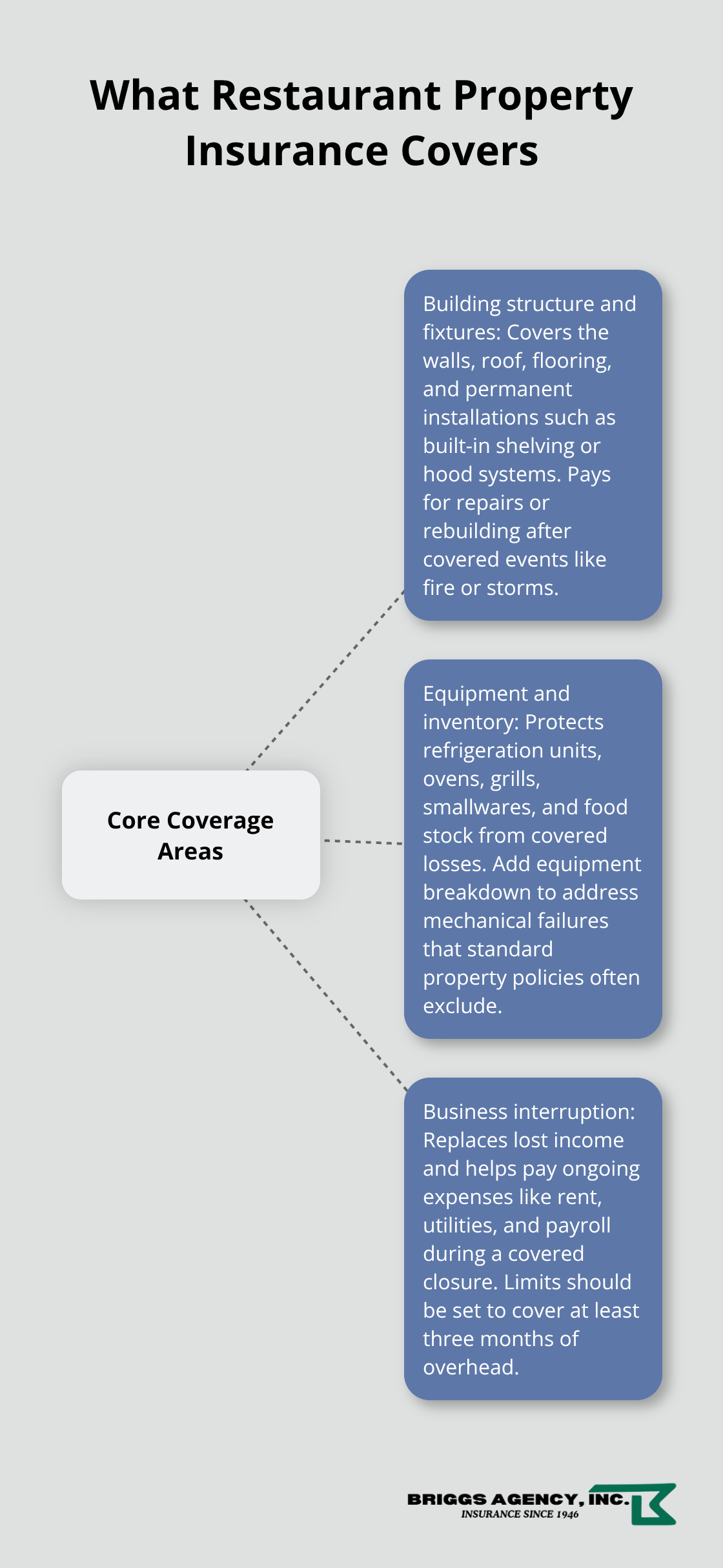

Building Structure and Fixtures

Restaurant property insurance protects three critical areas of your operation, and understanding each one matters because gaps here can drain your cash flow fast. Building structure and fixtures cover the physical shell-walls, roof, flooring, and permanent installations like built-in shelving or hood systems. If a fire damages your dining room or a storm tears through the roof, this coverage pays for repairs or rebuilding.

Equipment and Inventory Protection

Equipment and inventory protection handles the thousands of dollars in refrigeration units, ovens, grills, smallwares, and food stock that spoil without power. Most equipment replacement and inventory loss involves significant costs, and standard property policies often exclude mechanical breakdown though, so a refrigeration failure that spoils $5,000 in inventory won’t be covered unless you add equipment breakdown as a rider.

