Garage Property Insurance Indiana: Coverage That Shields Your Facility

Your garage is one of your biggest business assets, and it faces risks most standard commercial policies don’t cover. From severe Indiana weather to equipment damage and liability claims, the threats are real and specific to your operation.

At Briggs Agency, Inc., we’ve helped countless garage owners in Indiana find the right protection. Garage property insurance Indiana policies tailored to your facility can make the difference between a minor setback and a business-threatening loss.

What Your Garage Property Insurance Actually Covers

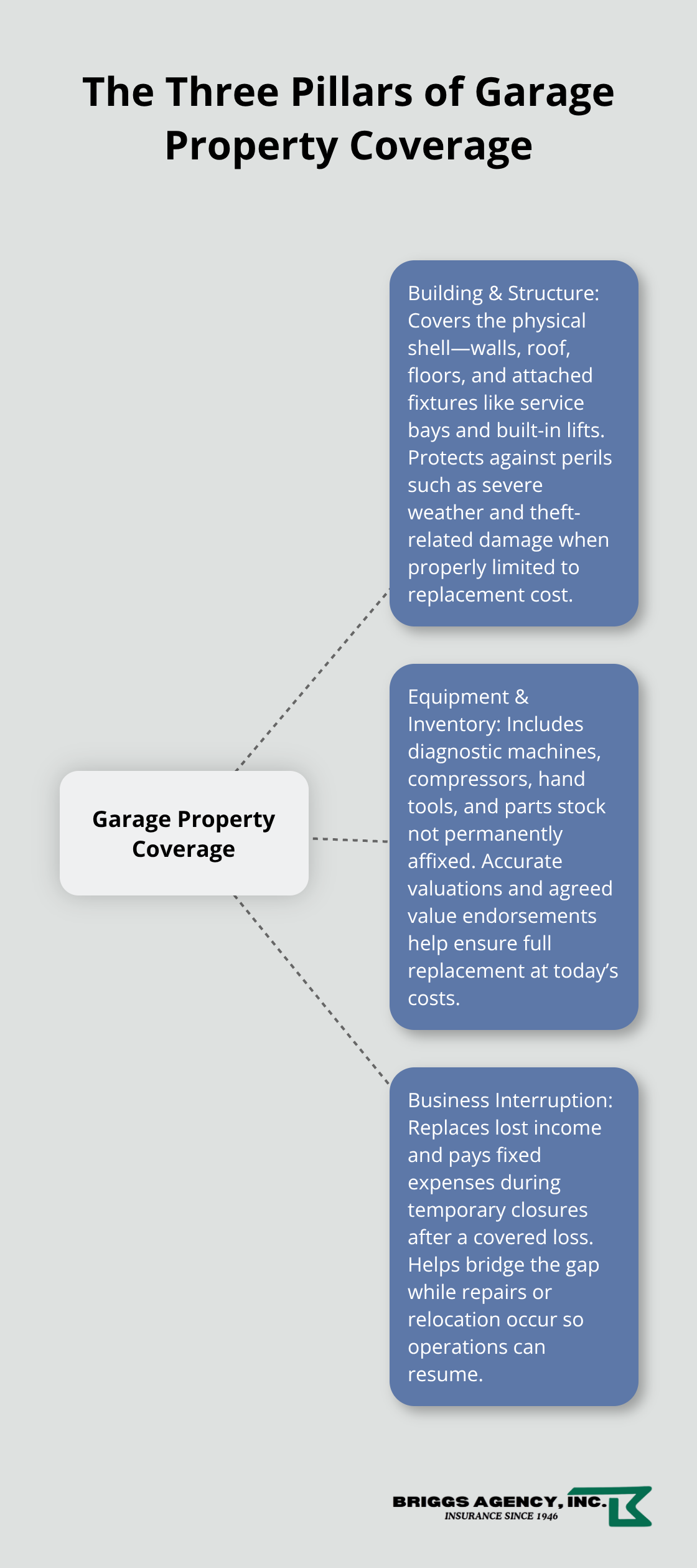

Garage property insurance in Indiana protects three critical areas of your operation, and understanding exactly what falls under each one matters more than you might think. Your building structure is the foundation-walls, roof, flooring, and the physical shell that houses your business. This includes permanent fixtures like service bays, lifts, and built-in equipment that are attached to the building itself. Many garage owners assume their standard commercial policy covers this, but it often doesn’t, especially when your facility has specialized equipment or modifications. Equipment, tools, and inventory represent the movable assets that generate your revenue: diagnostic machines, air compressors, hand tools, parts inventory, and vehicle lifts that aren’t permanently affixed. Equipment and inventory value is one of the largest premium drivers for auto repair shops, so accurately valuing these items during the quote process directly impacts your protection level.

