Small Restaurant Insurance Indiana: A Practical Guide for Local Owners

Running a restaurant in Indiana means juggling dozens of moving parts, and insurance is one that can’t be overlooked. Most restaurant owners discover too late that standard business policies leave dangerous gaps in coverage.

At Briggs Agency, Inc., we’ve helped countless local restaurant owners find the right small restaurant insurance in Indiana to protect what they’ve built. This guide walks you through exactly what you need.

What You’re Actually Risking Without Restaurant-Specific Coverage

Why Generic Policies Fall Short for Food Service

Standard business insurance policies treat restaurants like any other operation, which is precisely the problem. A generic commercial general liability policy might cover slip-and-fall incidents, but it often excludes foodborne illness claims, liquor-related liability, and spoilage losses that can devastate a food service business. Indiana restaurants face distinct exposures that demand specialized protection, yet many owners discover critical gaps only after a loss occurs.

The Real Cost of Common Restaurant Disasters

The National Fire Protection Association reports that restaurants burn at roughly twice the rate of other commercial buildings, with cooking equipment the leading cause. Water damage from burst pipes, slip-and-fall accidents exceeding $500,000 in medical costs and settlements, and foodborne illness outbreaks that sicken patrons represent everyday risks in this industry. Food contamination alone costs around $1,800 per incident when inventory spoils, not counting the legal defense costs and lost business income that follow.

Indiana’s Legal Requirements Add Complexity

Indiana law requires workers’ compensation for any restaurant with employees, plus mandatory liquor liability insurance if you serve alcohol-a legal obligation tied directly to your liquor license through the Indiana Alcohol and Tobacco Commission. Health code violations carry fines up to $1,000 per violation and can trigger license suspension, transforming operational oversights into financial crises that insurance must address.

The CDC estimates that foodborne illnesses sicken about 48 million Americans annually, making robust protection non-negotiable for any food service operation.

Your Specific Exposure Determines Your Coverage Needs

Your restaurant’s actual exposure depends on your specific setup: whether you own or lease the building, how many employees you have, whether you offer delivery services, and what your claims history shows. A small fast-casual spot with five employees and no alcohol service faces entirely different risks than a fine-dining establishment with a full bar and delivery operations. Indiana’s location and local risk profiles also matter-flood-prone areas need riders that standard property policies exclude, and storm-prone considerations apply differently across the state.

Finding the Right Coverage Starts With Honest Assessment

Getting the right coverage starts with honest assessment of your operation’s details, not guessing based on what another restaurant carries. A local agent who understands Indiana’s specific legal landscape and restaurant risks spots gaps that online quotes miss, making the next step-identifying which coverage types actually protect your business-far more straightforward.

The Four Coverage Pillars Every Indiana Restaurant Needs

General Liability: Your First Line of Defense

General liability insurance forms the foundation of restaurant protection, covering the slip-and-fall incidents and food poisoning claims that plague this industry. Indiana restaurants typically need limits of $1 million per occurrence, with average costs around $73 per month and many policies offering $0 deductibles. This coverage pays for medical expenses, legal defense, and settlements when a customer is injured on your property or becomes ill from your food. A single slip-and-fall accident costing $500,000 in medical expenses and settlements wipes out most small restaurants’ operating capital without this protection.

Property Insurance: Protecting Your Physical Assets

Property insurance protects your building, kitchen equipment, and inventory from fire, theft, storms, and vandalism on a replacement-cost basis. The National Fire Protection Association reports restaurants burn at roughly twice the rate of other commercial buildings, with a single fire potentially destroying $50,000–$100,000 of equipment and inventory. Property coverage averages about $106 per month with a typical $1,000 deductible, and it becomes non-negotiable if your landlord holds the lease-most require proof of coverage before you open.

Workers’ Compensation: A Legal Mandate

Workers’ compensation is legally mandatory in Indiana the moment you hire your first employee, covering medical costs and lost wages for injured staff members. Indiana Workers’ Compensation Board data shows median costs around $139 per month, calculated as roughly $2.25 per $100 of payroll, with claims typically filed within two years of the incident. Noncompliance triggers penalties that dwarf the insurance premium itself, making this coverage non-negotiable from both a legal and financial standpoint.

Liquor Liability: Required if You Serve Alcohol

Liquor liability insurance is essential if you serve alcohol-not optional-because Indiana law ties it directly to your liquor license through the Indiana Alcohol and Tobacco Commission. This coverage pays legal defense costs, medical expenses, and settlements when an intoxicated patron causes harm to themselves or others, and violations of liquor service laws create exposure that standard general liability policies explicitly exclude.

