Restaurant Insurance for Owners: Protect Your Business and Investment

Running a restaurant means managing countless moving parts, and one critical piece many owners overlook is proper insurance coverage. Restaurant insurance for owners isn’t just a box to check-it’s your financial safety net when accidents, fires, or foodborne illness claims threaten your business.

At Briggs Agency, Inc., we’ve helped restaurant owners across our community understand what coverage they actually need and why it matters. This guide walks you through the protection options available and how to build a policy that fits your operation.

What Your Restaurant Insurance Actually Protects

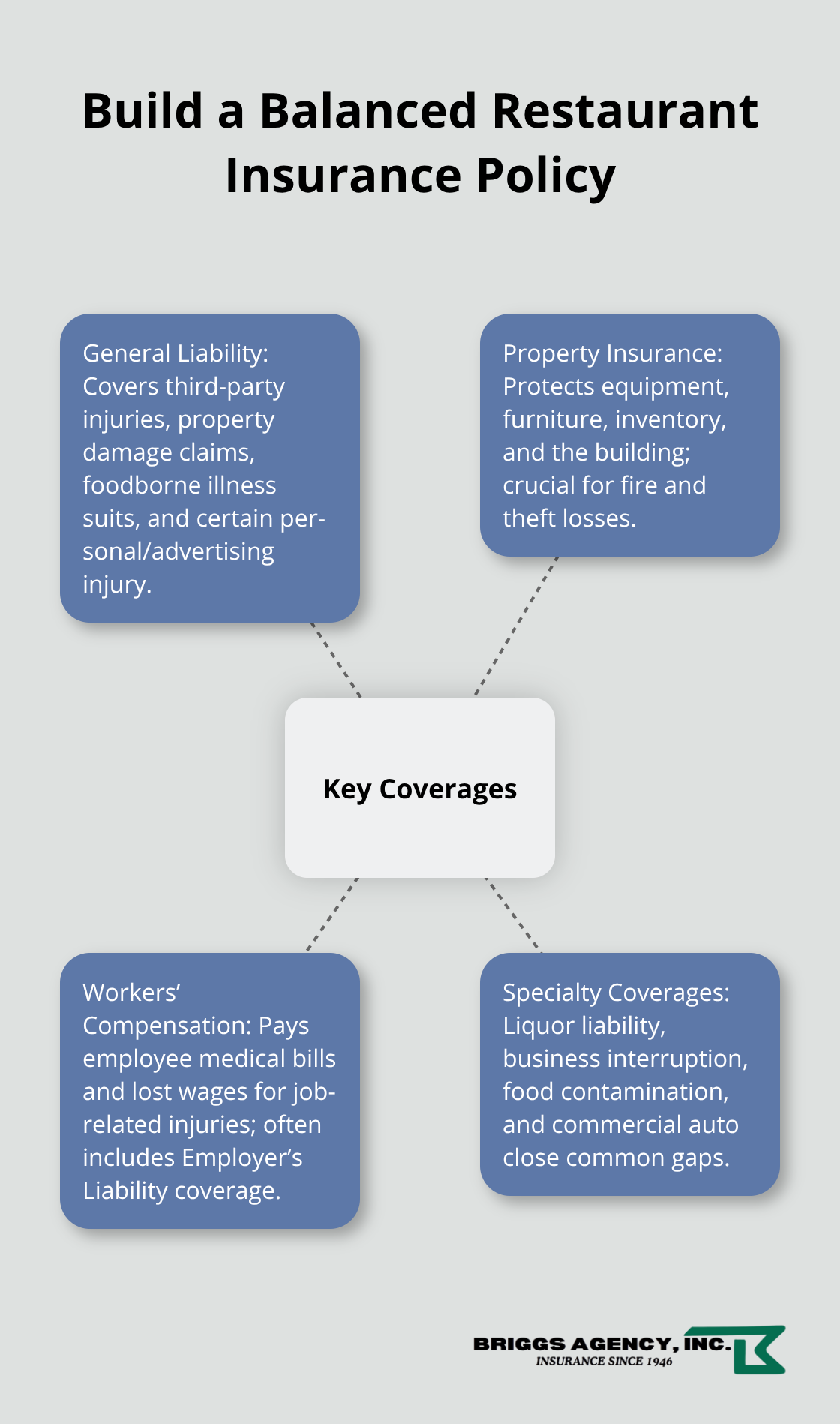

General Liability: Your First Line of Defense

General liability coverage is non-negotiable, and most policies cost between $500 and $6,000 annually with no deductible. This protection covers third-party bodily injuries that occur on your premises-a customer slips on a wet floor, or a server accidentally spills hot coffee on someone. It also covers property damage claims, foodborne illness lawsuits, and even copyright infringement if someone alleges you’ve used their recipe or image without permission. The National Safety Council data shows that workplace and premises incidents remain common in food service, making this foundational coverage essential.