The third component, business interruption insurance, covers your lost income and fixed operating expenses if a covered event forces you to temporarily close or relocate. If a fire damages your facility and you lose three weeks of revenue while repairs happen, it covers rent, payroll, utilities, and lost profits during that shutdown period-not just the physical damage itself.

Building and Structural Protection

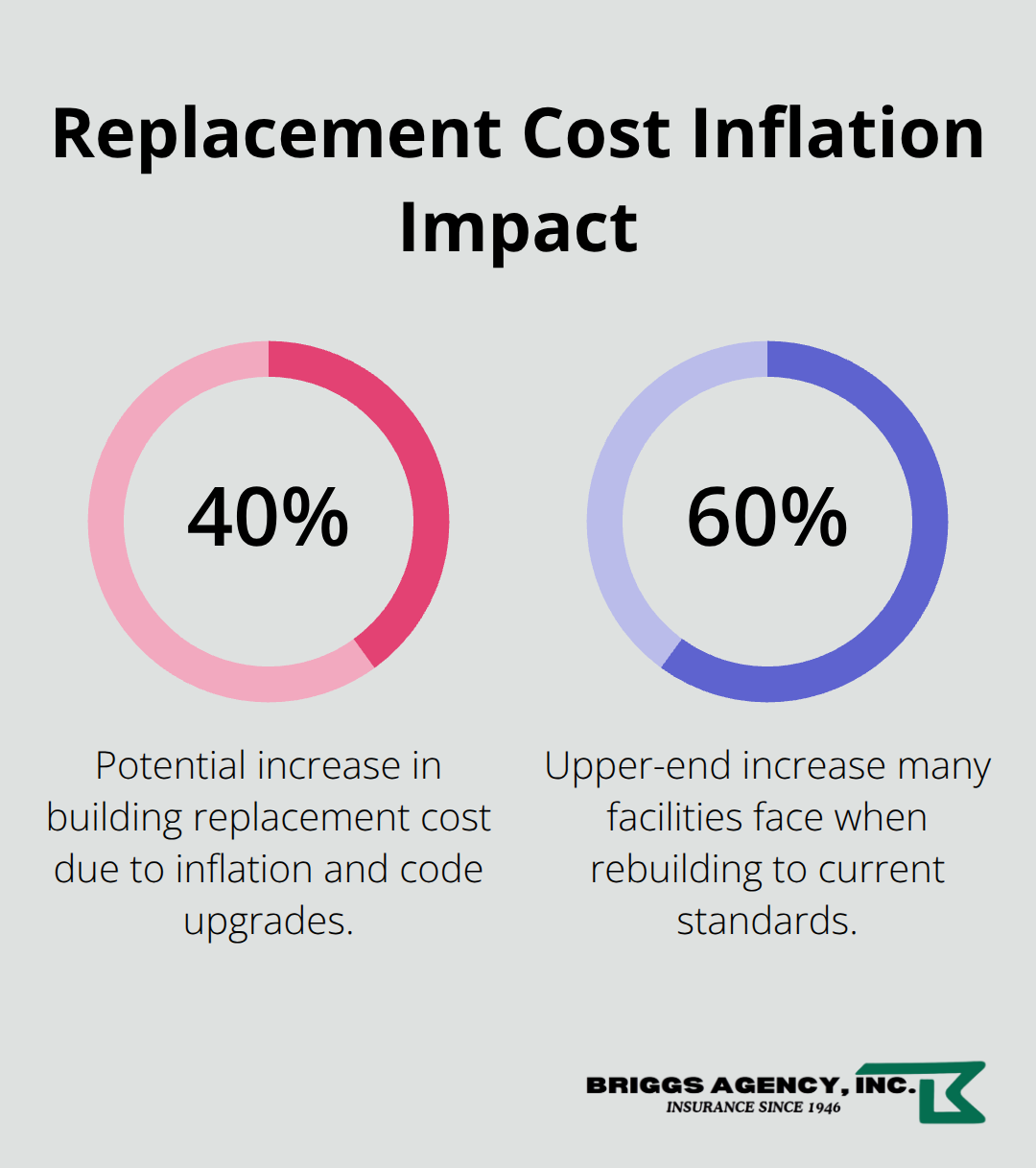

Your garage’s physical structure faces Indiana-specific threats that standard property policies often exclude or limit. Winter weather causes significant damage: ice dams lead to water intrusion, freeze-thaw cycles crack concrete foundations and damage underground utilities, and heavy snow loads stress roof structures. Spring severe weather brings hail damage to roofing and siding, and wind damage can compromise structural integrity or remove entire roof sections. A robust garage property policy covers these weather-related losses, but you need to verify your specific limits match your building’s replacement cost, not just its current market value. Many garage owners underestimate replacement costs because they fail to account for today’s labor and material expenses. If your facility was built in 2005 and cost $250,000 then, replacement today easily runs 40-60% higher due to inflation and code upgrades.