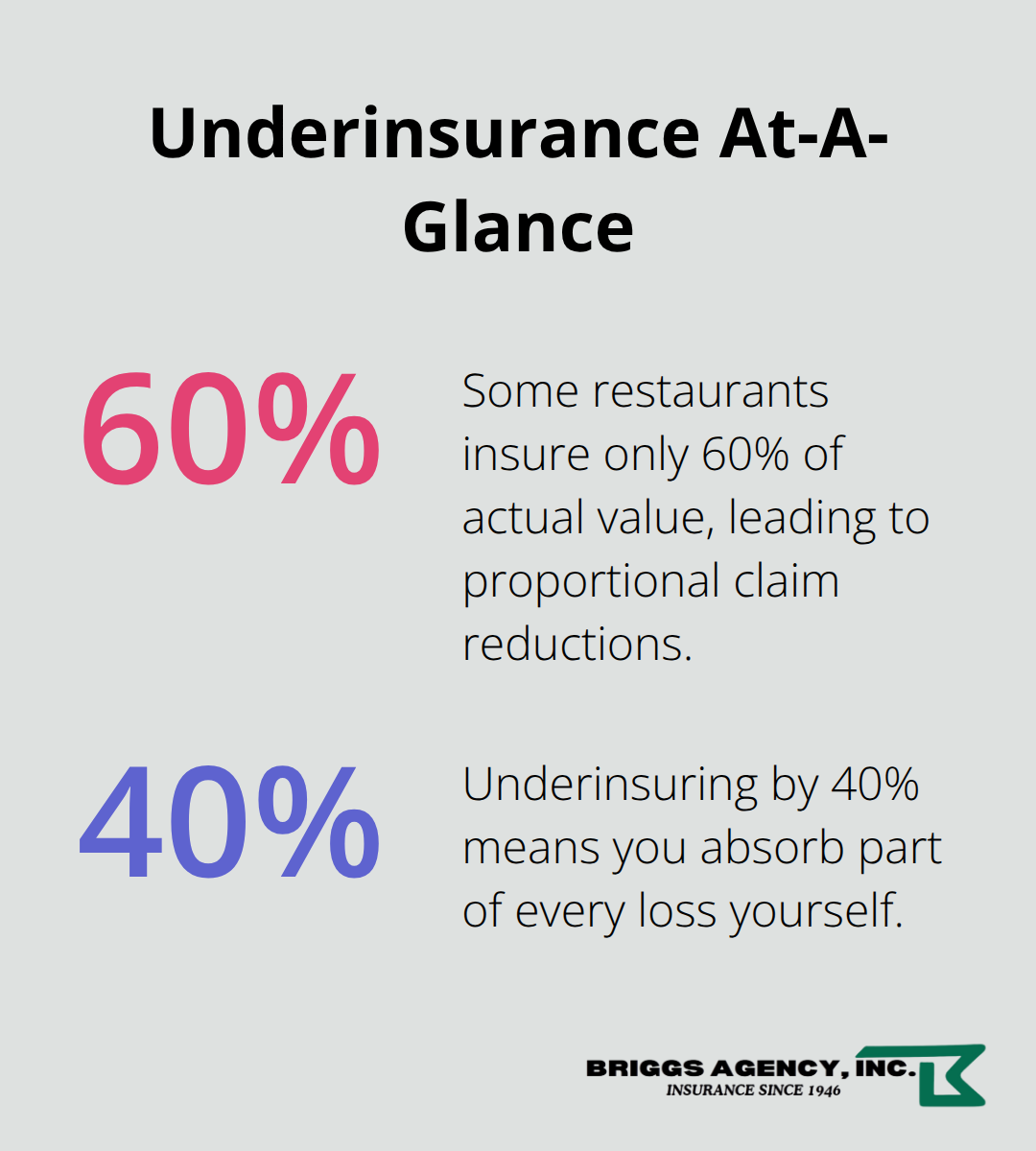

Equipment breakdown represents one of the five most common restaurant claims in Indiana, particularly refrigeration failures and oven breakdowns, yet most owners skip this rider thinking their standard property policy covers it-it doesn’t. Inventory coverage should reflect your peak stock levels, not your average, since a major incident often happens when you’re fully stocked. If your building is worth $500,000 but you only insure it for $300,000, most policies will pay claims on a proportional basis, meaning you absorb part of every loss out of pocket.

Business Interruption Coverage

Business interruption coverage replaces your lost income and covers ongoing expenses like rent, utilities, and payroll while you’re closed for repairs after a covered loss. Without this, you pay those bills from your own pocket while generating zero revenue-a situation that has shut down restaurants permanently even when the physical damage was repairable. Business interruption limits should be high enough to cover at least three months of operating expenses; if your monthly overhead is $15,000 and you’re closed for four months due to a major fire, you need $60,000 available just to stay afloat.

