Indiana Garage Insurance Rates: What Determines Your Premiums

Your garage insurance premiums in Indiana depend on several factors you can actually control. At Briggs Agency, Inc., we help local business owners understand exactly what drives their rates and where they can save money.

This guide walks you through the real costs behind Indiana garage insurance rates, practical ways to lower your premiums, and how to compare quotes without getting lost in the details.

What Really Drives Your Indiana Garage Insurance Premiums

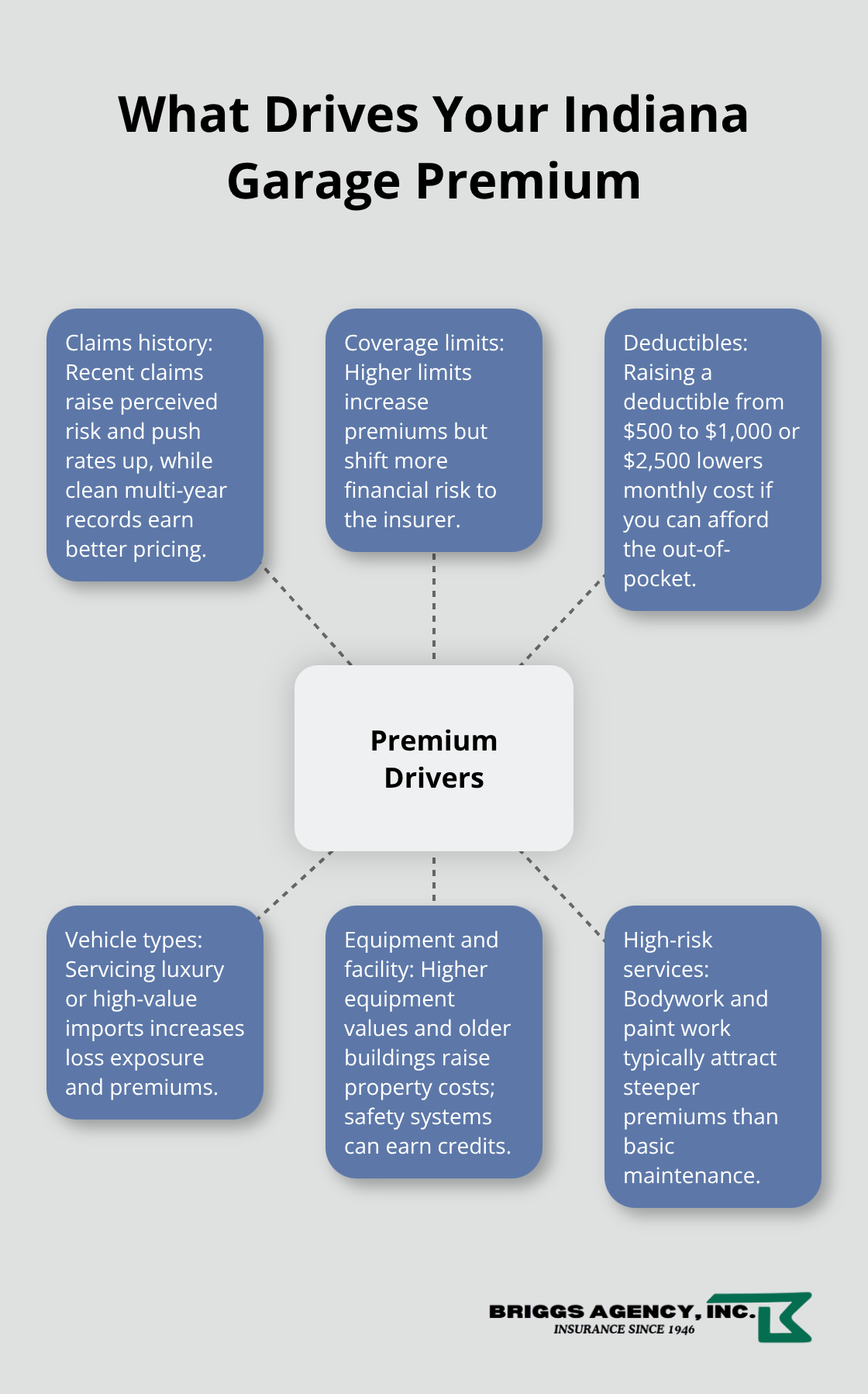

Your Claims History Sets the Tone

Your claims history hits your premiums harder than almost anything else. If you filed claims in the past three to five years, insurers view you as higher risk, and your rates reflect that. A single at-fault accident during a test drive or while a vehicle sits in your care can add hundreds to your annual premium. MoneyGeek’s analysis of typical auto repair shops shows that claims history directly influences underwriting decisions across all coverage types. Shops with clean records over several years earn better rates. This means every decision to file a claim-or handle minor damage out-of-pocket-carries real financial weight. Your driving record matters too, especially if you or your employees regularly road-test customer vehicles.

Traffic violations and accidents on personal time can affect your business insurance rates because insurers see them as indicators of risk behavior.

Coverage Limits and Deductibles Control Your Costs

The limits you choose aren’t just about compliance; they’re the single biggest lever you control over your premium. Indiana’s minimum garage liability requirements are $100,000 bodily injury per person and $300,000 per accident, with $50,000 property damage. Many dealers stop there, but that’s a mistake. Shops that carry higher limits-say $500,000 or $1,000,000-pay more upfront but transfer far more risk to the insurer. Your deductible works the opposite way: raising it from $500 to $1,000 or $2,500 lowers your monthly cost significantly. A typical Indiana auto repair shop that bundles general liability, workers’ compensation, professional liability, and a Business Owners Policy pays about $217 per month for the BOP alone, according to MoneyGeek’s data. Add a garage keeper’s endorsement to cover customer vehicles in your care, and you face additional exposure that justifies higher limits. The type of work matters too: shops that perform high-risk services like bodywork or paint work face steeper premiums than those that handle basic maintenance.