Theft and break-ins also damage building components-forced entry damages doors, windows, and locks, and the resulting water damage from exposed openings adds additional loss. Your policy should cover not just the theft itself but also the secondary property damage that follows.

Equipment, Tools, and Diagnostic Machines

This is where most garage owners face coverage gaps. Diagnostic equipment, alignment machines, and specialized lifts represent $50,000 to $150,000 or more in assets, depending on your service scope. Standard commercial property policies often apply blanket limits to equipment or exclude certain types entirely. Your garage property insurance should specifically cover equipment breakdown and replacement at full replacement cost, not depreciated value. Many policies offer agreed value endorsements for high-value equipment, which means you and the insurer agree upfront on the replacement cost, eliminating disputes when a claim occurs. Hand tools present a different challenge because they’re portable and scattered throughout the facility. A comprehensive policy covers hand tools within your facility but may exclude tools left in vehicles or taken off-site. Keep a detailed inventory with photos and serial numbers of all equipment and high-value tools; this documentation speeds claims processing significantly and prevents disputes over what you actually owned. Inventory of parts and fluids should also be covered at full replacement cost. If a water loss damages your parts stockroom, you need coverage that pays what you’d spend to replace those parts, not what you paid for them months earlier.

Why Coverage Limits Matter for Your Bottom Line

The difference between adequate coverage and underinsurance can devastate your business. You must calculate the actual replacement cost of your building, equipment, and inventory-not the depreciated value or what you think it’s worth today. Many garage owners discover too late that their policy limits fall short when they file a claim. An agreed value endorsement (also called a stated value endorsement) locks in your coverage amount upfront, so you avoid disputes about what your equipment is actually worth. This approach works especially well for high-value diagnostic machines and specialized lifts that lose value quickly on the used market but cost substantially more to replace new. Your policy should also address the time it takes to replace equipment and resume full operations. Business interruption coverage fills that gap by paying your fixed expenses while you rebuild, but only if your property policy limits are high enough to cover the actual loss.

Understanding these three coverage areas positions you to make informed decisions about your facility’s protection. The next step involves assessing your specific risks and comparing what different policies actually offer.

Why Indiana Garage Owners Face Real Coverage Gaps

Indiana’s Weather Creates Specific Property Damage Risks

Indiana’s weather patterns create property damage risks that generic commercial policies simply don’t address adequately. Winter freeze-thaw cycles damage concrete floors and foundations at an accelerated rate compared to milder climates, and ice dams routinely cause water intrusion into garage structures during March and April thaws. Spring severe weather brings hail events that damage roofing and siding-the National Weather Service documents multiple hail events across Indiana annually that exceed one inch in diameter. Heavy snow loads in northern Indiana counties stress roof structures designed for average loads, and wind speeds during spring storms regularly exceed 50 mph. Your standard commercial property policy may exclude weather-related losses or apply separate limits that don’t reflect your actual replacement costs.

Building Code Upgrades Add Hidden Costs

Indiana enforces specific building codes for commercial garages, particularly regarding fire suppression systems, electrical standards for vehicle service areas, and ventilation requirements for emissions control. If a covered loss forces you to rebuild, your new structure must meet current code standards, which typically cost more than the original construction. A proper garage property policy accounts for these code upgrades and doesn’t leave you paying the difference out of pocket. This gap between original construction costs and code-compliant rebuilding expenses catches many garage owners off guard when they file claims.

Liability Exposure Differs Significantly from Other Businesses

Liability exposure in Indiana garages differs significantly from other business types because your operation involves customer vehicles, employee test drives, and high-value equipment in close quarters. If a mechanic’s test drive causes an accident, your standard commercial general liability won’t respond-you need garage liability coverage specifically. Property damage claims in Indiana garages spike during certain seasons: spring hail damage, summer thunderstorm water intrusion, and winter ice-related losses create predictable claim patterns that insurers price accordingly. This seasonal risk concentration means your coverage limits must account for multiple potential losses happening in compressed timeframes, not just single isolated incidents.