Getting the Coverage Right

An agent who understands restaurant operations specifically will help you calculate accurate values for each category and identify coverage gaps before you have a claim. The specifics matter enormously because underinsuring any of these areas creates real risk. Your next step involves assessing your unique business risks to determine which coverage options and limits actually fit your operation.

Why Your Restaurant Needs Property Insurance

The Real Cost of Fire and Weather Damage

One event-a kitchen fire, a burst pipe, or a severe storm-wipes out years of profit in hours. Fire damage averages around $23,000 per fire in the restaurant industry, and that covers only structural repair. Indiana experiences significant tornado and severe storm activity according to the National Weather Service, which makes this risk especially real for restaurants in our region. When your refrigeration system fails and spoils $5,000 in inventory overnight, or when a tornado damages your building and forces you to close for three months, property insurance becomes the difference between recovering and closing permanently. Without property coverage, you absorb these costs entirely from cash reserves that most restaurants don’t have sitting idle.

Protecting Against Theft and Vandalism

Theft and vandalism represent ongoing threats that many restaurant owners underestimate until they happen. A break-in targeting your POS system, liquor inventory, or kitchen equipment costs $3,000 to $10,000 in losses plus the expense of replacing damaged locks and security systems. Weather-related closures hit even harder because the damage compounds-your building needs repairs, your equipment may need replacement, and your inventory spoils while you remain shut down. Property insurance covers these losses directly, preventing them from draining your operating capital when you can least afford it.

Business Interruption: The Hidden Financial Threat

The real financial pressure comes from business interruption, which is where most restaurant owners face catastrophic loss. If your monthly overhead runs $15,000 and a major fire closes you for four months, you need $60,000 just to cover rent, utilities, payroll, and loan payments while generating zero revenue. This is why property insurance with business interruption coverage isn’t optional-it’s the foundation that keeps your restaurant standing when disaster strikes. Your coverage must reflect your actual peak inventory levels and monthly expenses, not estimates that leave gaps when you need protection most.