Property Insurance: Protecting Your Equipment and Building

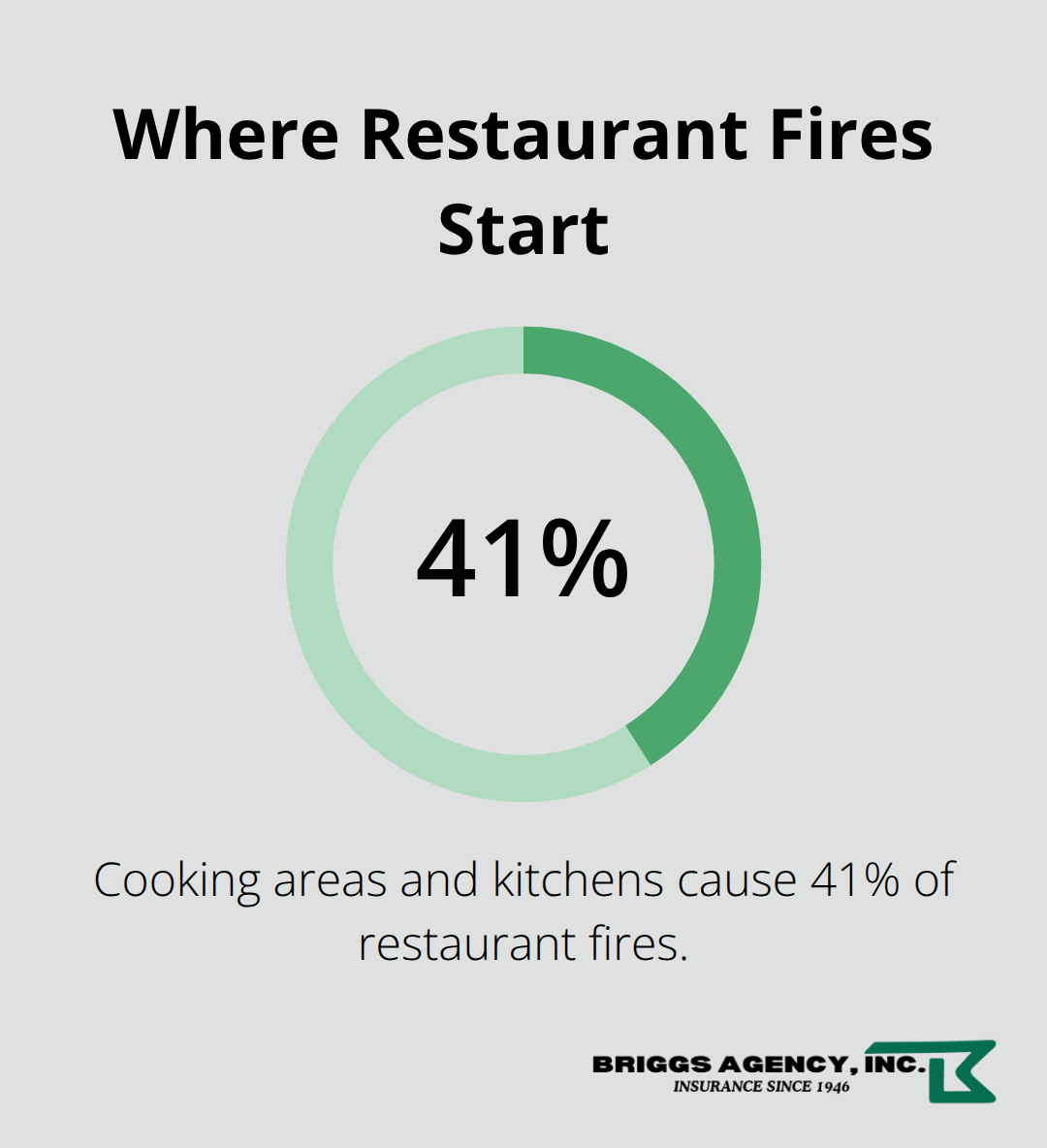

Property insurance typically runs $1,000 to $2,500 per year with a $1,000 deductible and protects your kitchen equipment, furniture, inventory, and the building itself if you own it. Cooking areas and kitchens account for 41 percent of restaurant fires, underscoring why this coverage matters-fire can destroy your entire operation in minutes. If you lease your space, confirm whether the landlord’s policy covers the building structure; your policy must cover everything inside, from your $15,000 commercial range to your point-of-sale system and inventory.

Workers’ Compensation: Protecting Your Team

Workers’ compensation insurance costs roughly $2.25 per $100 of payroll with no deductible and is legally required in nearly all states if you have employees. This coverage pays medical bills and lost wages when an employee sustains an injury on the job-a kitchen burn, a fall in the walk-in cooler, or a repetitive strain injury. Most workers’ compensation policies also include Employer’s Liability Insurance, which protects you if an employee sues over workplace conditions.

Specialty Coverage That Fills Critical Gaps

Beyond these three core coverages, specialty protections fill gaps that standard policies miss. Liquor liability insurance costs $400 to $3,000 annually and covers damages if an intoxicated patron injures someone or damages property-essential if you serve or sell alcohol. Business interruption insurance, averaging $750 to $10,000 per year, replaces lost income and covers ongoing expenses when a covered event forces temporary closure, whether that’s a fire, theft, or severe weather.

Food contamination insurance averages around $1,800 annually and reimburses losses from spoiled or contaminated food during power outages or water-contamination events. If you offer delivery or catering services, commercial auto insurance typically costs $1,200 to $2,500 annually and covers accidents involving business vehicles. General liability alone won’t cover delivery-related incidents, creating a dangerous gap if you skip this protection.

Tailoring Coverage to Your Operation