Regulatory Requirements and Equipment Replacement Costs

Indiana’s regulations around vehicle storage, hazardous materials handling, and employee safety standards directly impact your insurance needs and premium calculations. Garages storing vehicles for extended periods face different liability exposure than shops that complete work same-day, and your policy must reflect your actual operation. Equipment breakdown coverage becomes critical in Indiana because the cost to replace specialized diagnostic machines or alignment systems runs substantially higher than depreciated values suggest. A 2015 alignment machine worth $30,000 new might show a used market value of $12,000 today, but replacement with current technology costs $40,000 or more. Agreed value endorsements prevent this gap from devastating your claim recovery.

Common Claims Patterns in Indiana Garages

Common garage-related claims in Indiana include theft from unsecured facilities (particularly in urban areas like Indianapolis and Gary), water damage from roof leaks during spring thaw periods, and equipment failures that interrupt operations for days or weeks. Fire damage claims in garages often involve flammable materials storage or electrical system failures, and Indiana fire codes require specific suppression systems that affect your coverage options. Many garage owners discover their coverage limits fall short after a loss occurs, which is why detailed facility assessments matter. These assessments must account for Indiana’s specific weather patterns, local regulatory environment, and the unique operational risks your garage faces. Understanding these regional factors positions you to evaluate whether your current coverage actually protects your facility or leaves critical gaps exposed.

How to Choose the Right Garage Property Insurance Policy

Start with a detailed facility walkthrough that documents every asset and vulnerability specific to your garage. Photograph your building’s exterior, roof condition, and foundation; list every piece of equipment with purchase dates and current replacement costs; and inventory your parts stockroom by category and approximate value. This documentation forms the foundation for accurate quotes and proper claim recovery. Contact three to five insurance carriers that specialize in garage operations, not general commercial policies. Indiana-specific carriers understand freeze-thaw damage patterns, seasonal hail risk, and local building code requirements that generic insurers miss entirely.

When you receive quotes, compare the actual replacement cost values carriers assign to your building and equipment, not just the premium amounts. If one quote values your alignment machine at $15,000 and another at $35,000, that difference directly impacts your claim recovery if equipment fails. Agreed value endorsements waive the coinsurance provision and lock in replacement costs upfront. Request that carriers itemize coverage limits separately for building, equipment, inventory, and business interruption rather than bundling them into single limits. This transparency reveals whether your policy protects all three areas or leaves gaps in critical categories.