Additional Protections That Fill Critical Gaps

Food contamination coverage reimburses spoiled or contaminated inventory after power outages or refrigeration failures, averaging about $1,800 per incident and protecting against losses that standard property policies often exclude. Commercial auto insurance becomes mandatory if you offer delivery services, with typical costs ranging from $1,200 to $2,500 per year depending on vehicle type and driver history. A Business Owner’s Policy bundles property, general liability, and business interruption coverage at a discounted rate, simplifying management and reducing total premiums compared to purchasing separate policies. Indiana restaurants in flood-prone areas need flood insurance riders since standard property policies exclude water damage from rising water, though coverage varies by region across the state. Cyber liability insurance protects against data breaches and payment card compromises, increasingly important as online ordering becomes standard in the industry.

The total foundation coverage-general liability, property, and workers’ compensation-typically costs roughly $300–$500 per month for a small restaurant, with final pricing determined by your building ownership status, employee count, claims history, and whether you serve alcohol or offer delivery. Understanding these four pillars gives you a solid starting point, but the real work begins when you compare actual quotes and identify which optional coverages match your specific operation.

How to Actually Save Money on Restaurant Insurance

Compare Quotes From Multiple Carriers

Getting multiple quotes from different carriers is non-negotiable if you want competitive pricing, yet most Indiana restaurant owners stop after one online form and accept whatever rate appears first. When you request quotes from three or four A-rated carriers, you’ll often see premium differences of 30 to 50 percent for identical coverage limits-differences that compound to thousands of dollars annually. The process takes two hours max: document your building square footage, number of employees, annual sales projection, whether you own or lease, delivery services offered, and claims history from the past five years.

Contact independent agents who represent multiple carriers rather than relying on online quote tools that funnel you toward a single insurer. An independent agent can access pricing from companies like State Farm, Travelers, and Hartford simultaneously, showing you side-by-side comparisons that reveal which carrier values your specific risk profile. Don’t accept the first number-push back and ask agents to run quotes with different deductibles ($1,000 versus $2,500) and coverage limits ($500,000 versus $1,000,000 per occurrence) so you see the actual cost of upgrading protection.

Many restaurant owners discover that increasing general liability limits from $500,000 to $1,000,000 costs only $15 to $25 more per month, making the upgrade obvious once you see the numbers. This comparison process also exposes which carriers penalize you for specific exposures-some charge premiums 40 percent higher for delivery operations while others barely adjust the rate, so knowing these differences matters enormously.