Choosing the Right Property Coverage for Your Restaurant

Calculate Your Actual Asset Values

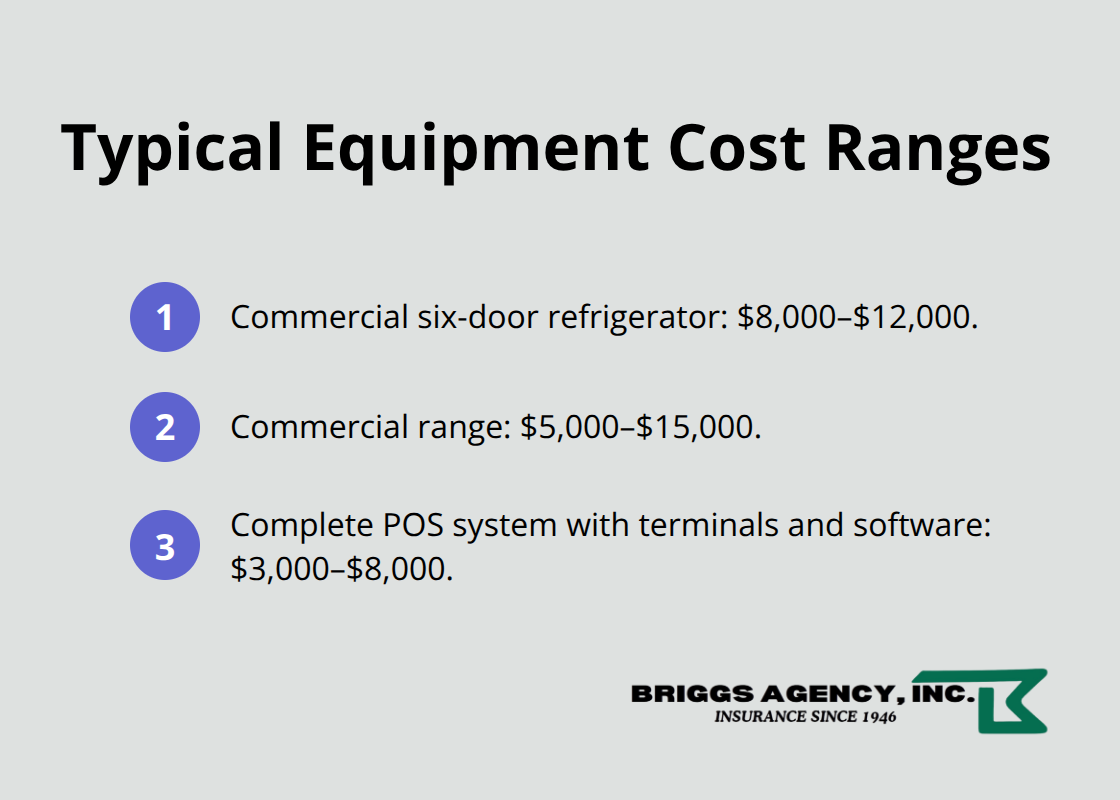

Start with a walk through your restaurant and a notepad to calculate what you actually own. Count your refrigeration units, ovens, grills, POS systems, furniture, and estimate your peak inventory levels-not your average stock, but what you have when fully stocked. Most restaurant owners underestimate equipment value significantly; a commercial six-door refrigerator runs $8,000 to $12,000, a commercial range costs $5,000 to $15,000, and a complete POS system with terminals and software adds another $3,000 to $8,000. Your building value matters equally-if you own, factor in replacement cost for walls, roof, flooring, and permanent fixtures; if you rent, calculate the cost to restore your leasehold improvements like custom hood systems or built-in shelving.

This inventory becomes your baseline for setting coverage limits.

Avoid the Underinsurance Trap

Many restaurants make the critical mistake of insuring for 60 percent of actual value to save on premiums, then discover during a claim that their property insurance policy pays proportionally. If you insure $300,000 worth of assets for $200,000, the insurer pays only two-thirds of any loss. Indiana’s equipment breakdown claims data shows refrigeration failures and oven breakdowns rank among the five most common restaurant losses, yet most standard property policies exclude mechanical breakdown entirely.

Add equipment breakdown coverage as a rider; it covers the costs of repairing or replacing damaged equipment and costs roughly $500 to $1,500 annually but prevents a $5,000 inventory spoilage from coming directly from your pocket.

Set Business Interruption Limits Appropriately

Business interruption limits should cover at least three months of your monthly overhead. If rent, utilities, payroll, and loan payments total $15,000 monthly, set your limit at $45,000 minimum, though four months of coverage provides better protection given typical repair timelines. This protection keeps your operation afloat when disaster forces temporary closure.

Compare Quotes from Multiple Carriers

Once you’ve calculated your actual values, obtain quotes from at least three agents using identical information about your restaurant size, location, employee count, equipment, and services. Request detailed policy language for each quote, not just the premium, because gaps hide in coverage definitions and exclusions. An independent agent representing multiple carriers can access better pricing and broader options than captive agents locked into one company’s forms.

Prioritize Claims Handling Speed Over Price Alone

Independent agents in Indiana often outperform national chains because they understand local risks like Ohio River flood exposure, weather patterns, and regional claim frequency. When comparing quotes, look beyond price to claims handling speed-a carrier that issues certificates of insurance same-day and processes claims within 48 hours protects your operation better than one saving you $200 annually but taking weeks to respond. Ask each agent directly: have they worked with restaurants your size, what claims have they handled for similar operations, and how quickly do they typically resolve property damage claims. We at Briggs Agency, Inc., an independent agency representing multiple top-rated carriers, help local restaurant owners navigate these decisions by comparing options and tailoring policies to deliver the right protection for restaurant-specific risks.

Final Thoughts

Restaurant property insurance protects the physical assets that generate your revenue, but only when coverage limits match your actual values and business needs. Calculate your building value, equipment replacement costs, and peak inventory levels accurately, then set business interruption limits high enough to cover at least three months of overhead. Equipment breakdown coverage costs roughly $500 to $1,500 annually but prevents a refrigeration failure from becoming a $5,000 out-of-pocket expense.

Underinsuring by 40 percent to save on premiums backfires when claims are paid proportionally, meaning you absorb part of every loss yourself. Obtain quotes from at least three carriers using identical information about your size, location, equipment, and services. Compare not just price but claims handling speed, carrier reputation, and whether the agent has worked with restaurants similar to yours.

We at Briggs Agency, Inc., a family-owned independent agency serving Crown Point and surrounding communities since 1946, help local restaurant owners compare options and tailor policies to deliver the right protection for restaurant-specific risks. Our experienced agents represent multiple top-rated carriers, meaning we can find competitive pricing and comprehensive coverage tailored to your operation. Contact us today to discuss your restaurant property insurance needs and get a quote that reflects your actual values and business requirements.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.