The right combination of coverages depends on your specific operation-a pizza shop with delivery needs different protection than a fine-dining establishment without alcohol service. Your restaurant’s unique risks determine which specialty coverages matter most, which is why the next step involves assessing your business needs and comparing options with someone who understands your operation.

Common Risks Restaurants Face

Foodborne Illness and Contamination Claims

Foodborne illness claims represent one of the costliest exposures restaurant owners face, yet many underestimate how quickly a contamination incident spirals into legal liability and operational shutdown. Cross-contamination during food prep, improper storage temperatures, and inadequate handwashing protocols create real pathways to illness, and a single outbreak triggers multiple lawsuits, regulatory fines, and mandatory closure. A single foodborne outbreak could cost a restaurant millions of dollars in lost revenue, fines, lawsuits, legal fees, and insurance premium increases.

Your general liability policy covers some food-related injuries, but the scope remains limited. Audit your vendor contracts and food-handling procedures to minimize exposure. Train your kitchen staff on temperature monitoring, cross-contamination prevention, and cleaning protocols specific to your menu items. Require vendors to carry their own liability coverage for any pre-packaged or prepared items they supply.

Slip-and-Fall Incidents

Slip-and-fall incidents on your dining floor or sidewalk happen more often than most owners realize, and they generate claims that can exceed $20,000 when serious injury occurs. A customer trips on a loose floor mat, another slips on a spill that wasn’t cleaned promptly, and suddenly you’re defending a negligence lawsuit and facing potential premium increases if claims repeat.

The solution isn’t just liability coverage-it’s proactive hazard management. Conduct safety inspections at least twice daily and mark wet floors immediately with visible signage. Implement a nightly closing checklist that includes floor inspection, and address any damaged tile or carpet within 48 hours. Document these efforts because they demonstrate due diligence if a claim arises.