Vehicle Types and Equipment Value Affect Your Rate

The vehicles you service and the equipment you own directly affect your rate. Luxury vehicles or high-value imports represent larger loss exposure than standard sedans, so shops that handle those vehicles pay more. Your diagnostic equipment, lifts, and tool inventory also factor into property coverage pricing. Shops with $500,000 in equipment on hand need higher property limits than those with $150,000 worth. Age of your facility matters too: older buildings without updated electrical systems or fire suppression may face higher rates or coverage restrictions. Sprinkler systems, alarm systems, and surveillance cameras can qualify businesses for premium discounts. Document these safety measures and share them with your insurer during renewal; you may qualify for loss-control credits that chip away at your bill. Understanding what your insurer sees as risk helps you make smarter decisions about which coverage upgrades and safety investments pay off fastest.

Real Ways to Cut Your Indiana Garage Insurance Costs

Bundle Your Policies for Immediate Savings

Bundling your policies cuts your monthly costs faster than any other single action. When you add garage keeper’s coverage and other specialized endorsements to that bundle, the per-policy cost drops noticeably compared to buying each one separately. Independent agencies like Briggs Agency, Inc. represent multiple top-rated carriers, which means they can shop your coverage across different insurers to find the combination that costs less while keeping your protection intact. Many shop owners buy policies one at a time from whoever answers the phone first, which costs them hundreds annually without delivering better coverage.

Keep Your Driving Record Clean

Your driving record and the records of anyone who test-drives customer vehicles directly impact your premium because insurers track these details closely. A single traffic violation or at-fault accident in the past three to five years signals higher risk to underwriters, and your rate moves up accordingly. Shops with clean records earn substantially better rates than those with violations on file. If you or your employees have traffic tickets or accidents, work to clear those records before renewal time rolls around, and disclose them honestly when shopping quotes because insurers will find them anyway. This transparency prevents surprises and helps your agent find carriers willing to work with your situation.