Evaluate Bundled Policies Carefully

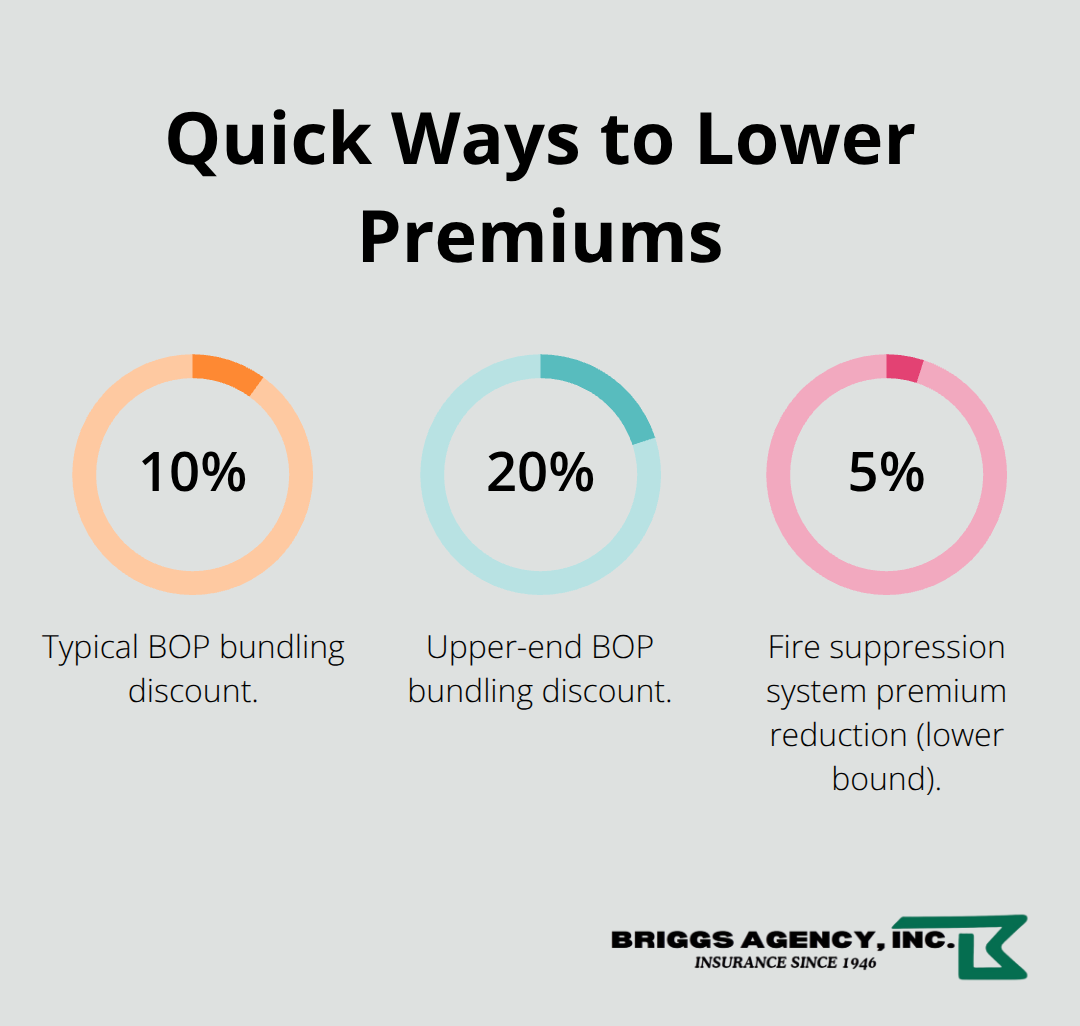

Bundling policies into a Business Owner’s Policy sounds convenient but demands scrutiny before you commit. A bundled BOP typically combines property, general liability, and business interruption coverage at a 10 to 20 percent discount compared to purchasing policies separately, which sounds attractive until you realize the bundled limits may not match your actual needs. An agent might bundle you into a $300,000 property limit to hit a lower premium, but if your kitchen equipment alone exceeds that value, you’re underinsured despite the discount.

Request separate quotes for each coverage type, then ask the agent to price a BOP, and compare total premiums rather than assuming bundling always wins. This approach reveals whether the discount actually saves you money or simply masks inadequate coverage.

Lower Premiums Through Operational Changes

Safety measures directly lower premiums across all carriers-maintaining clean floors prevents slip-and-fall claims, implementing documented food safety procedures reduces contamination exposure, and offering employee benefits cuts turnover and associated workers’ compensation costs. Installing fire suppression systems in your kitchen can reduce property insurance costs by 5 to 10 percent, while updating your employee manual and conducting regular safety training demonstrates risk management that insurers reward with lower rates.

The question to ask your local agent isn’t what coverage costs, but rather what specific operational changes would reduce your premium-some agents identify quick wins like installing a commercial hood cleaning service contract or upgrading lighting that immediately lower your rate. These conversations often reveal $2,000 to $4,000 in annual savings simply through restructuring deductibles and eliminating duplicate or unnecessary coverage, so a conversation with an agent who understands your operation pays for itself immediately.

Final Thoughts

Restaurant insurance in Indiana protects everything you’ve built, from your equipment and inventory to your employees and customers. Small restaurant insurance Indiana owners face real financial exposure that compounds every day without proper protection, and the coverage gaps we’ve outlined throughout this guide represent genuine risks that generic policies fail to address. Your restaurant’s specific setup determines what you actually need, which is why tailored coverage that matches your actual exposure beats one-size-fits-all approaches that leave critical gaps.

Start by documenting your operation’s details: building square footage, employee count, annual revenue projection, whether you own or lease, and any delivery or alcohol service you offer. Request quotes from multiple carriers using identical coverage specifications so you see real pricing differences, then evaluate whether bundling saves money or masks inadequate limits. Ask your agent which operational changes would lower your premium immediately, since this process takes a few hours but saves thousands annually and prevents the financial devastation that follows an uninsured loss.

A local independent agent who represents multiple carriers and understands Indiana’s specific legal requirements spots gaps that online tools miss, turning insurance from a cost center into genuine risk management. Contact Briggs Agency, Inc. to discuss your specific situation and receive quotes that reflect your real exposure rather than guessing based on what competitors carry.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.