Surety Bonds for Contractors: What You Need to Know

In the world of construction and contracting, trust and accountability are everything. Clients want to know that their projects will be completed on time, within budget, and according to specifications. That’s where surety bonds come in. If you’re a contractor, understanding how surety bonds work can not only help you win more jobs but also build credibility and protect your business.

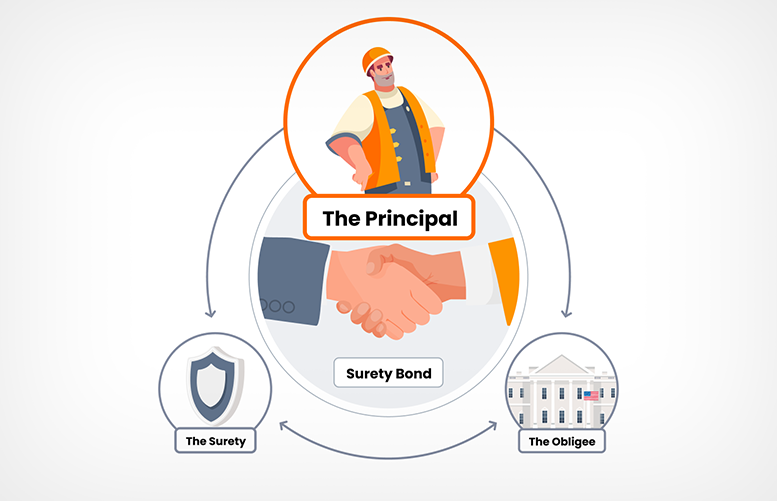

What Is a Surety Bond?

A surety bond is a three-party agreement between:

-

The Principal – That’s you, the contractor.

-

The Obligee – The client or project owner requiring the bond.

-

The Surety – The company that issues the bond and guarantees your performance.

Essentially, a surety bond is a financial guarantee that you will fulfill your contractual obligations. If you don’t, the surety steps in to cover the cost or ensure the job gets done—often up to the full value of the bond.

Types of Surety Bonds for Contractors

There are several types of surety bonds, but the most common in the construction industry include:

1. Bid Bonds

A bid bond guarantees that you, as the bidder on a project, will enter into the contract and provide the required performance and payment bonds if awarded the job. It gives the project owner confidence that your bid is serious and that you’re financially capable of following through.

2. Performance Bonds

These ensure that you’ll complete the project according to the terms of the contract. If you default, the surety company may pay for completion or hire another contractor to finish the job.

3. Payment Bonds

These protect subcontractors, laborers, and suppliers by guaranteeing they will be paid even if the contractor runs into financial trouble.

4. Maintenance Bonds

Sometimes called warranty bonds, these cover workmanship and materials for a certain period after a project is completed, ensuring the client won’t face unexpected costs due to faulty work.

5. Contractor License Bonds

Contractor license bonds are often required by state or local licensing boards as a condition of getting or renewing a contractor’s license. These bonds ensure that you’ll comply with applicable laws, building codes, and regulations. If a client or the licensing board files a claim due to misconduct, negligence, or code violations, the bond can provide financial recourse.

Why Surety Bonds Matter

-

They’re often required by law. For example, federal projects over $150,000 require contractors to be bonded under the Miller Act.

-

They build trust. A bonded contractor is seen as more reliable and financially stable.

-

They help you win contracts. Many public and private project owners won’t even consider unbonded contractors.

How to Get a Surety Bond

To obtain a surety bond, you’ll need to go through a surety company or bonding agent. The process typically involves:

-

A credit check and financial review

-

Providing business and personal financial statements

-

Sharing your project history and experience

Rates vary depending on the size of the bond and your creditworthiness, but premiums generally range from 1% to 3% of the bond amount.

Final Thoughts

Surety bonds are more than just a box to check—they’re a vital tool for protecting your business, your clients, and your reputation. Investing the time to understand and secure the right bonds can open doors to larger, more lucrative projects and long-term growth.

If you’re new to bonding or unsure where to start, we will guide you through the process and find the right fit for your business needs.