Install Security and Safety Equipment

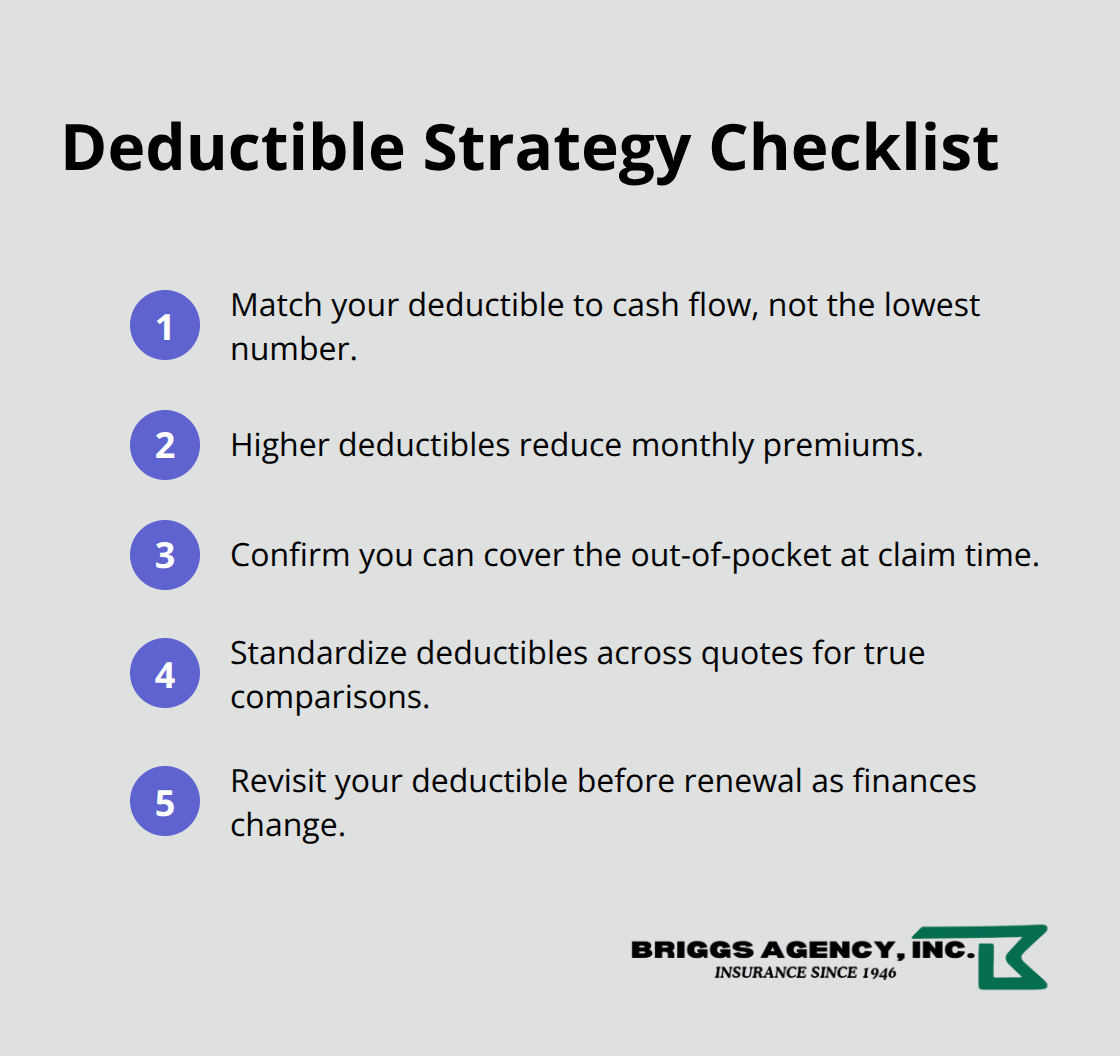

Installing visible security measures like alarm systems, surveillance cameras, and fire suppression equipment cuts your premium in concrete ways. These aren’t optional upgrades that sound nice; they qualify you for loss-control credits that reduce your actual bill. Document every safety investment you make, photograph your equipment and systems, and hand that documentation to your insurer during renewal conversations. Raising your deductible from five hundred to one thousand or even twenty-five hundred dollars also lowers your monthly cost significantly, though you need to ensure you can actually cover that amount out-of-pocket if a claim happens. Match your deductible to your cash flow situation, not the lowest number available.

Adjust Your Coverage Limits and Deductibles Strategically

Your deductible choice directly controls what you pay each month. Higher deductibles mean lower premiums, but only if your business can absorb the out-of-pocket cost when a claim occurs. Many shop owners set deductibles too low because they focus on the monthly payment rather than their actual financial capacity. Test this: if a customer’s vehicle sustains five thousand dollars in damage while in your care, could you cover a twenty-five-hundred-dollar deductible without disrupting operations? If yes, that higher deductible saves you money every month. If no, stick with a lower deductible and accept the higher premium as the cost of financial stability.