Kitchen Fires and Equipment Damage

Kitchen fires remain the most destructive risk in your operation, with cooking areas accounting for 41 percent of all restaurant fires according to the National Fire Protection Association. A single fire destroys your kitchen equipment, inventory, and building improvements in minutes, forcing closure and wiping out months of revenue.

Property insurance protects against fire loss, but you must maintain your hood and duct system according to manufacturer specifications, service your fire suppression system quarterly, and train staff on fire extinguisher use.

These actions reduce both the likelihood of catastrophic loss and your insurance premiums over time. Understanding what threatens your restaurant helps you identify which coverage gaps matter most for your specific operation-the next section walks you through assessing your business risks and selecting the right protections.

How to Choose the Right Restaurant Insurance Policy

Assess Your Specific Business Risks and Needs

Start with your actual operation, not with what you think you should buy. Many restaurant owners begin by collecting basic information: your location, square footage, projected annual sales, inventory value, kitchen equipment list, whether you serve alcohol, and your operating hours. This data matters because a 2,000-square-foot casual pizzeria with delivery creates different risks than a 5,000-square-foot fine-dining establishment without alcohol service. Once you have these details documented, request quotes from at least three insurers who specialize in restaurants rather than general commercial insurance.

Specialists understand that standard liability policies exclude liquor incidents, foodborne illness claims, and delivery-related accidents-gaps that generic policies leave wide open. Your operation’s unique profile determines which specialty coverages matter most and what limits you actually need to protect your investment.

Compare Coverage Options and Limits

When comparing quotes, don’t fixate on premium alone; instead, examine coverage limits, deductibles, and what’s actually excluded. A $500-per-year policy with a $5,000 deductible and $500,000 liability limits won’t protect you the same way a $2,000-per-year policy with a $1,000 deductible and $2,000,000 limits does. Many restaurant owners bundle general liability and property coverage to save money, but bundled policies sometimes offer lower limits or narrower coverage than purchasing each protection separately.

Compare the specific coverage and limits between bundled and individual policies before assuming the bundle saves money overall. The cheapest option often leaves dangerous gaps that cost far more when a claim arises.

Work with a Local Agent Who Understands Your Operation

The real decision comes down to working with someone who understands your restaurant and your community. An independent insurance agent familiar with local fire codes, health department enforcement patterns, and neighborhood demographics can spot coverage gaps you’d miss alone. If you own the building, your needs differ substantially from a lessee; if you added a delivery service last year, your auto liability exposure changed.

Ask potential agents whether they’ve worked with restaurants similar to yours and request referrals from five other restaurant owners they represent. An experienced agent should ask detailed questions about your food-handling procedures, kitchen equipment maintenance, employee training, and vendor relationships before recommending coverage-not just plug numbers into a form.

Adapt Your Coverage as Your Restaurant Evolves

When your coverage needs shift because you’re adding catering, expanding to a second location, or increasing alcohol sales, your agent should proactively recommend adjustments rather than waiting for you to ask. This ongoing partnership matters more than the initial quote because restaurants evolve, risks change, and the insurance that protected you last year may leave gaps today. At Briggs Agency, Inc., we represent multiple top-rated carriers and compare options to tailor policies that deliver the right protection for your specific operation.

Final Thoughts

Restaurant insurance for owners protects your investment when accidents, fires, or contamination claims threaten your business. Your coverage needs shift as your operation evolves-adding delivery services, expanding your menu, or increasing alcohol sales all create new exposures that your current policy may not address. Start by auditing your existing policies against the risks we’ve discussed: Do your limits cover a serious foodborne illness claim? Is your property coverage set to replacement cost? If gaps exist, contact your agent within the next month to adjust your protection.

The difference between adequate coverage and dangerous exposure often comes down to working with someone who understands restaurants and your community. A local agent asks the right questions about your food-handling procedures, kitchen maintenance, and vendor relationships-details that generic commercial insurance agents overlook. At Briggs Agency, Inc., we’ve served restaurant owners across our community since 1946 and represent multiple top-rated carriers so we can tailor policies that fit your operation rather than force you into a standard package.

Your restaurant represents years of hard work and significant financial investment. Reach out to discuss your specific needs and build a policy that protects what you’ve built.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.