Deductibles and Business Interruption Coverage

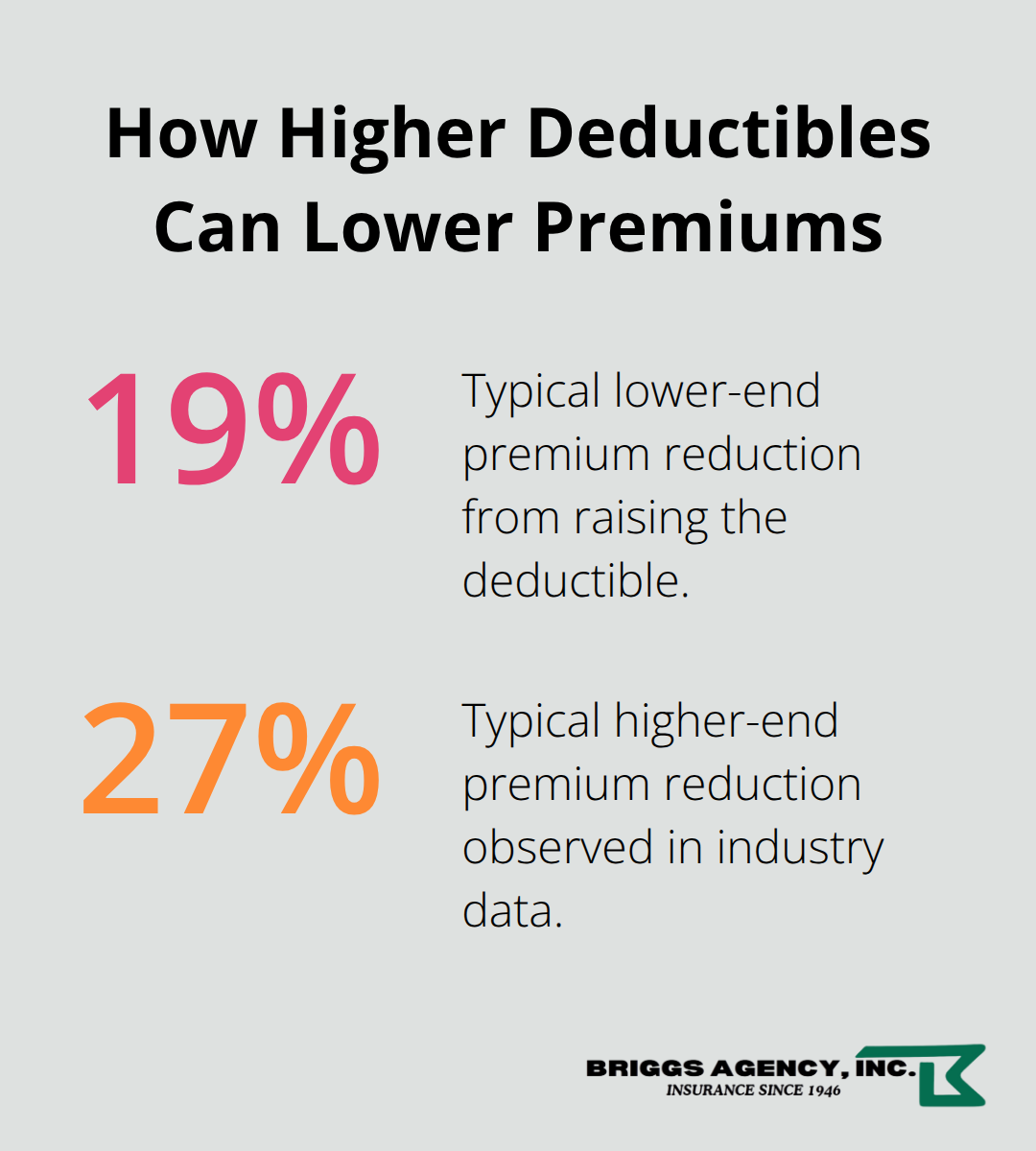

Your deductible choice directly affects your monthly premium and your out-of-pocket costs during claims. Increasing your deductible from $500 to $2,500 typically reduces premiums by 19 to 27 percent according to industry cost data, but only if your business can absorb that larger out-of-pocket expense.

A single water loss from spring thaw could cost $8,000 to $15,000 in repairs, so your deductible must align with your cash flow capacity, not just premium savings.

Business interruption coverage protects your bottom line during forced closures. Calculate your monthly fixed expenses-rent, payroll, utilities, insurance premiums, and loan payments-and try for a business interruption limit that covers at least 90 days of operations. If your monthly fixed costs total $12,000, a 90-day interruption costs $36,000 in lost income, and many garage owners underestimate this figure. Request quotes that clearly state how many days of coverage you receive and whether the policy includes a waiting period before payments begin. Some policies include a 30-day waiting period, which means you absorb the first month of losses yourself. For Indiana garages, seasonal risks mean you might face multiple claims in compressed timeframes (spring hail damage followed by summer water intrusion, for example), so your annual aggregate limits matter as much as per-occurrence limits.

Finding Agents Who Understand Your Operation

Local insurance agents who specialize in garage operations ask different questions than generalist brokers. They know that a transmission shop faces different risks than a quick-lube facility, and a shop storing customer vehicles for weeks faces different liability exposure than one completing same-day work. When you meet with an agent, expect detailed questions about your service scope, equipment values, customer vehicle storage practices, and claims history. Provide that information accurately because incomplete details lead to inadequate coverage.

Discuss Indiana-specific risks directly: ask how the policy handles freeze-thaw damage, spring hail, and code upgrade costs during rebuilding. Request sample policies and read the exclusions carefully-some carriers exclude certain equipment types or apply sublimits that reduce your actual protection. Compare not just premiums but also the financial stability ratings of carriers offering quotes. J.D. Power and Consumer Reports provide insurer quality rankings that help you avoid carriers with poor claims-handling reputations. A $200 annual premium savings means nothing if the carrier denies your claim or delays payment for months during a critical shutdown period.

Final Thoughts

Your garage’s protection depends on decisions you make today. Garage property insurance Indiana policies must address three specific areas: your building structure against weather and theft, your equipment and inventory at full replacement cost, and your business operations during forced closures. Generic commercial policies leave gaps in all three areas, which is why specialized garage coverage matters.

Start by documenting your facility’s actual replacement costs, not depreciated values. Photograph your building, list every piece of equipment with current replacement prices, and calculate your monthly fixed expenses for business interruption planning. Request quotes from carriers that specialize in garage operations and compare their replacement cost valuations carefully-an agreed value endorsement locks in those costs upfront and prevents disputes when you file claims.

Contact Briggs Agency, Inc. today to schedule your facility assessment and receive quotes tailored to your garage’s unique needs. We at Briggs Agency, Inc. represent multiple top-rated carriers, which means we compare options across different insurers rather than pushing a single company’s products. Our team will walk through your facility, identify your specific risks, and build a garage property insurance policy that actually protects your investment.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.