Your coverage limits also matter tremendously. Indiana’s minimums are $100,000 bodily injury per person and $300,000 per accident, with $50,000 property damage, but many dealers stop there and expose themselves to significant risk. Shops that carry higher limits transfer far more risk to the insurer and pay more upfront but sleep better at night knowing they’re protected.

Compare Quotes to Find Your Best Rate

Shopping multiple insurers reveals how much rates vary for identical coverage. One carrier might quote $300 per month while another quotes $600 for the same limits and deductibles, depending on how they underwrite garage operations and what risk factors they weight most heavily. When you request quotes, provide identical information to each insurer so you can actually compare apples to apples. Include details about your vehicle types, equipment value, employee count, and any safety measures you’ve installed. This information helps carriers price your risk accurately and sometimes uncovers discounts you didn’t know existed. Once you have quotes in hand, look beyond the monthly number and examine what each policy actually covers, which endorsements are included, and whether the limits match your actual exposure.

How to Read a Garage Insurance Quote

What Makes Quotes So Different

Comparing quotes means understanding what each number actually represents, and most shop owners skip this step entirely. When you request quotes from multiple carriers, you’ll see vastly different prices for what appears to be the same coverage. This variation isn’t random; it reflects how each insurer weights your specific risk factors.

Breaking Down the Details That Matter

To make apples-to-apples comparisons, you need to look past the monthly premium and examine the actual policy details. Check whether each quote includes garage keeper’s coverage, which protects customer vehicles in your care during repair, storage, or test drives. Verify the bodily injury and property damage limits match across all quotes. Confirm that workers’ compensation, professional liability, and Business Owners Policy coverage are included in bundled quotes, since some carriers price these separately and others include them together.

Request quotes with identical deductibles-say $1,000 across the board-so premium differences reflect underwriting philosophy rather than coverage choices. Ask each carrier specifically which safety measures or equipment they’re crediting in their quote, because one insurer might offer a discount for your alarm system while another doesn’t. This detail matters because you can sometimes find savings simply by informing carriers about existing safety investments they didn’t know about.

Local Agencies Understand Your Market Better

National insurance companies operate from distant underwriting centers and apply broad formulas that don’t account for your shop’s specific location or reputation in the local community. Local independent agencies represent multiple top-rated carriers and understand Indiana’s specific risk landscape-winter weather patterns, local theft exposure, and regional vehicle types that affect your actual claims likelihood. When you work with a local agency, your agent advocates directly with carriers on your behalf, explaining your shop’s safety practices and claims history in context rather than letting a computer algorithm decide your rate.

National providers also take longer to respond to questions and process changes, which costs you time during renewal periods when rates matter most.

Red Flags That Signal Trouble

Watch for carriers that quote suspiciously low rates-rates that seem thirty or forty percent below competitors often indicate either missing coverage or underwriting that will result in claim denials when you need protection most. Avoid any quote that doesn’t clearly list what’s included and what’s excluded; vague wording about coverage scope means disputes later.

If a quote lacks details about garage keeper’s coverage limits, employee coverage, or how high-risk services like bodywork affect the rate, ask directly or move to another carrier. Some national providers also impose strict guidelines about which vehicles you can service or limit your coverage if you perform certain types of work, restrictions that local agencies can often negotiate away with carriers that know your business.

Final Thoughts

Your Indiana garage insurance rates reflect the choices you make today about coverage limits, deductibles, safety equipment, and which carriers you compare. Claims history, vehicle types, and policy details matter far more than the monthly premium alone, so take time to examine what each quote actually includes and verify that garage keeper’s coverage protects your customer vehicles. Raising your deductible to $1,000 or $2,500 cuts your costs immediately if your cash flow allows it, while installing security systems and fire suppression equipment qualifies you for loss-control credits that reduce your bill month after month.

Working with a local independent agency makes this process faster and smarter because we represent multiple top-rated carriers and understand Indiana’s specific risk landscape in ways national providers cannot match. Briggs Agency, Inc. compares options across different insurers, negotiates on your behalf, and tailors policies to deliver competitive pricing alongside the right protection for your operation. Contact us today to get quotes on your garage coverage and see how much you might save by working with an agency that knows your community and genuinely cares about your success.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.